James Torgerson

Senior Research Analyst

The National Bureau of Economic Research (NBER) is widely considered the official judge on what is and is not a recession. The academic organization’s traditional definition of a recession is a “significant decline in economic activity that is spread across the economy and lasts more than a few months.” This definition can be subjective and, to help avoid the need for revisions, the committee does not typically call the start of a recession, or the end of a recession, until well after the fact.

Another commonly accepted definition of a recession is at least two consecutive quarters of negative GDP growth. Given the last two GDP prints of -1.6% in the first quarter and the advance estimate of -0.9% in the second quarter, the U.S. economy would be in a technical recession. Recently, both the White House and Federal Reserve Chairman Jerome Powell have argued that this interpretation does not accurately reflect the current state of our economy, specifically given the still-strong labor market.

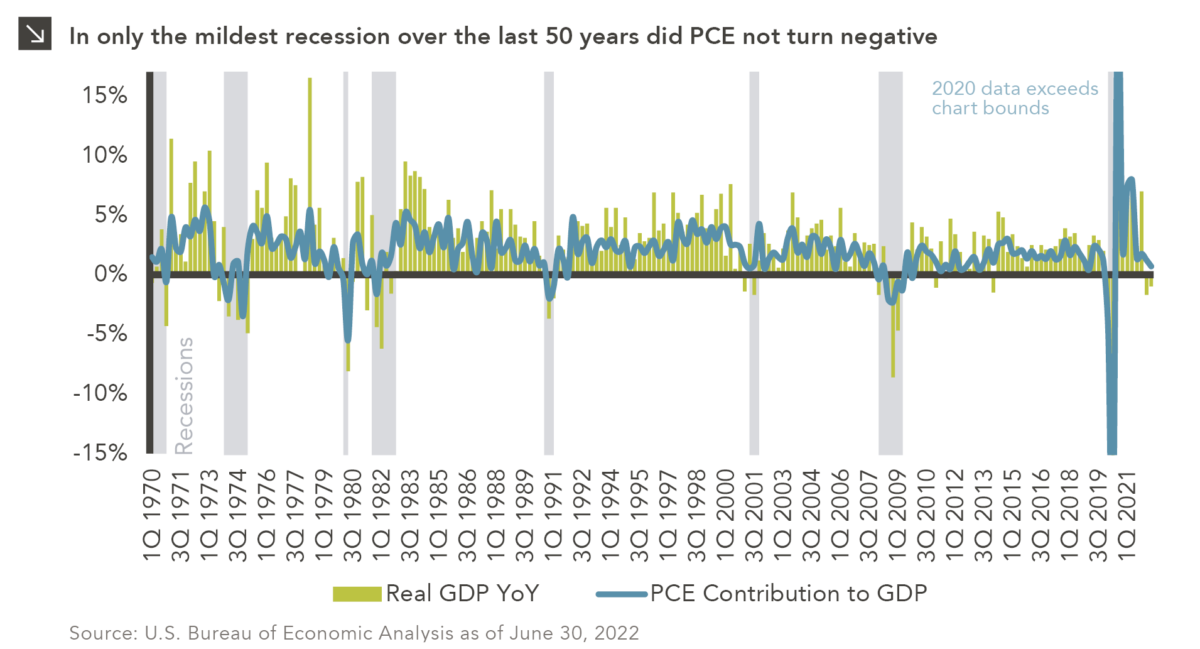

Another economic indicator to consider is consumer spending, specifically the contribution to GDP from Personal Consumption Expenditures (PCE). Consumer spending comprises 70% of GDP and is traditionally a much less volatile component than investment and net exports, the primary contributors to the year-over-year declines in the first half of the year. The strength of the U.S. consumer will dictate the country’s path from here, as healthy balance sheets and a hot labor market contend with decades-high inflation and rising rates. PCE contributed a positive 1.2% and 0.7% to first and second quarter GDP, respectively. In only one of the last eight recessions over the last 50 years — the relatively mild downturn in 2001 — has PCE not turned negative. One month into the third quarter, the highly-regarded Atlanta Fed GDPNow tracker is projecting positive PCE and overall GDP growth for the quarter. The current macro situation is complex, with a healthy U.S. consumer facing a number of headwinds, and, in this case, understanding those underlying dynamics is just as important as the “are we or aren’t we” debate.

Print PDF > Recession Redefined

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.27.2026

The rapid growth of non-traded business development companies (BDCs), which are investment vehicles that pool investor capital to make loans…

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >