07.24.2026

2026 Halftime Market Insights

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

On November 15, 2017, S&P Dow Jones Indices, a leading provider of financial market indices, and MSCI Inc., a leading provider of research-based indices and analytics, conducted their annual review of the Global Industry Classification Standard (GICS). As a result, the pair decided to broaden and rename the Telecommunications Services sector to the Communications Services sector. The thought process is that over the past several years consumers and businesses have fundamentally transformed the way in which they communicate and access content.

In some ways, this trend started when Comcast, a cable company, announced its intention to purchase a stake of NBC Universal, a television network and content provider, in 2007. The latest example of the convergence between communications and media is the on-going asset fight between Fox, Comcast, and Disney for Sky PLC, a European satellite broadcaster. Moving away from traditional communications and media companies, firms like Alphabet through its Google search engine and YouTube, Facebook through its ever-expanding social media platform, and Netflix through its direct-to-consumer streaming content, have changed the way the world communicates and accesses content. The lines have officially blurred and S&P along with MSCI decided to take action.

What impact will this have on investors?

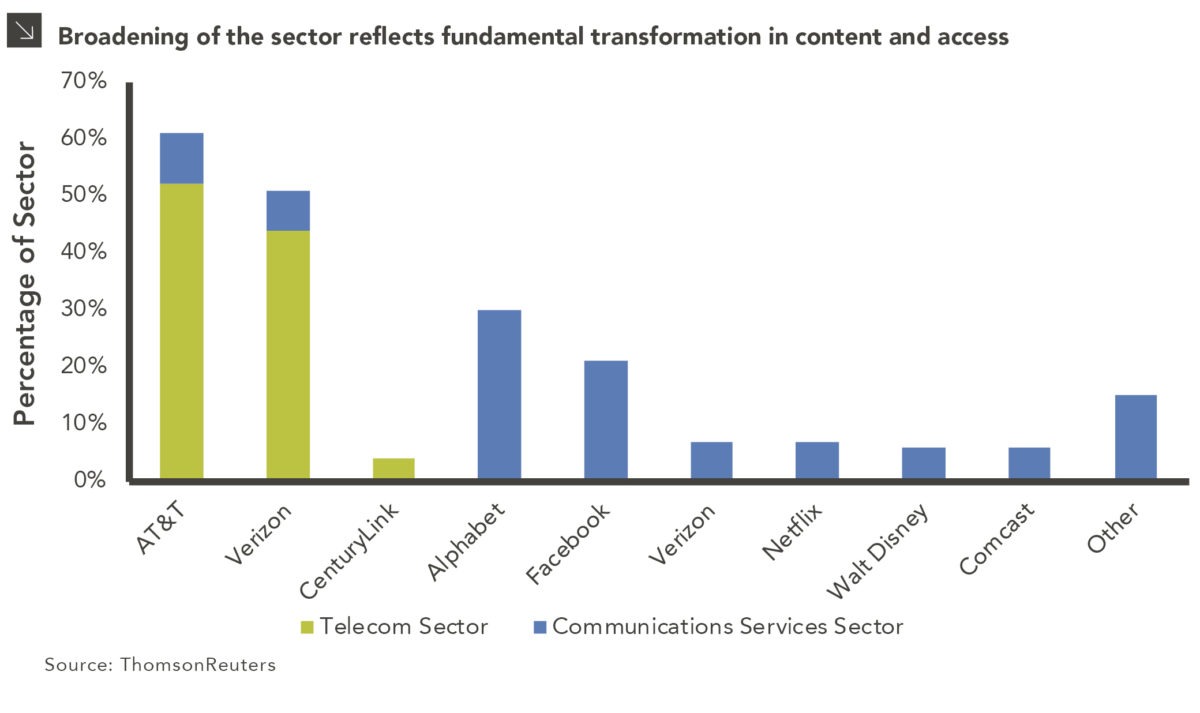

On September 21, 2018, the Telecommunications Services sector, the smallest sector at a 2% weight in the S&P 500 will quintuple in size to become the fourth largest sector in the index at the expense of the Information Technology and Consumer Discretionary sectors. This change is much larger than GICS’s creation of the Real Estate sector in 2016, which affected approximately 3% of the index’s market cap. Sleepy firms like AT&T, Verizon and CenturyLink will be grouped in the same sector as Alphabet, Facebook, and Netflix, just to name a few. Most notably, a sector classified as 100% value will be primarily growth-oriented.

The composition change is shown in the above chart; the formerly dominant names of AT&T, Verizon, and CenturyLink of the Telecom sector (shown in green) will now occupy a much smaller percentage of the new Communications Services sector, as shown by the considerably smaller blue boxes in the graph.

Luckily, most investment managers select stocks based on their investment merits and not their GICS sector classification. An investment manager that owns Alphabet (Google), which is currently classified as an Information Technology stock, on September 21st will continue to hold it on September 22nd. Much like the creation of the Real Estate sector in 2016, there is no action needed on the part of investors. We will continue to monitor new developments as S&P and MSCI finalize the change over the coming months.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >