Ryan Maher

Associate Client Analyst

Get to Know Ryan

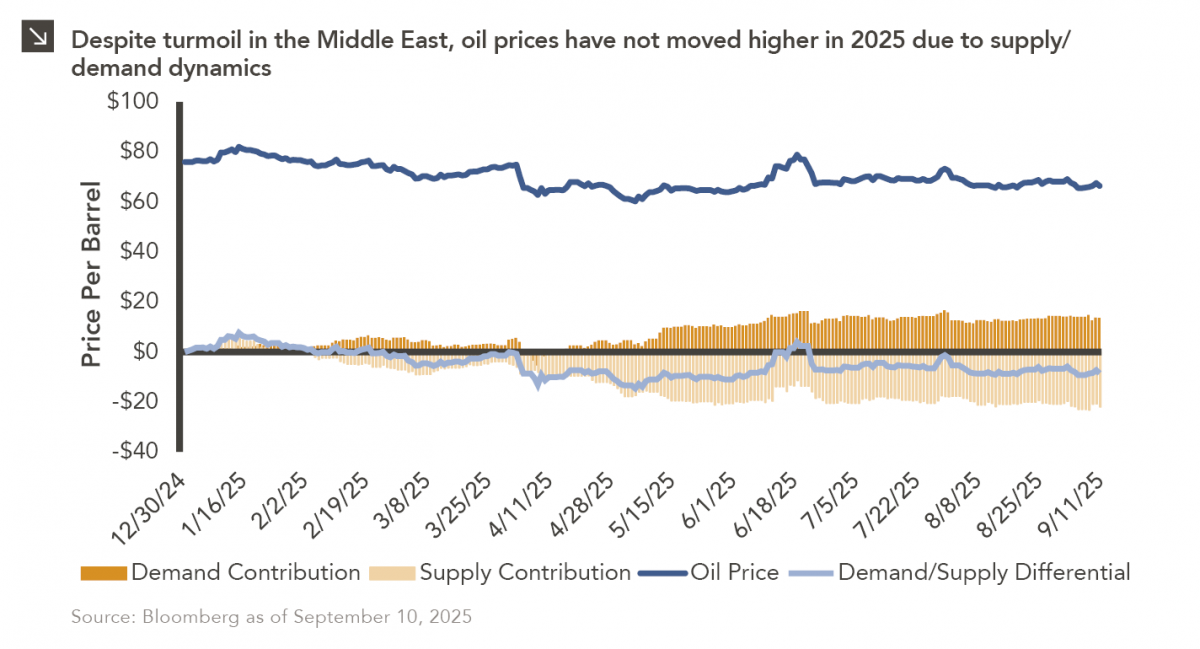

Earlier this year, Marquette published a Chart of the Week that detailed the muted change in oil prices in the aftermath of U.S. strikes on Iranian nuclear facilities. Tensions in the region have persisted in recent time, with last week seeing Israeli airstrikes that targeted Hamas leadership in Qatar. In response to this development, oil ticked higher as investors assessed the increased risk of commodity supply chain disruptions but later gave back most of these gains. This represents a continuation of the trend exhibited during most of 2025, in which geopolitical shocks do not materially increase the price of oil. One possible explanation for this dynamic would be persistently elevated supply of the commodity.

As displayed in the chart above, there has been a sustained imbalance between oil supply and demand for most of the last six months, with supply outpacing demand. Indeed, OPEC+, which includes the Organization of Petroleum Exporting Countries, Russia, and other allied producers, has moved to aggressively raise output in 2025, which has resulted in a production capacity increase of over two million barrels per day since April. Despite this already increasing supply, OPEC+ recently made an agreement to add an additional 137,000 barrels per day to its production capacity in October. These increases in capacity have significantly outpaced global demand, driving prices lower and widening the oil supply glut. Going forward, while geopolitical instability may support temporary price increases, the longer-term outlook for oil remains clouded by excess supply and uncertainty surrounding future consumption of the commodity.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.27.2026

The rapid growth of non-traded business development companies (BDCs), which are investment vehicles that pool investor capital to make loans…

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >