07.24.2026

2026 Halftime Market Insights

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

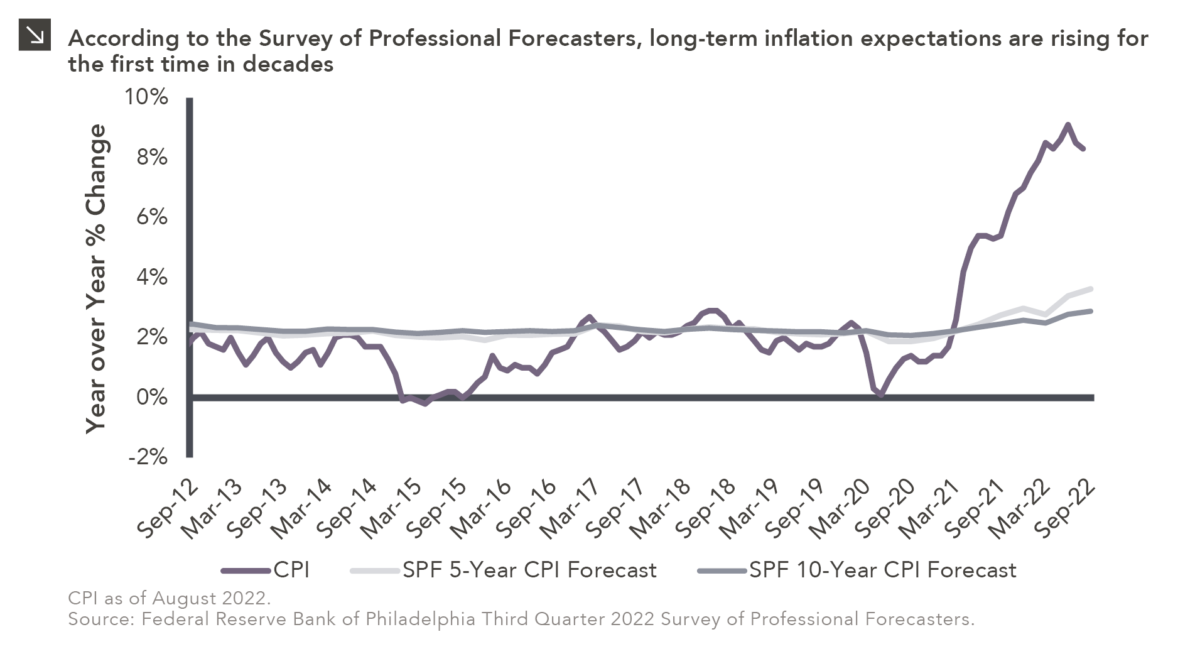

The announcement of another 75 basis point rate hike at last week’s FOMC meeting reaffirmed the Federal Reserve’s unwavering commitment to reducing inflation. One of the key variables the Fed watches to help it determine the path of rates is expected inflation. Inflation can become a self-fulfilling prophecy if consumers start pricing future inflation into their decision-making and businesses start making anticipatory adjustments to their prices and behavior. To combat this, the Fed strives to anchor expectations around a 2% target inflation rate. When long-term inflation forecasts deviate from that 2% target it means inflation expectations are not well-anchored, i.e., people believe that a short-term rise in inflation could lead to higher price levels longer-term.

Inflation expectations have moved further away from the 2% target over the course of 2022, something the Fed recognizes as a potential roadblock in navigating the current inflationary environment. Indeed, Fed Chair Jerome Powell stressed the importance of “expeditiously continuing to raise rates” to “ensure that longer-term inflation expectations remain well-anchored” at the June FOMC press conference.¹ With higher-than-anticipated August CPI figures, however — headline inflation of 8.3% and core inflation that reaccelerated to 6.3% — inflation expectations may remain higher for longer. Headline inflation is moving in the right direction, but core inflation, which remains well above Fed targets, tends to be stickier and may further complicate the Fed’s task. While there are no crystal balls, longer-term inflation expectations will continue to bear monitoring as investors search for potential indicators of a market bottom.

Print PDF > Inflation: Expectations Matter

¹ Lee, J., Powell, T., & Wessel, D. (2022, June 27). What are inflation expectations? Why do they matter? The Brookings Institute. Retrieved September 28, 2022.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >