08.03.2026

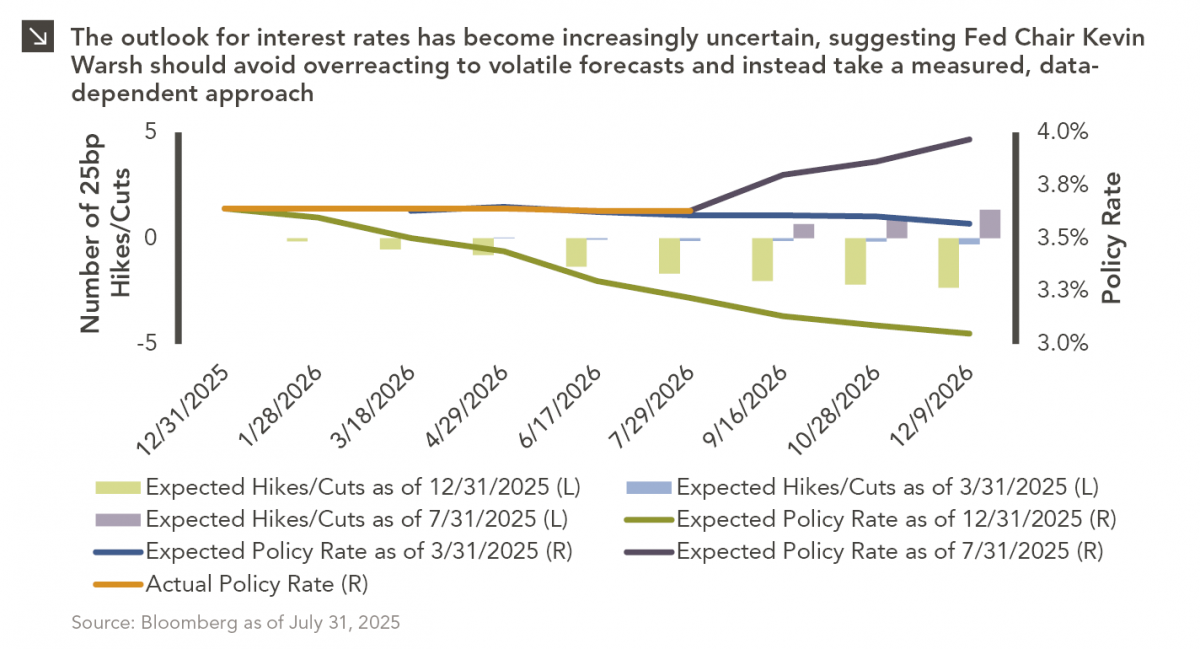

Hit the One in the Middle, Mr. Chairman!

In the cinematic masterpiece Rocky IV, Rocky gets dazed by his opponent, Captain Ivan Drago, and complains that he sees…

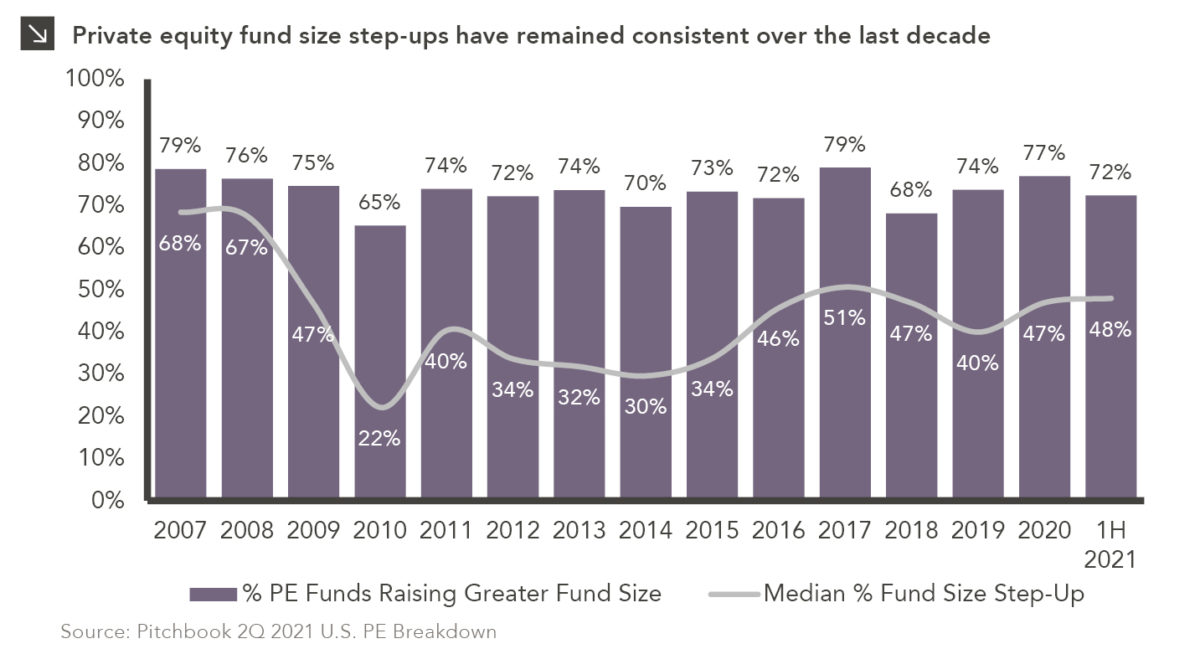

Despite strong fundraising numbers in recent years, private equity managers in the U.S. have stayed consistent with subsequent fund size step-ups. Through the first half of 2021, 72% of private equity managers launched funds with increased size targets, in line with the average over the last decade. The median fund size step-up in the first half of the year was 48%, modestly above the 40% average increase over the last decade, but in line with the industry average over the last five years.

Fund size is a critical factor for private equity investors to consider, as it can push a manager outside their strategy, require additional resources, require purchasing larger businesses that are more efficient, and/or take managers longer to deploy. That said, modest fund size growth is healthy for a private equity organization, allowing for internal growth, giving existing investors the ability to scale their allocations, and creating opportunities to bring new investors into the fund. Risks related to increased fund size can be mitigated by managers via scaled resources, targeting more portfolio companies, reducing the amount of co-investment offered, and/or reducing leverage — all things we look for in our due diligence process. We believe modest growth is healthy and to be encouraged if done responsibly, but we do carefully evaluate the magnitude of a fund size increase relative to our assessment of a manager’s capacity and strategy.

Print PDF > Private Equity Staying Rational with Fund Sizes

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

08.03.2026

In the cinematic masterpiece Rocky IV, Rocky gets dazed by his opponent, Captain Ivan Drago, and complains that he sees…

07.27.2026

The rapid growth of non-traded business development companies (BDCs), which are investment vehicles that pool investor capital to make loans…

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >