Thomas Neuhardt

Associate Research Analyst

Get to Know Thomas

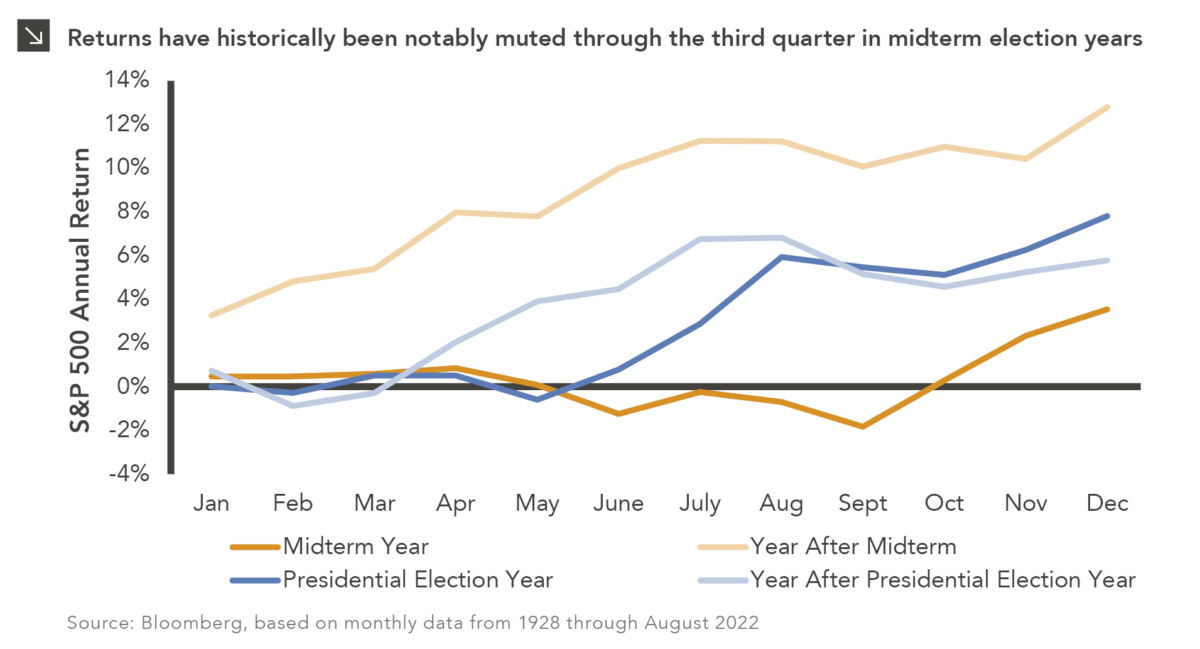

If inflation, rising rates, and a war in Europe were not enough to keep markets interesting this year, 2022 is also a midterm election year. Based on data over the last nine decades, midterm election years — while only marginally more volatile than non-election years overall — tend to exhibit a distinct performance pattern throughout the year. On average, returns during midterm years tend to be flat to slightly negative through the first three quarters as investor confidence is dampened by uncertainty around the outcome of the election. Historically, returns start to pick up as November draws near and tend to finish strongly, with fourth quarter returns in midterm years significantly stronger than non-midterm years. This holds true regardless of which party wins the House and Senate and whether or not there is a change of control, suggesting investors value predictability more so than a specific party controlling Congress. While each year is unique, and this analysis does not consider the deluge of other macroeconomics issues plaguing 2022, it is interesting historical context. Come November 6, there may be one less source of uncertainty in markets.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >