Eddie Arrieta

Associate Research Analyst

Get to Know Eddie

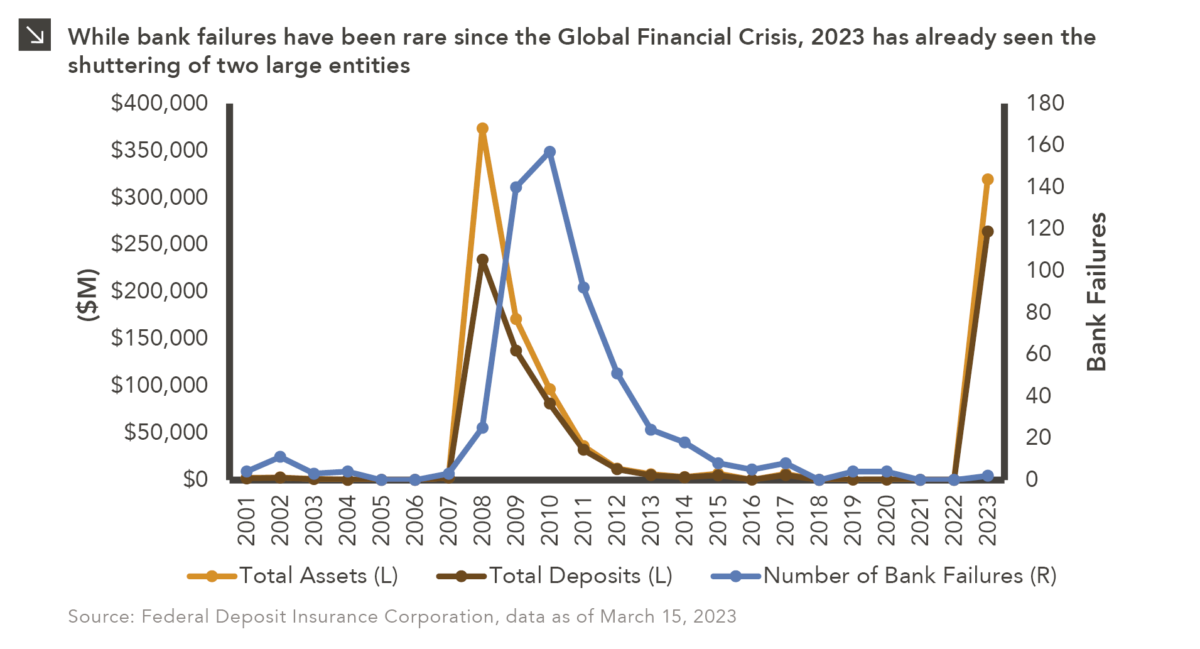

Recent developments within the banking industry have revived difficult memories of the Global Financial Crisis (GFC). As many will recall, hundreds of financial institutions failed during that period, including Washington Mutual (WaMu), a savings and loan organization with approximately $307 billion in assets at the time of its collapse. The Federal Deposit Insurance Corporation (FDIC) ultimately sold the banking subsidiaries of WaMu to JP Morgan for $1.9 billion, marking the largest U.S. bank failure in history. In total, 25 banks with combined assets of more than $373 billion closed their doors in 2008, with additional failures in 2009 (140 banks) and 2010 (157 banks). In response to the widespread impact of the GFC, the federal government enacted many new laws and regulations pertaining to the financial sector, which resulted in greater industry oversight and more robust stress tests of bank operations. While additional failures have occurred since the GFC, most banks have been healthy and resilient in the last decade, including during the COVID-19 pandemic. All told, a total of just eight banks with a combined $678 million in assets failed from 2018–2022.

Needless to say, dynamics within the domestic banking industry have shifted in the last several days. After a run on its deposits, Silicon Valley Bank, which had once been the 16th largest bank in the United States, failed and was placed into receivership of the FDIC on March 10. Silicon Valley Bank is now the second-largest bank to fail in American history, with approximately $209 billion in total assets and $175 billion in deposits at the time of its collapse. Signature Bank was the next domino to fall over the weekend, again due in part to a run on its deposits, and now stands as the third-largest U.S. bank failure ever ($110 billion in assets and $88.6 billion in deposits). While these two cases represent the only bank failures thus far in 2023, many regional banks have seen their share prices drop significantly amid fears of contagion.

It is important to remember that while GFC-inspired regulations were designed specifically to mitigate the fallout from these types of events, the situation related to recent bank failures is fluid and could have ongoing impacts on global markets and central bank interest rate policy. Marquette will continue to monitor dynamics within the banking industry and provide updates and counsel to clients accordingly.

Print PDF > Bank Failures: Past and Present

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.07.2026

JULY 23 — 1:00pm CT Please join Marquette’s research team for our 2026 Halftime Market Insights Webinar…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

06.25.2026

Commodities represent a unique asset class within global financial markets. Like equities and bonds, commodity prices are influenced by the…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >