Commodities represent a unique asset class within global financial markets. Like equities and bonds, commodity prices are influenced by the macroeconomic environment, geopolitical events, and technological developments. However, because commodities are tangible assets, their prices are also directly affected by physical supply-and-demand dynamics, weather patterns, and other factors unique to underlying resource markets. Recent structural trends, including rising demand for metals within the technology and renewable energy sectors, have created secular tailwinds for certain commodities that potentially complement the asset class’s traditionally cyclical characteristics. Additionally, evolving energy market dynamics may provide further structural support. Years of underinvestment in conventional energy production coupled with recent geopolitical conflicts and damage to critical infrastructure in the Middle East have increased concerns about the long-term resilience of global energy supply chains, potentially supporting elevated energy prices relative to historical norms. Simultaneously, global inflationary pressures and conflicts across the world have renewed interest in commodity allocations as a hedge against macroeconomic uncertainty and geopolitical strife. This paper examines the viability of commodities in institutional portfolios by exploring the dynamics of commodity cycles and demand drivers, analyzing the historical performance of the asset class, and outlining risk management considerations. By reviewing both opportunities and challenges, the paper aims to provide a balanced and educational assessment for institutional investors seeking to understand the role of commodities in modern portfolios.

Topic Tags: International Economy

The New Face of Emerging Markets

The MSCI Emerging Markets Index has undergone a significant structural transformation in recent years. For much of the past decade, China dominated the benchmark, but Taiwan now represents the largest country in the index at roughly 27%, with South Korea close behind at around 23%. After reaching nearly 40% at the end of 2020, China’s weight in the index now sits below 20%. This shift has largely been driven by the strength of Taiwan and South Korea in the semiconductor space and the global AI infrastructure buildout. For example, Taiwan Semiconductor Manufacturing Company (TSMC), the world’s leading contract chip manufacturer and a critical supplier of the advanced semiconductors used in AI accelerators, has seen its revenues, margins, and market capitalization expand significantly in the last five years. TSMC now represents nearly 15% of the MSCI Emerging Markets Index. Additionally, South Korean companies Samsung and SK Hynix have become global leaders in memory semiconductors, particularly high-bandwidth memory chips, which are essential for training and operating large AI models. Samsung and SK Hynix constitute roughly 9% and 7% of the MSCI Emerging Markets Index, respectively.

This change in index leadership carries important implications for investors. Strong performance of a relatively small group of semiconductor companies has led to an uptick in concentration within passive emerging market funds and tied benchmark performance more closely to AI-related chip demand. The lower weighting of China in the index, meanwhile, reflects both weaker relative performance for Chinese companies and the broader investor preference for markets more directly connected to AI infrastructure spending. As a result of these trends, the MSCI Emerging Markets Index increasingly reflects advanced semiconductor leadership rather than the diversified growth of emerging economies, heightening both country- and company-specific risks. For instance, geopolitical tensions involving Taiwan, supply chain disruptions, or a meaningful slowdown in AI capital expenditures could materially alter recent performance trends. This dynamic reflects a broader shift in where value creation is occurring across emerging markets and is likely to persist as long as AI-related semiconductor demand remains strong.

A Renewed Focus on Renewables

In addition to the humanitarian toll of the conflict in Iran, the world is currently confronting the impact that trade disruptions in the Strait of Hormuz are having on energy markets. To this point, oil importing nations in Asia are bearing the brunt of these disruptions, with many of these countries instituting measures like school and work closures, transportation restrictions, and manufacturing cutbacks in order to save on fuel costs. These dynamics underscore the strategic importance of energy independence and could ultimately result in meaningful shifts in how various countries power their economies.

While the conflict may lead governments to see the value of diversifying energy sources in a new light, the search for alternatives to fossil fuels is not new. Along with environmental concerns, reliance on finite resources imposes limitations on power generation capacity. Those limits are at odds with groundbreaking technological advancements in artificial intelligence, which are propelled by infrastructure that requires vast amounts of energy to operate. As illustrated in the chart above, more than half of newly installed energy capacity in the last five years has come from renewable sources like solar and wind, and that share is still increasing. Countries like China and Brazil are leaders on this front, with 58% and 87% of their energy capacity additions coming from renewables last year, respectively. Opportunities for investment should continue to emerge as countries around the world commit capital to expanding renewable energy infrastructure, making this a trend worth monitoring for investors going forward.

Let’s Hear It for Latin America

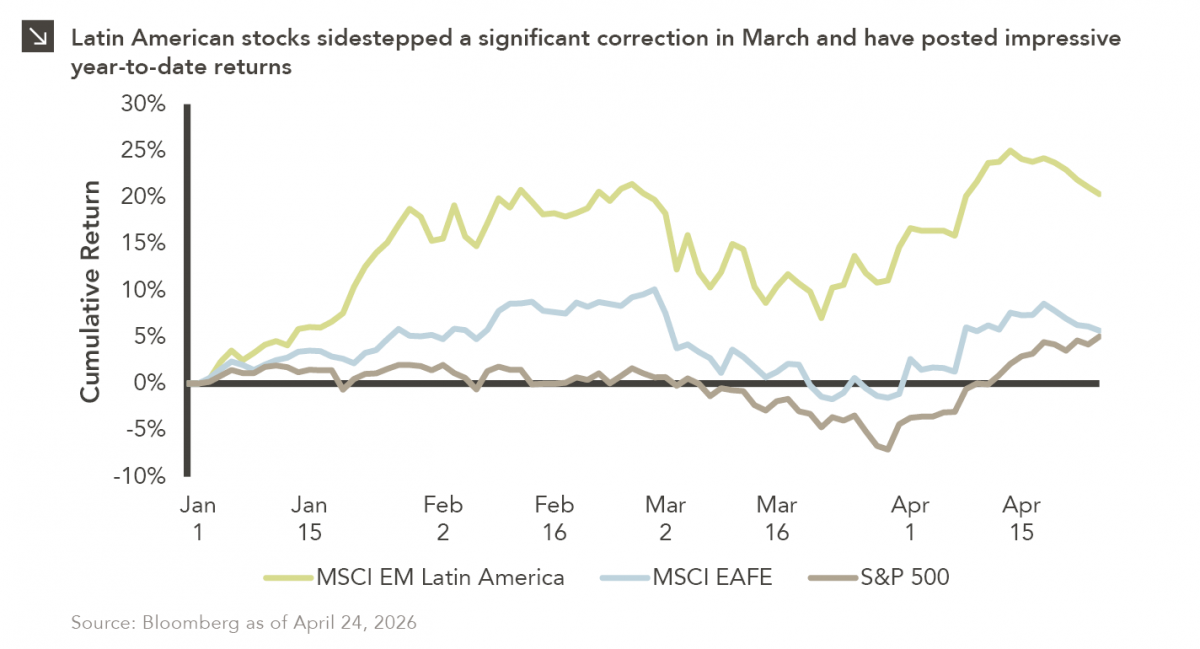

Latin American equity markets have shown remarkable strength in 2026. After a strong start to the year, the MSCI Emerging Markets Latin America Index corrected by only 4% in March amid a broad, more pronounced market pullback due in large part to the conflict in Iran. Brazil, which represents the largest economy in Latin America, was uniquely positioned to handle commodity market disruptions given its status as a net exporter of crude oil and a world leader in renewable energy utilization. Indeed, almost 90% of Brazilian electricity is generated via hydropower, wind, and solar sources, so the nation has been able to withstand recent energy shocks better than many other Western nations. The Central Bank of Brazil also cut interest rates for the first time in two years in March, though additional rate cuts that were anticipated at the start of this year are now more uncertain. Investors have also looked on Latin American financial institutions with favor in recent time, as banks across the region (e.g., Creditcorp in Peru, Itaú in Brazil, and Grupo Financiero Banorte in Mexico) are outperforming their global peers on a year-to-date basis due to attractive earnings projections. Additionally, significant foreign investment in the Brazilian economy has led to higher volumes and earnings for B3, the Brazilian stock exchange.

Global markets have stabilized in April, with the S&P 500 Index now trading near calendar year highs and developed international equities also exhibiting renewed strength. At the same time, Latin American equities have continued their upward trajectory, with the MSCI Emerging Markets Latin America Index now up more than 20% since the start of 2026. Following strong performance in 2025 and after having avoided a major drawdown in the wake of the Iran conflict, investors may want to keep a close eye on Latin American stocks as the year progresses.

We’ve Seen This Before

Diversify. Rebalance. Stay invested. Every one of these letters has concluded with that same advice in some shape or form. It’s not particularly shiny and new, but the best documented path to a successful long-term investment program. The last eight weeks are another data point in support of these practices.

In this edition:

- Impact of U.S.–Iran conflict on oil prices, interest rates, and equity markets

- Volatility and drawdowns in the market cycle

- Equity market rotation

- Magnificent 7 detraction and increased market breadth

- Slowdown in non-U.S. equities

Liberation Day: One Year Later

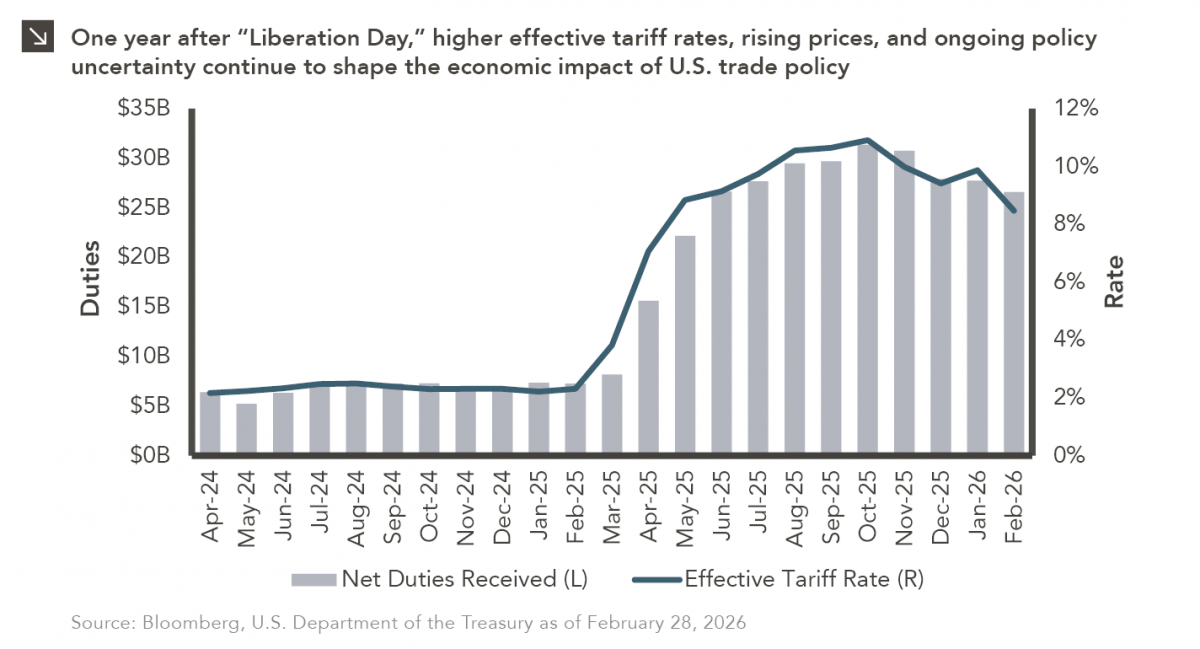

On April 2, 2025, President Donald Trump announced a sweeping set of tariffs on imports into the United States. Dubbed “Liberation Day,” the announcement marked one of the most significant shifts in U.S. trade policy in decades and initiated a period of heightened uncertainty across global supply chains and financial markets. One year later, it is useful to examine how markets and economic participants have navigated the resulting trade environment.

A key distinction when assessing the impact of tariffs is the difference between the policy tariff rate and the effective tariff rate (ETR). While the headline policy rate often attracts the most attention, the ETR provides a more accurate measure of economic impact. The ETR reflects the ratio of duties actually collected relative to the total value of imports entering the country. Because it incorporates supply-chain adjustments, exemptions, and technical exclusions, the effective rate tends to have a closer relationship with market outcomes than the stated policy rate.

Following Liberation Day, the monthly ETR rose sharply (from roughly 3% in March 2025 to approximately 7% in April 2025) before continuing higher and reaching a peak near 10.9% in October. By the end of February 2026, the rate had moderated but remained elevated at slightly above 8%. Over that period, the U.S. Treasury reported that the government collected approximately $295 billion in net customs duties. The administration highlighted a decline in the U.S. trade deficit of roughly 24% during the same time frame.

Another important concept is the tariff pass-through rate, which measures the extent to which higher tariffs translate into higher prices paid by businesses and consumers. Although tariff costs are shared across the global supply chain, they are not distributed evenly. Research from the Federal Reserve Bank of New York suggests that the majority of the tariff burden has fallen on U.S. importers, with estimates indicating that more than 85% of the incidence was borne domestically. Similar findings have been reported by the European Central Bank, which estimated that the pass-through to U.S. consumer prices reached roughly one-third in 2025 and could rise further if elevated tariff levels persist.

Federal Reserve officials have also acknowledged the inflationary implications of tariffs. During the FOMC press conference last month, Chair Jerome Powell noted that tariffs associated with Liberation Day had contributed to modestly higher inflation and that the full price effects could take additional time to materialize.

The policy landscape has continued to evolve. In February 2026, the U.S. Supreme Court ruled that the broad Liberation Day tariffs exceeded the administration’s authority under emergency powers, forcing the rollback of some measures and raising questions about potential tariff refunds. Nevertheless, the administration has since explored alternative legal pathways to maintain certain tariffs, underscoring that trade policy remains fluid.

As the economic effects of the original tariffs continue to unfold and as new trade measures are considered, global markets remain attentive to the evolving policy environment. One year after Liberation Day, tariffs continue to serve as a reminder that shifts in trade policy can carry meaningful economic consequences for businesses, consumers, and investors alike.

1Q 2026 Market Insights Webinar

This video is a recording of a live webinar held April 16 by Marquette’s research team analyzing the first quarter across the economy and various asset classes as well as themes we’ll be monitoring in the coming months.

Our quarterly Market Insights series examines the primary asset classes we cover for clients including the U.S. economy, fixed income, U.S. and non-U.S. equities, hedge funds, real assets, and private markets, with commentary by our research analysts and directors.

Featuring:

Greg Leonberger, FSA, EA, MAAA, FCA, Partner, Director of Research

James Torgerson, Senior Research Analyst

Fred Huang, Research Analyst

David Hernandez, CFA, Director of Traditional Manager Search

Evan Frazier, CFA, CAIA, Senior Research Analyst

Dennis Yu, Research Analyst

Hayley McCollum, Senior Research Analyst

Sign up for research alerts to be invited to future webinars and notified when we publish new videos.

If you have any questions, please send our team an email.

Pain at the Pump

Global energy costs have risen sharply this month due to a convergence of geopolitical shocks, as critical infrastructure and transport routes have been severely disrupted in the wake of U.S. strikes on Iran. Specifically, oil prices have climbed above $100 per barrel for the first time since 2022, while European gas futures have nearly doubled from late February levels. These developments have led to pain at the pump for many in the U.S., where the cost of a gallon of regular, unleaded gasoline has risen to more than $3.96 as of this writing. This figure represents a roughly 33% increase from the national average just one month ago.

It is hard to understate the importance of the Persian Gulf region to commodities markets, with the Strait of Hormuz alone typically handling around a quarter of seaborne oil and a significant share of liquefied natural gas (LNG) shipments. The effective closure of this waterway has choked off a vital artery for the global energy trade, and damage to the LNG export capacity of Qatar has further tightened markets. With shipping traffic in the region reduced or halted due to security risks, traders are now pricing in the possibility of prolonged energy shortages. The current situation is particularly acute because ongoing disruptions affect not just production but also the transportation of commodities that have already been produced, amplifying the supply squeeze. Additionally, oil producers in the Gulf have scaled back output as storage capacity reaches its limits, both on land and aboard tankers offshore. According to the International Energy Agency, production has been reduced by at least 10 million barrels per day, which represents more than half of the volume that typically passes through the Strait of Hormuz.

Beyond the immediate supply loss, markets are also responding to the risk of sustained or worsening disruption. Damage to key facilities (e.g., large-scale LNG processing plants) could take years to fully repair, raising the prospect of a prolonged imbalance between supply and demand. Meanwhile, continued military escalation increases the likelihood that additional infrastructure could be targeted. This uncertainty has led to a risk premium being embedded in prices, as buyers compete to secure alternative supplies and hedge against future shortages. In effect, the combination of physical damage, logistical bottlenecks, and geopolitical risk has created significant upward pressure on energy prices, with potential ripple effects across inflation, industrial activity, and global economic growth.

Seventy-Five Horses and Two Pieces of Plastic

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest powered by a 75-horsepower engine with two plastic skis to steer makes it hard to feel like one has complete control; 30 mph in the open air feels more like 100!

Nonetheless, operating a snowmobile is pretty straightforward: The throttle is a right-thumb button, the brake is a left-hand squeeze lever. Beyond those two controls, it’s up to the driver to effectively navigate the trail, with the critical concession that the terrain is out of anyone’s complete control. Which brings me to our 2026 market outlook.

The “throttles” for portfolios are the usual constituents: equities, below investment grade credit, and private markets. The “brakes” are investment grade fixed income, particularly Treasuries which can slow a portfolio’s losses if the market tumbles. The terrain is naturally the actual path that each of these asset classes will follow in 2026. Since 2022 the equity market ride has been mostly exhilarating, save for some of the terrifying moments like the market dip after Liberation Day. But that’s in the rearview mirror, and the focus is what is around the bend. Will the thrill continue, or should we ease up on the throttle?

2026 Market Preview

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the economy and various asset classes as well as themes we’ll be monitoring in 2026.

Our quarterly Market Insights series examines the primary asset classes we cover for clients including the U.S. economy, fixed income, U.S. and non-U.S. equities, hedge funds, real assets, and private markets, with commentary by our research analysts and directors.

Featuring:

Greg Leonberger, FSA, EA, MAAA, FCA, Partner, Director of Research

Frank Valle, CFA, CAIA, Associate Director of Fixed Income

James Torgerson, Senior Research Analyst

Catherine Hillier, Senior Research Analyst

David Hernandez, CFA, Director of Traditional Manager Search

Evan Frazier, CFA, CAIA, Senior Research Analyst

Dennis Yu, Research Analyst

Amy Miller, Associate Director of Private Equity

Chad Sheaffer, CFA, CAIA, Associate Director of Private Credit

Sign up for research alerts to be invited to future webinars and notified when we publish new videos.

If you have any questions, please send our team an email.