Jessica Noviskis, CFA

Portfolio Strategist, OCIO Services

While not as commonly dissected as earnings and multiples, liquidity is a key driver of equity markets. An influx of liquidity set up both the tech and real estate bubbles, which burst as that capital dried up, leading to severe market corrections in the early 2000s and in 2008. The easy credit environment that followed the Global Financial Crisis facilitated one of the longest and strongest bull markets in U.S. history. An unprecedented amount of stimulus injected into the financial system amid the COVID pandemic led to the sharpest stock market upturn on record. And now in 2023, amid an increase in liquidity and despite heightened macro uncertainties, a hawkish Fed, and a banking crisis, the S&P 500 is up 14%¹ nearing the end of the second quarter while the CBOE Volatility Index (VIX) has retreated to below-average levels.

¹Through June 27, 2023

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

06.15.2026

The rapid buildout of artificial intelligence infrastructure is reshaping the U.S. investment landscape. According to recent Census Bureau data, spending…

05.26.2026

The classic novel A Tale of Two Cities by Charles Dickens begins with the line “It was the best of…

05.18.2026

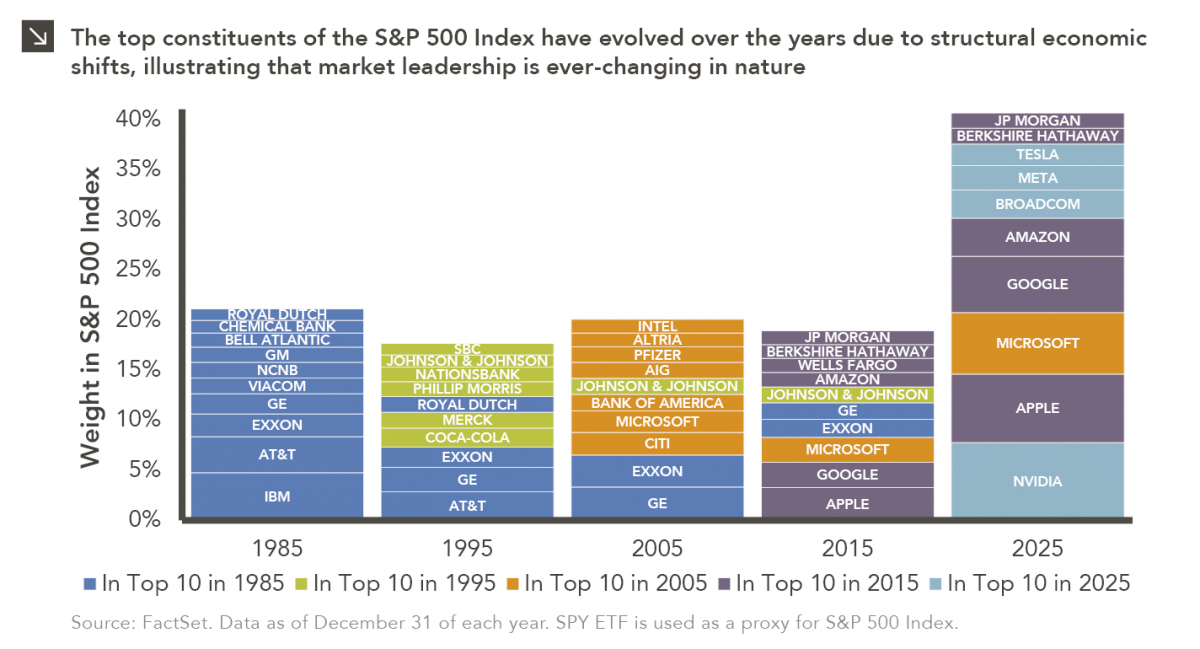

Over the last few years, equity markets have been defined by a group of stocks often referred to as the…

05.11.2026

In addition to the humanitarian toll of the conflict in Iran, the world is currently confronting the impact that trade…

05.07.2026

The leadership structure of the Federal Reserve is intentionally designed to promote continuity, independence, and institutional stability across political cycles….

05.04.2026

Rooted in medieval Persian Sufi thought, the adage “this too shall pass” speaks to the fleeting and impermanent nature of…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >