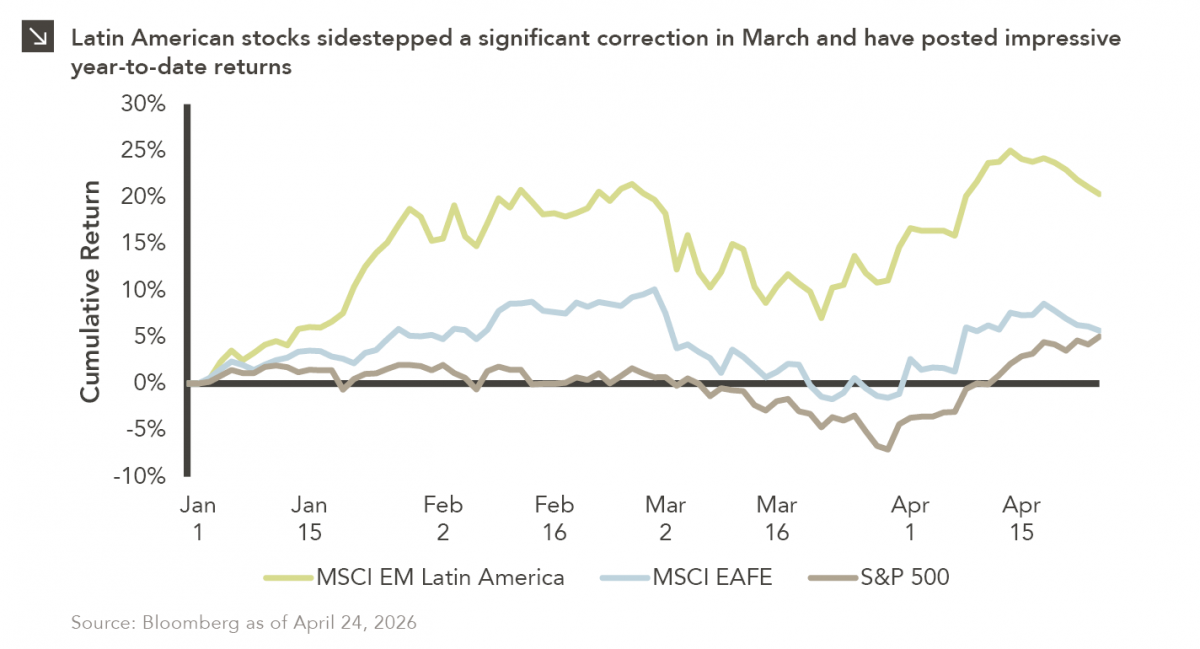

Latin American equity markets have shown remarkable strength in 2026. After a strong start to the year, the MSCI Emerging Markets Latin America Index corrected by only 4% in March amid a broad, more pronounced market pullback due in large part to the conflict in Iran. Brazil, which represents the largest economy in Latin America, was uniquely positioned to handle commodity market disruptions given its status as a net exporter of crude oil and a world leader in renewable energy utilization. Indeed, almost 90% of Brazilian electricity is generated via hydropower, wind, and solar sources, so the nation has been able to withstand recent energy shocks better than many other Western nations. The Central Bank of Brazil also cut interest rates for the first time in two years in March, though additional rate cuts that were anticipated at the start of this year are now more uncertain. Investors have also looked on Latin American financial institutions with favor in recent time, as banks across the region (e.g., Creditcorp in Peru, Itaú in Brazil, and Grupo Financiero Banorte in Mexico) are outperforming their global peers on a year-to-date basis due to attractive earnings projections. Additionally, significant foreign investment in the Brazilian economy has led to higher volumes and earnings for B3, the Brazilian stock exchange.

Global markets have stabilized in April, with the S&P 500 Index now trading near calendar year highs and developed international equities also exhibiting renewed strength. At the same time, Latin American equities have continued their upward trajectory, with the MSCI Emerging Markets Latin America Index now up more than 20% since the start of 2026. Following strong performance in 2025 and after having avoided a major drawdown in the wake of the Iran conflict, investors may want to keep a close eye on Latin American stocks as the year progresses.