06.22.2026

The VC Convergence Era

When Benchmark, one of Silicon Valley’s most renowned early-stage venture capital firms, closed $2 billion across two new funds this…

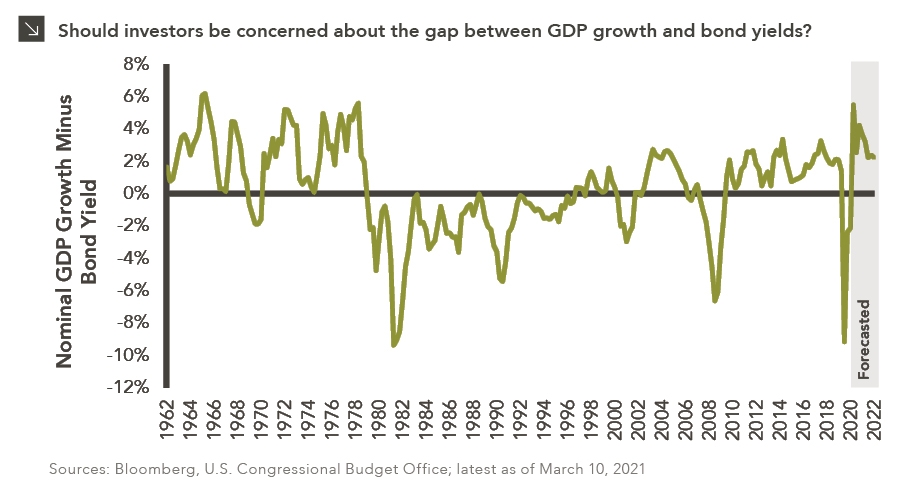

The gap between U.S. GDP growth and bond yields is expected to rise to the highest level since the 1970s amid unprecedented amounts of fiscal and monetary stimulus and an accelerating vaccination roll-out. The chart depicts nominal U.S. GDP growth rates year-over-year less the 10-year U.S. Treasury yield over the last 60 years. Beyond 2020, we profile the U.S. Congressional Budget Office (“CBO”) forecasted nominal GDP growth rate for 2021 and 2022, minus the forecasted 10-year U.S. Treasury yield from the Treasury forwards market, which projects a 25 basis point rise each year over the next four years.

The quarterly GDP growth rate is much more volatile than bond yields. It can decline precipitously in a recession much faster than bond yields as well as rebound much faster than bond yields in a recovery. The ratio has spiked down several times in the past: during the early 1980s and early 1990s recessions, following the dot-com bust of 2000 and the housing bust of 2008, and most recently after the COVID panic of March 2020. This is because the GDP growth rate reflects actual economic growth, measured year-over-year quarterly, while bond yields reflect the market’s anticipation of economic growth over a longer time period. While this gap is expected to reach its highest level in roughly 50 years as the economy rebounds from the depths of COVID, it is then expected to moderate back to pre-pandemic levels, as the CBO forecasts GDP growth to normalize throughout 2021 and 2022 after the initial recovery. Therefore, despite the spike in this ratio it is not a fundamental concern for investors and is not suggestive of a coming market downturn.

Print PDF > GDP Growth Hits Highs vs. Bond Yields

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

06.22.2026

When Benchmark, one of Silicon Valley’s most renowned early-stage venture capital firms, closed $2 billion across two new funds this…

06.15.2026

The rapid buildout of artificial intelligence infrastructure is reshaping the U.S. investment landscape. According to recent Census Bureau data, spending…

06.08.2026

Hi, James Torgerson here! Volatility can be an unsightly blemish on portfolios and lead to inferior risk-adjusted returns. Private credit…

06.01.2026

The MSCI Emerging Markets Index has undergone a significant structural transformation in recent years. For much of the past decade,…

05.26.2026

The classic novel A Tale of Two Cities by Charles Dickens begins with the line “It was the best of…

05.18.2026

Over the last few years, equity markets have been defined by a group of stocks often referred to as the…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >