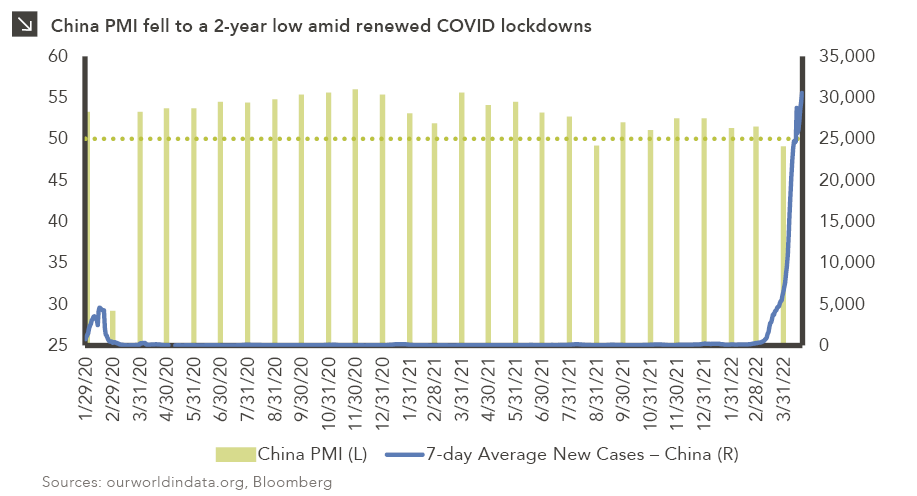

COVID cases have been on the rise in China over the last ten weeks, surpassing February 2020 highs by 800%. The seven-day rolling average has moved from 110 new cases at the end of January 2022 to a high of 30,500 on April 21st. Since the beginning of the pandemic, China has operated with a zero-COVID policy, combining testing and tracing with the use of lockdowns to prevent the spread of the virus. These measures have resulted in an extremely low case count compared to the rest of the world. The country’s recent high near 30,000 is still well below the U.S. seven-day average peak of 800,000 in January 2022.

China’s aggressive use of lockdowns to control the spread of the virus has impacted the country’s economic activity. March’s Purchasing Managers Index (PMI) reading was 48.8, below the neutral 50 mark, indicating a contraction in economic activity. Several Chinese cities are feeling the pressures of the recent lockdown, including Shanghai, a key finance and manufacturing hub. Many investors expect Chinese authorities to step in with supportive policies to help the country navigate the current downturn. Ultimately, however, China may need to choose between two of its seemingly opposing agenda items — its zero-COVID policy and its 5.5% target growth rate — with the choice likely to have material implications for equity markets for the rest of 2022.

Print PDF > Lockdowns Lead to Slowdown