Jessica Noviskis, CFA

Portfolio Strategist, OCIO Services

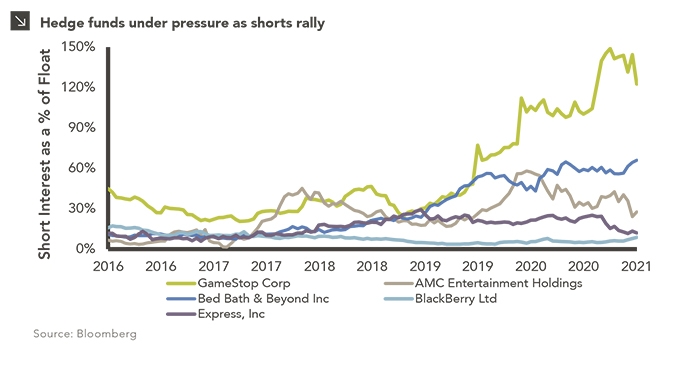

A group of small-cap stocks made big waves last week as retail day traders collaborated online to drive up certain stock prices in order to “squeeze” hedge funds with short positions. The influence of the retail investor has been building for over a year, facilitated by reduced trading fees, new brokerage platforms, and the time and money freed up by COVID lockdowns, but the Reddit-documented campaigns to manipulate GameStop and others brought forth entirely new dynamics.

Hedge funds take short positions when they expect stock prices to fall, generally for fundamental reasons. Short positions are inherently more risky than long positions — the downside is theoretically unlimited and short positions will increase in size as the stock moves against you, but prudent long/short managers understand these risks and typically run short portfolios that are more diversified, with smaller position sizes and tighter risk management parameters. Market sentiment and positioning is a key part of their analysis, especially on the short side. Stocks with high short interest have been red flags for many managers well before the term “Gamestonk” existed.

GameStop, AMC, Bed Bath & Beyond, and other stocks being irrationally bid up have fundamentally struggled for years. Outdated business models have led to earnings declines and multiple compression, and the impact of COVID has pulled forward bankruptcy concerns. At the same time, short interest has increased, and profitably — for the three years ending June 30th, 2020, the five stocks in the chart above lost on average 59% of their value. Over the last seven months, through the end of January, the worst performer of the group has almost tripled, and GameStop is up more than 7,000%, despite a largely unchanged fundamental outlook.

A number of hedge funds holding these higher short interest stocks were significantly impacted. At the center of the drama, Melvin Capital was reportedly down more than 50% for the month. While many hedge funds did not have direct exposure, the broader issue for the group and investors is the related de-grossing — long selling and short covering — as managers look to reduce exposure to the volatility. While de-grossing is not unusual (seen most recently in March 2020, September 2019, the fourth quarter of 2018), it has been especially rapid over the last week with hedge funds coming into the year with above average levels of gross and net leverage. While this has a created a tough backdrop for hedge fund alpha, especially coming off a record year in 2020, year to date losses have been modest. Through January, the average U.S. long/short fund was down just 2.3%,¹ relative to the S&P 500 -1.0%.

While Melvin Capital and others have publicly stated that they have fully closed out short positions on GameStop, the damage has been done, and these funds will likely face ongoing investor scrutiny over their risk management processes. But the majority of long/short funds should be able to make up any early year losses, with 2021 set up to be a good year for stock pickers. Prudent managers are re-underwriting their short positions, reducing exposure to potential targets and names with higher short interest, and many are patiently planning for the inevitable next leg. Stocks do not typically remain this severely disconnected from fundamentals for long, and at these valuations could present strong short opportunities.

¹ Morgan Stanley Prime Brokerage

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

06.15.2026

The rapid buildout of artificial intelligence infrastructure is reshaping the U.S. investment landscape. According to recent Census Bureau data, spending…

06.08.2026

Hi, James Torgerson here! Volatility can be an unsightly blemish on portfolios and lead to inferior risk-adjusted returns. Private credit…

06.01.2026

The MSCI Emerging Markets Index has undergone a significant structural transformation in recent years. For much of the past decade,…

05.26.2026

The classic novel A Tale of Two Cities by Charles Dickens begins with the line “It was the best of…

05.18.2026

Over the last few years, equity markets have been defined by a group of stocks often referred to as the…

05.11.2026

In addition to the humanitarian toll of the conflict in Iran, the world is currently confronting the impact that trade…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >