Chad Sheaffer, CFA, CAIA

Associate Director of Private Credit

U.S. consumer sentiment has become increasingly pessimistic in 2022 as a plethora of macro headwinds have created uncertainty. The University of Michigan Consumer Sentiment Index, a key proxy for consumer confidence, fell to 58.4 in May, the lowest reading since August 2011. The survey aggregates consumer views across a range of questions including personal finances, general business conditions, housing market conditions, spending expectations, and outlook. The overall level of the index and the relative change from prior readings provide an indication as to how consumers feel about the current and future U.S. economy. Since its inception in 1978, the survey has posted a reading below 60 in only three other distinct periods: the late stages of the stagflationary environment in 1980, the Global Financial Crisis in 2008–2009, and a brief period in 2011 when S&P Global Ratings downgraded U.S. Treasury debt.

Despite consumer spending comprising the majority of GDP, extremely bearish consumer sentiment has historically been a poor predictor of recession. Survey readings below 60 have coincided with a recession only 33% of the time (two out of six recessions) since 1978. Consumer sentiment surveys seem to be far more indicative of the current consumer experience than the longer-term economic outlook. As seen in this week’s chart, the University of Michigan Consumer Sentiment Index has shown a strong correlation to gasoline prices — a very visible component of inflation for most consumers — especially during periods of rising gas prices. While current sentiment can have a very real impact on economic growth via consumer spending, it is important to consider this metric alongside other economic measures, many of which still show consumer strength. With the market laser-focused on the health of the U.S. consumer and the risk of recession, we will continue to monitor various economic indicators and advise our clients accordingly.

Print PDF > Consumer Sentiment: Harbinger for Recession or a Reflection of Pain at the Pump?

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

08.10.2026

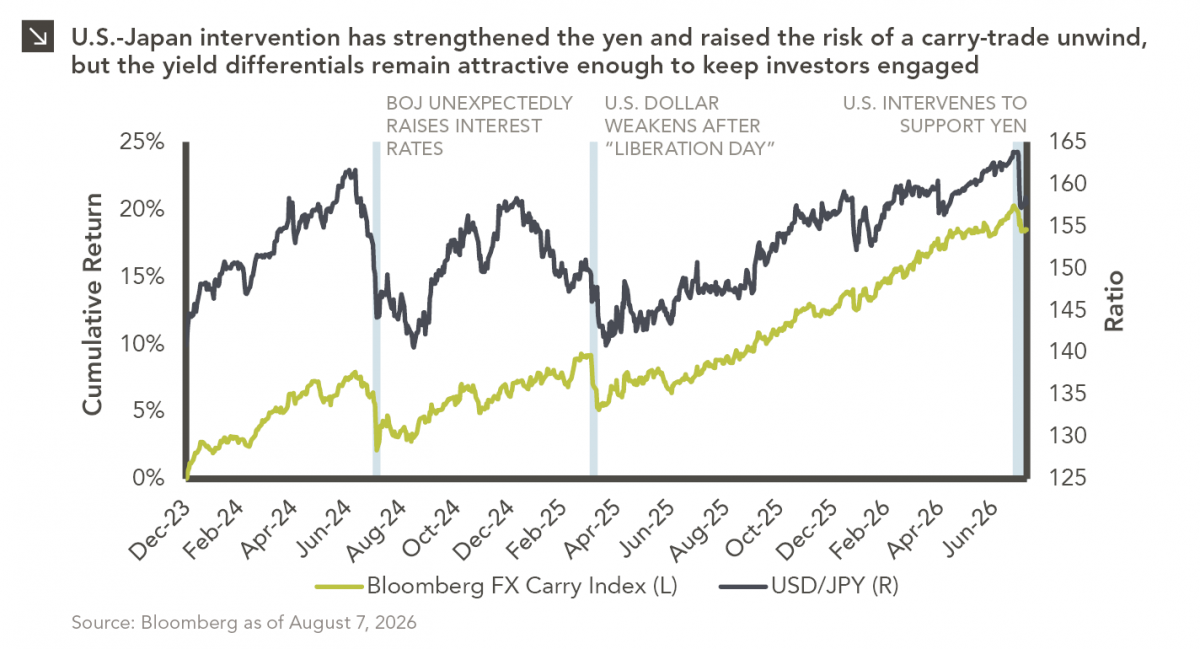

After reaching nearly ¥164 per dollar, its weakest level in roughly four decades, the yen had become a source of…

08.03.2026

In the cinematic masterpiece Rocky IV, Rocky gets dazed by his opponent, Captain Ivan Drago, and complains that he sees…

07.27.2026

The rapid growth of non-traded business development companies (BDCs), which are investment vehicles that pool investor capital to make loans…

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >