Weston Whalen, CFA

Associate Research Analyst

Get to Know Weston

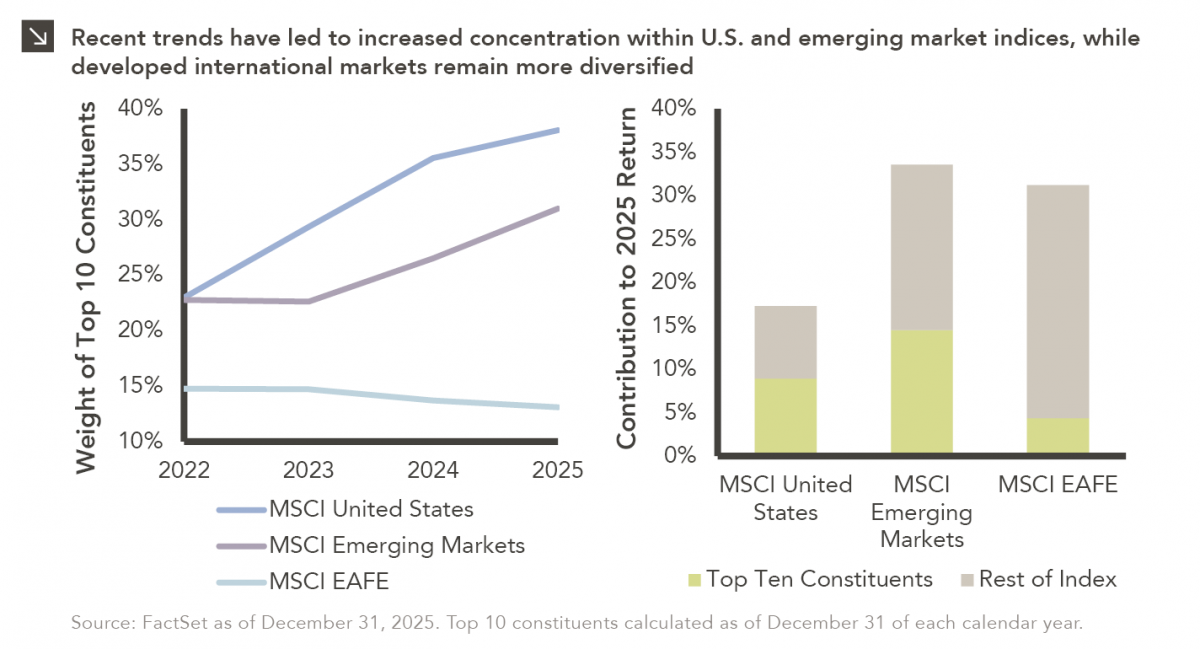

Last week, Alphabet joined NVIDIA, Microsoft and Apple as the only companies to ever reach a market capitalization of $4 trillion. The growth of these and other U.S. mega-cap technology companies has completely changed the composition of indices that measure the domestic equity market. Indeed, the weight of the top 10 constituents of the MSCI United States Index (which is comprised of large- and mid-cap stocks) sat at roughly 23% just three years ago. At the end of last year, however, that figure sat closer to 38%. As can be seen above, this concentration has resulted in a handful of stocks driving a significant share of overall index returns in recent periods. Interestingly, the theme of market concentration is not exclusive to domestic indices. For instance, companies in China, Taiwan, and South Korea have helped provide the materials required for the artificial intelligence boom, and the growth of these businesses has led to higher levels of concentration for the MSCI Emerging Markets index. The top 10 constituents now represent slightly less than one-third of this index, and TSMC, the largest producer of semiconductors in the world, notably comprises roughly 12% of the benchmark. Similar to trends within domestic markets, these top constituents had an outsized impact on the return of the MSCI Emerging Markets Index in 2025.

Interestingly, the MSCI EAFE Index, which is comprised of non-U.S. developed markets large- and mid-cap stocks, has not followed these same trends, with the weight of its top 10 constituents actually decreasing in recent years. While its largest holding is ASML, a supplier for the semiconductor industry, this benchmark is not nearly as heavily tilted towards the AI boom as domestic and emerging markets indices. For this reason, developed international markets could be a stronger source of diversification for investors moving forward.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.07.2026

JULY 23 — 1:00pm CT Please join Marquette’s research team for our 2026 Halftime Market Insights Webinar…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >