The leadership structure of the Federal Reserve is intentionally designed to promote continuity, independence, and institutional stability across political cycles. Specifically, the seven members of the central bank’s Board of Governors serve staggered 14-year terms, while the Chair is appointed to a renewable four-year term by the president and confirmed by the Senate. In this context, the nomination of Kevin Warsh by the Trump administration earlier this year to lead the Fed marks a potential inflection point for U.S. monetary policy leadership. Warsh brings a combination of public- and private-sector experience, having served as a Federal Reserve governor during the Global Financial Crisis, worked in mergers and acquisitions at Morgan Stanley, and later advised policymakers and investors as a fellow at the Hoover Institution and lecturer at Stanford. Warsh’s nomination, first announced in late January and now nearing final Senate confirmation, comes as Jerome Powell is set to end his term as Chair in the coming days, concluding a tenure defined by extraordinary economic shocks and aggressive policy responses. Recent developments have effectively cleared the path for this transition, with Warsh expected to assume the role shortly after Powell’s term expires, even as Powell has indicated he intends to remain on the Board of Governors through 2028 in a move aimed at preserving institutional continuity. Against this backdrop, Warsh is in position to take the helm of a Federal Reserve that has recently undergone a historic tightening cycle and is now navigating the late stages of the inflation fight, setting the stage for what is likely to be an evolution (rather than a reset) of policy direction.

Topic Tags: Interest Rates

We’ve Seen This Before

Diversify. Rebalance. Stay invested. Every one of these letters has concluded with that same advice in some shape or form. It’s not particularly shiny and new, but the best documented path to a successful long-term investment program. The last eight weeks are another data point in support of these practices.

In this edition:

- Impact of U.S.–Iran conflict on oil prices, interest rates, and equity markets

- Volatility and drawdowns in the market cycle

- Equity market rotation

- Magnificent 7 detraction and increased market breadth

- Slowdown in non-U.S. equities

1Q 2026 Market Insights Webinar

This video is a recording of a live webinar held April 16 by Marquette’s research team analyzing the first quarter across the economy and various asset classes as well as themes we’ll be monitoring in the coming months.

Our quarterly Market Insights series examines the primary asset classes we cover for clients including the U.S. economy, fixed income, U.S. and non-U.S. equities, hedge funds, real assets, and private markets, with commentary by our research analysts and directors.

Featuring:

Greg Leonberger, FSA, EA, MAAA, FCA, Partner, Director of Research

James Torgerson, Senior Research Analyst

Fred Huang, Research Analyst

David Hernandez, CFA, Director of Traditional Manager Search

Evan Frazier, CFA, CAIA, Senior Research Analyst

Dennis Yu, Research Analyst

Hayley McCollum, Senior Research Analyst

Sign up for research alerts to be invited to future webinars and notified when we publish new videos.

If you have any questions, please send our team an email.

Seventy-Five Horses and Two Pieces of Plastic

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest powered by a 75-horsepower engine with two plastic skis to steer makes it hard to feel like one has complete control; 30 mph in the open air feels more like 100!

Nonetheless, operating a snowmobile is pretty straightforward: The throttle is a right-thumb button, the brake is a left-hand squeeze lever. Beyond those two controls, it’s up to the driver to effectively navigate the trail, with the critical concession that the terrain is out of anyone’s complete control. Which brings me to our 2026 market outlook.

The “throttles” for portfolios are the usual constituents: equities, below investment grade credit, and private markets. The “brakes” are investment grade fixed income, particularly Treasuries which can slow a portfolio’s losses if the market tumbles. The terrain is naturally the actual path that each of these asset classes will follow in 2026. Since 2022 the equity market ride has been mostly exhilarating, save for some of the terrifying moments like the market dip after Liberation Day. But that’s in the rearview mirror, and the focus is what is around the bend. Will the thrill continue, or should we ease up on the throttle?

2026 Market Preview

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the economy and various asset classes as well as themes we’ll be monitoring in 2026.

Our quarterly Market Insights series examines the primary asset classes we cover for clients including the U.S. economy, fixed income, U.S. and non-U.S. equities, hedge funds, real assets, and private markets, with commentary by our research analysts and directors.

Featuring:

Greg Leonberger, FSA, EA, MAAA, FCA, Partner, Director of Research

Frank Valle, CFA, CAIA, Associate Director of Fixed Income

James Torgerson, Senior Research Analyst

Catherine Hillier, Senior Research Analyst

David Hernandez, CFA, Director of Traditional Manager Search

Evan Frazier, CFA, CAIA, Senior Research Analyst

Dennis Yu, Research Analyst

Amy Miller, Associate Director of Private Equity

Chad Sheaffer, CFA, CAIA, Associate Director of Private Credit

Sign up for research alerts to be invited to future webinars and notified when we publish new videos.

If you have any questions, please send our team an email.

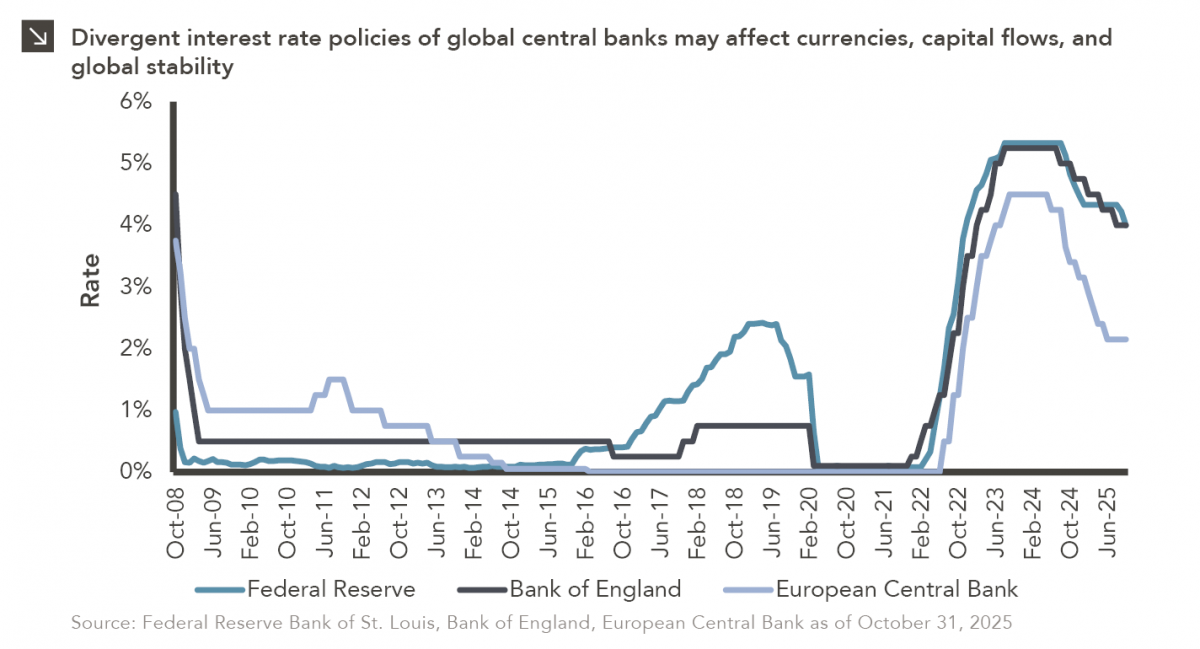

Central Bank Examination

After a largely synchronized hiking cycle beginning in 2022, there has been a slight divergence in interest rate policies across the Federal Reserve, European Central Bank, and Bank of England in recent time. Both the ECB and BoE initiated their easing cycles in the middle of last year, ahead of the Fed, which has since followed suit with its latest rate cut coming last month. The target range for the effective federal funds rate is now 3.75– 4.00%. The policy rate of the BoE also hovers near 4% following its August 2025 cut, and the central bank is expected to maintain this positioning through November. Meanwhile, the latest rate reduction by the ECB in June has brought its policy rate down to roughly 2.2% given the relatively weaker growth and lower inflationary pressures faced by the euro area.

While it is critical for central banks to maintain independent monetary policies tailored to the conditions of their respective economies, disparate rate regimes across the developed world could have significant implications. For instance, global currency markets remain highly sensitive to interest rate differentials, and currency movements can meaningfully shift trade balances since goods from the country with the stronger currency become more expensive abroad. Additionally, investors may redirect capital toward regions with higher yields, impacting security prices and creating volatility in global financial markets as funds move across borders. In conclusion, if these central banks opt for different policy paths going forward, an additional layer of uncertainty will likely be added to the broader economic outlook.

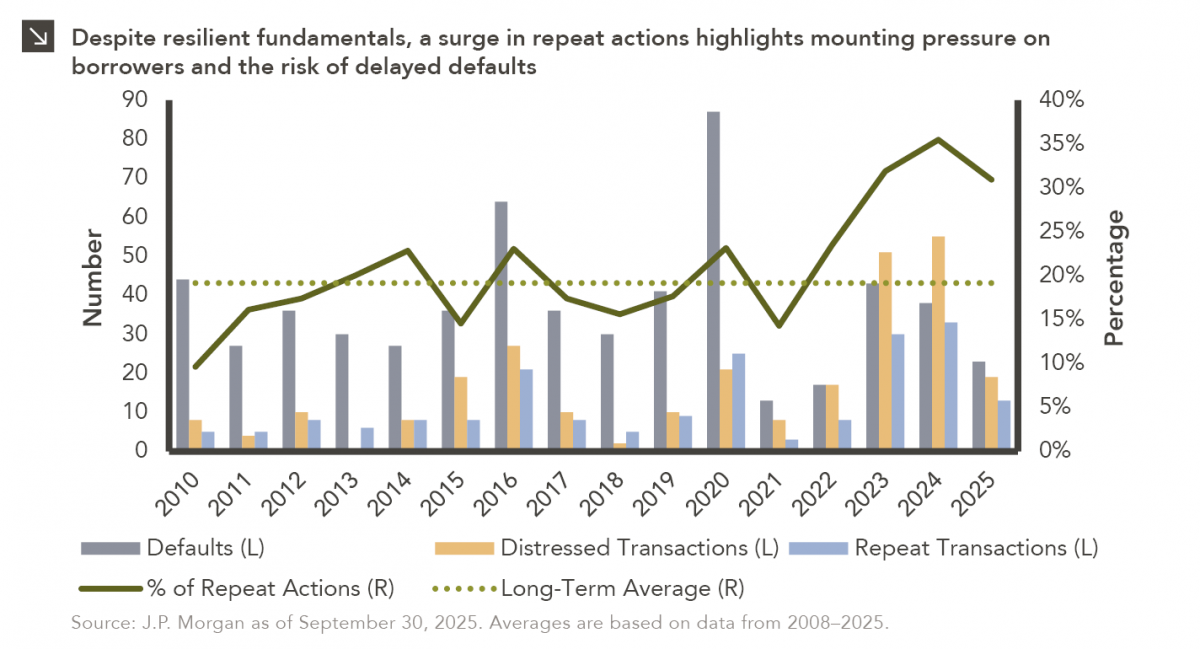

Don’t Make Me Repeat Myself

To paraphrase a quote from former President George W. Bush: “Fool me once, shame on… shame on you. Fool me — you can’t get fooled again.” This botched attempt at quoting the common phrase aside, the below-investment grade market shows that it can, in fact, get fooled again. High-profile defaults from subprime auto lender Tricolor and auto parts manufacturer First Brands have recently made waves, but additional default trends exist below the hood (automotive pun intended) and are currently flying under the radar.

This week’s chart shows a meaningful increase in the percentage of leveraged credit borrowers conducting repeat distressed and default actions. A repeat action is defined as when a borrower that has previously undergone a distressed transaction or default undergoes either another distressed transaction, defaults after a distressed transaction, or defaults again. Since 2008, an average of 19% of borrowers who underwent either a distressed transaction or default went on to conduct a repeat action according to J.P. Morgan. This figure has increased meaningfully to 33% since the beginning of 2023. There are many factors fueling this increase, including a sustained environment of higher interest rates and the increased desire of lenders to recoup portions of their investments. However, repeat actions don’t have favorable outcomes for all parties, as approximately 72% ultimately end in the borrower defaulting. While a repeat transaction can serve as a lifeline to a stressed borrower, it typically just ends up “kicking the can” on the eventual default.

Broadly, headline defaults remain below or near long-term averages within leveraged credit, even when incorporating distressed transactions. Additionally, leveraged credit fundamentals remain resilient. The high yield bond market is now of significantly higher quality than it has been historically, as some of the lowest quality borrowers in the space have opted to transact in private markets. Additionally, interest costs should begin to ease for borrowers as the Federal Reserve continues its easing cycle. However, the increase in repeat actions shows that the most stressed borrowers remain under pressure and are trying to delay defaults as long as possible. This is a dynamic that certainly bears monitoring. Going forward, while additional defaults like First Brands may generate headlines, idiosyncratic developments likely won’t offset a fundamental environment that has not shown broad-based deterioration. Some may get fooled, but the key is to not get fooled again.

3Q 2025 Market Insights

This video is a recording of a live webinar held October 22 by Marquette’s research team analyzing the third quarter across the economy and various asset classes as well as themes we’ll be monitoring through the rest of 2025.

Our quarterly Market Insights series examines the primary asset classes we cover for clients including the U.S. economy, fixed income, U.S. and non-U.S. equities, hedge funds, real assets, and private markets, with commentary by our research analysts and directors.

Featuring:

Greg Leonberger, FSA, EA, MAAA, FCA, Partner, Director of Research

Frank Valle, CFA, CAIA, Associate Director of Fixed Income

James Torgerson, Senior Research Analyst

Catherine Hillier, Senior Research Analyst

David Hernandez, CFA, Director of Traditional Manager Search

Evan Frazier, CFA, CAIA, Senior Research Analyst

Dennis Yu, Research Analyst

Amy Miller, Associate Director of Private Equity

Sign up for research alerts to be invited to future webinars and notified when we publish new videos.

If you have any questions, please send our team an email.

2025 Investment Symposium

Watch the flash talks from Marquette’s 2025 Investment Symposium livestream on September 26 in the player below — use the upper-right list icon to access a specific presentation.

- Public vs. Private: A Fixed Income Collision

Frank Valle, CFA, CAIA, Chad Sheaffer, CFA, CAIA, and James Torgerson - What Makes a Good Fiduciary?

Linsey Schoemehl Payne and Stephanie Osten - The Changing Face of Real Estate

Greg Leonberger, FSA, EA, MAAA, FCA - U.S. Equity Markets: Trend or New Normal?

Catherine Hillier - Private Equity in 2026 and Beyond: Allocations, Expectations, and the New Reality

Amy Miller and Chris Caparelli, CFA - Will U.S. Exceptionalism Continue for Global Equities?

David Hernandez, CFA

Please feel free to reach out to any of the presenters should you have any questions.

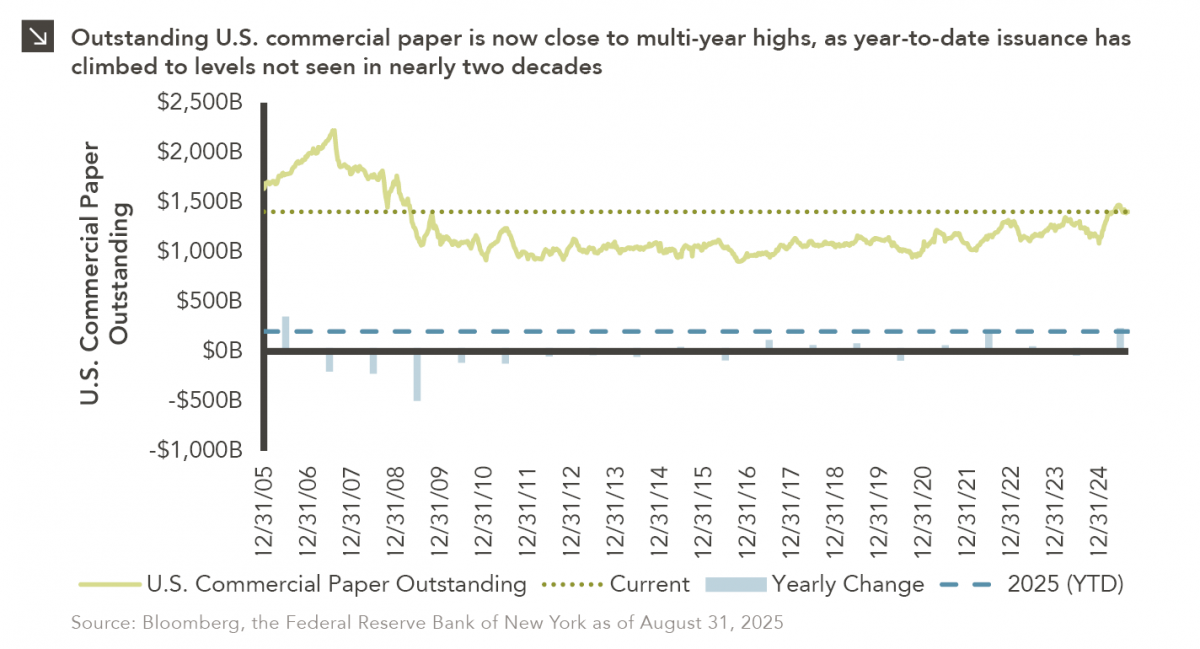

Getting That Paper

Commercial paper is a type of unsecured debt instrument that can be utilized by companies to finance short-term liabilities. The U.S. commercial paper market, which eclipsed $2 trillion in total value in 2007, was decimated in the aftermath of the Global Financial Crisis, with ultra-low interest rates pushing most companies toward longer-term obligations. That said, this method of financing is currently experiencing a revival, as 2025 has seen more than $200 billion in new U.S. commercial paper issuance. This is the highest figure notched in a calendar year since 2006. Indeed, major corporations including Uber, Netflix, Coca-Cola, PepsiCo, Philip Morris, and Honeywell have recently ventured into the commercial paper market, collectively raising billions through instruments that usually mature within one to three months. Total U.S. commercial paper outstanding stood at more than $1.4 trillion at the end of August.

The recent growth of the commercial paper market reflects a notable change in how U.S. companies are choosing to finance operations. With borrowing costs elevated and trade tensions persisting, firms have opted to bolster cash reserves while avoiding the higher expense of long-term debt, particularly as potential interest rate cuts from Federal Reserve loom. This trend is consistent with the approach of the U.S. Department of the Treasury, which has relied heavily on short-term T-bill issuance to cover government funding needs. It is important to note, however, that commercial paper utilization exposes issuers to certain risks. For instance, if long-term interest rates remain high, companies could be forced to regularly roll over short-dated obligations. A surge in short-term borrowing by both businesses and the government may also increase competition for investors, raising funding costs further.