07.24.2026

2026 Halftime Market Insights

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

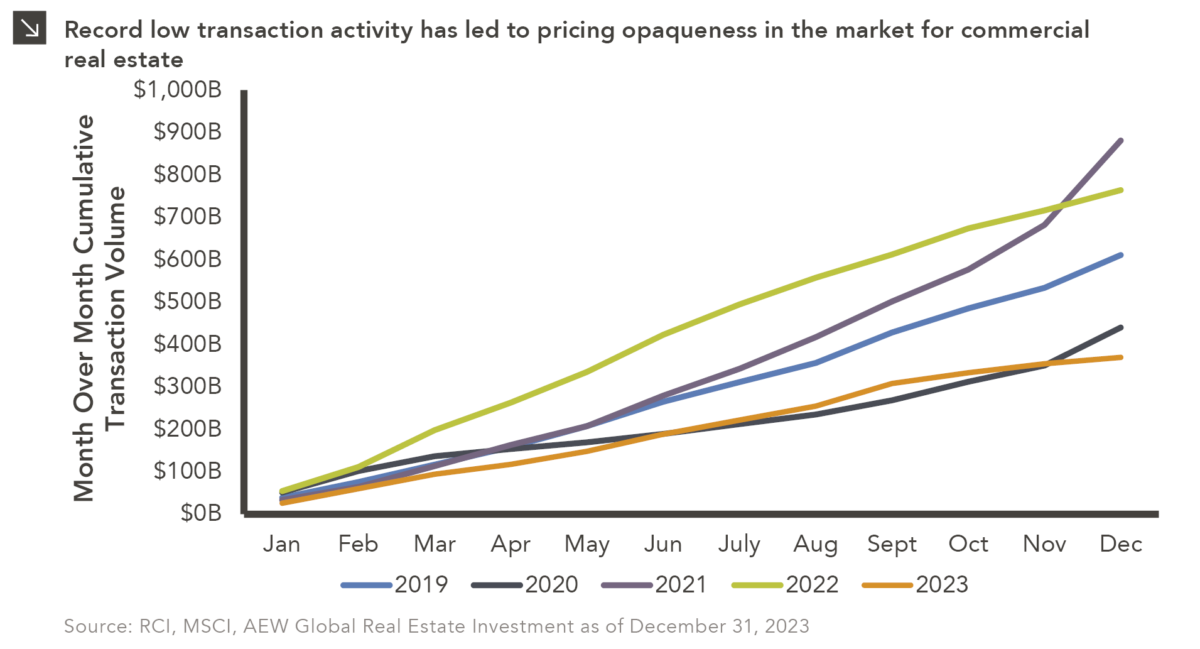

The 10-year Treasury yield notably displayed significant movements throughout 2023. Specifically, it was largely range-bound over the summer (between 3.5%–3.8%), then shot up to around 5.0% in October before falling back down to under 4.0% before year-end. It currently hovers slightly above 4.1%. Thanks in large part to these movements in yields, the real estate market seized up and very few transactions occurred in the fourth quarter of last year. As a result, the full calendar year of 2023 exhibited the lowest transaction volume in the last five years. Limited transactions in the market provide a hurdle for real estate managers and third-party appraisers to accurately determine asset values. As such, the pace of contraction for the private real estate index NCREIF-ODCE has been choppy, with the latest quarter responsible for nearly one-third of the benchmark’s gross return correction of -16.4% since late 2022.

Quarterly returns for the underlying index managers have been volatile in recent time as well. Based on a sample of 18 of the 25 ODCE index funds, the average spread of gross returns over the last five quarters has been nearly 6 percentage points. For context, the longer-term spread is closer to 4 percentage points. Additionally, each fund in that sample has underperformed the ODCE benchmark in at least one of the last six quarters. These figures underscore the notion that recent marks have displayed an elevated degree of dispersion and noise.

Even with the considerable drop in valuations, real estate fundamentals remain relatively healthy outside of the office space. Most do not believe assets are broken, and rent growth still exists within the multifamily, industrial, and self-storage sectors (albeit at lower levels than in prior years). As it relates to the road ahead, real estate investors should remain patient as market dynamics play out. To that point, it may take several quarters for buyers to come off the sidelines, after which more transactions can occur and ultimately be reflected in valuations. Marquette will continue to monitor the real estate landscape while emphasizing the importance of prudence and a long-term perspective.

Print PDFThe opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

06.22.2026

When Benchmark, one of Silicon Valley’s most renowned early-stage venture capital firms, closed $2 billion across two new funds this…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >