07.24.2026

2026 Halftime Market Insights

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

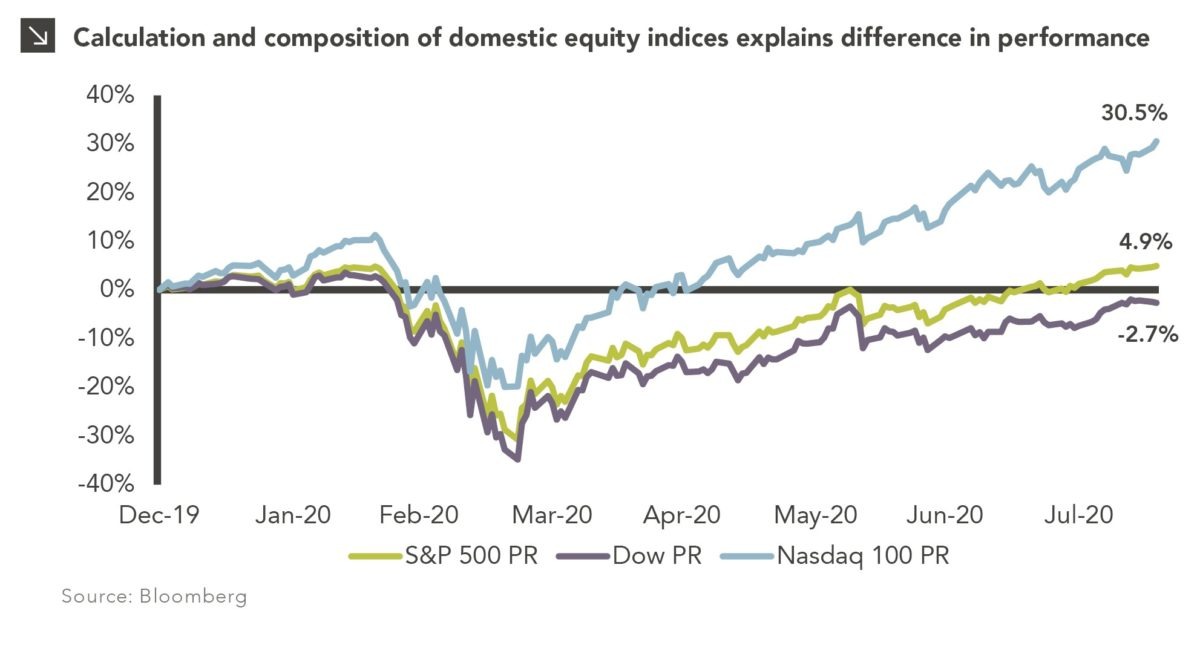

This week, the S&P 500 index closed at 3,389.78, setting its first record high since previously peaking on February 19th, 2020; it is up 4.9% year to date. This post-bear market recovery is officially the fastest ever. For the sake of comparison, it took more than three years for the S&P 500 to reclaim its peak after the Global Financial Crisis. However, the S&P 500 was not the first broad market index to reclaim its high in 2020. The NASDAQ 100 index surpassed its previous peak more than two months ago on June 5th and is up 30.5% year to date. On the other hand, the Dow Jones Industrials Average (DJIA) is still more than 5% off its record high and negative for the year.

How is it that each of these indices is considered to represent the broad domestic equity market, but they have such wide performance differences? The main reason is the calculation and composition of the indices. Let us begin with the Dow, the oldest index out of the three indices. Founded in 1896, the Dow is comprised of 30 stocks that are selected by their size and influence on American business (with the latter clearly being subjective). In addition, the DJIA is a price-weighted index which means that the companies with the highest share price have the highest weighting in the index. For instance, Apple, which trades at $462 a share¹ is the largest constituent in the DJIA with an 11.4% weight. The next largest constituent is UnitedHealth Group, which trades at $316 a share² and has a 7.8% weight in the DJIA. As a result, large price increases or declines in these stocks will have an outsized effect on the returns of the index. Consequently, the price decline in Boeing, a top 10 Dow constituent, due to delays in the Max 8 and lower demand from the COVID-19 pandemic has had a large impact on the Dow’s year-to-date return.

The S&P 500 and NASDAQ 100 indices are market capitalization-weighted indices. This means that the weightings of their constituents are based on the product of the stock price and the outstanding shares. As a result, stocks with high prices and the largest number of shares outstanding will have the greatest impact on the index’s return. In the case of the S&P 500, which tracks the largest 500 companies in America, this means that Apple, Microsoft, Amazon, Google, and Facebook are the largest constituents in the index. As discussed in my previous post, “There’s FAAMG and Everyone Else,” investor enthusiasm has propelled these stocks to new highs even though most of the companies in the S&P 500 are still negative for the year.

Technology companies have been the biggest beneficiaries of the COVID-19 pandemic and the NASDAQ 100, a proxy for the Technology sector, is more concentrated than the S&P 500 and more tech-centric than the DJIA. The NASDAQ 100, which was created in 1985, tracks the largest non-financial companies listed on the NASDAQ exchange. The FAAMG stocks are still the largest constituents in the NASDAQ 100, but Technology makes up over 55% of the NASDAQ 100 relative to 27.5% for the S&P 500 and 26.9% for the DJIA. It is also important to note that the Dow does not include Amazon, Google, or Facebook.

Over the short term, index calculation methods and composition differences can cause wide performance divergences. However, these divergences come and go based on the performance of the underlying sectors and companies. This year’s divergence has been exacerbated by the COVID-19 pandemic and the outperformance of Technology. As other non-Technology sectors rise in economic importance, we would expect the S&P 500 and DJIA to post more attractive relative returns.

Print PDF > And the Beat Goes On…

¹ Apple’s closing price as of August 18, 2020. Apple has also announced a 4-for-1 split effective August 31, 2020, which will reduce its price to ~$115 a share. Thus, Apple’s weight in the DJIA will decline accordingly.

² UnitedHealth Group’s closing price as of August 18, 2020.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >