Jessica Noviskis, CFA

Portfolio Strategist, OCIO Services

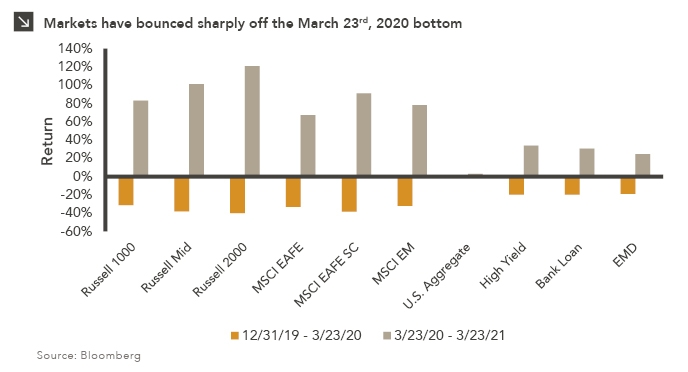

What a year it has been. Officially one year after the equity market’s bottom on March 23rd, 2020, all major indices in the chart above have at least recovered back to ending 2019 levels. The groups that were hit the hardest have also rebounded the strongest, with returns over the last year exceeding 100% for some. Small-cap equities stand out, especially in the U.S. — up 121% over the last year and up 33% over the almost 15-month period since 2019. U.S. mid-cap equities are up 101% over the last year, up 25% over the full period, and U.S. large-cap equities are up 83% over the last year for a 26% return over the full period. Small-cap stocks have also outperformed internationally — the MSCI EAFE Small Cap Index is up 91% over the last year and 18% since 2019, while the MSCI EAFE Index is up 67% over the last year and 12% for the full period. Emerging markets, some of the hardest hit by the crisis last year, have more than recovered, up 78% over the last year for a 22% return since 2019. Fixed income returns have been more muted. Investment grade bonds stayed positive in early 2020 as equity markets fell precipitously and are up another 3% since. High yield bonds, bank loans, and emerging market debt were hit harder but still held up better than equities. Each group has recovered those losses but remains in positive single-digit territory over the full period.

From here, we expect returns will likely moderate. As the vaccine roll-out continues we expect further economic re-openings and renewed growth across the globe, but it seems highly unlikely capital markets returns can continue at this pace beyond the initial recovery.

Print PDF > One Year Ago, Would Anyone Have Predicted This?

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >