Nat Kellogg, CFA

President

Much has been made of the low bond yields on risk-free U.S. government debt. The yield on 10-year government debt dropped to just 1.7% as of May 18th. Many investors assume that if rates stay where they are today bond returns will be less than 2% over the coming years. However, this ignores both the steepness of the yield curve and the fact that most institutional investors maintain a fairly constant duration in their bond portfolios. This chart shows the current yield curve (red line) and the expected return an investor can expect to achieve owning government bonds at each maturity along the curve, assuming they maintain a constant duration. As the chart shows, investors in 10-year bonds will earn almost double the 1.7% return indicated by the yield curve if rates remain unchanged.

While this may come as a surprise, the math is fairly straightforward. An investor that buys a 10-year U.S. government bond today will pay $100.47 and receive a $1.75 coupon. The 10-year risk free interest rate is 1.70% and the 9-year risk free rate is 1.51%. This means that one year from now our investor owns a 9-year bond that pays a $1.75 coupon. However, because the current market interest rate for a 9-year risk free bond is 1.51%, the bond has appreciated to $101.99. To maintain the duration of the investment, our investor sells the 9-year bond at $101.99 and buys a new 10-year bond. Since rates have not changed a 10-year bond still sells for $100.47. Our investor’s total return is thus:

($101.99+$1.75)/$100.47 = 3.25%

This simple illustration and the implications for an institutional portfolio are discussed in greater detail in Marquette’s April 2011 Investment Perspectives “Short Duration vs. Core Bonds in a Rising Rate Environment”. Currently, the yield curve is predicting a fairly substantial rise in interest rates a few years in the future. However, if such a rise does not materialize and the current low rate environment persists, bond returns may once again exceed expectations.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

01.26.2026

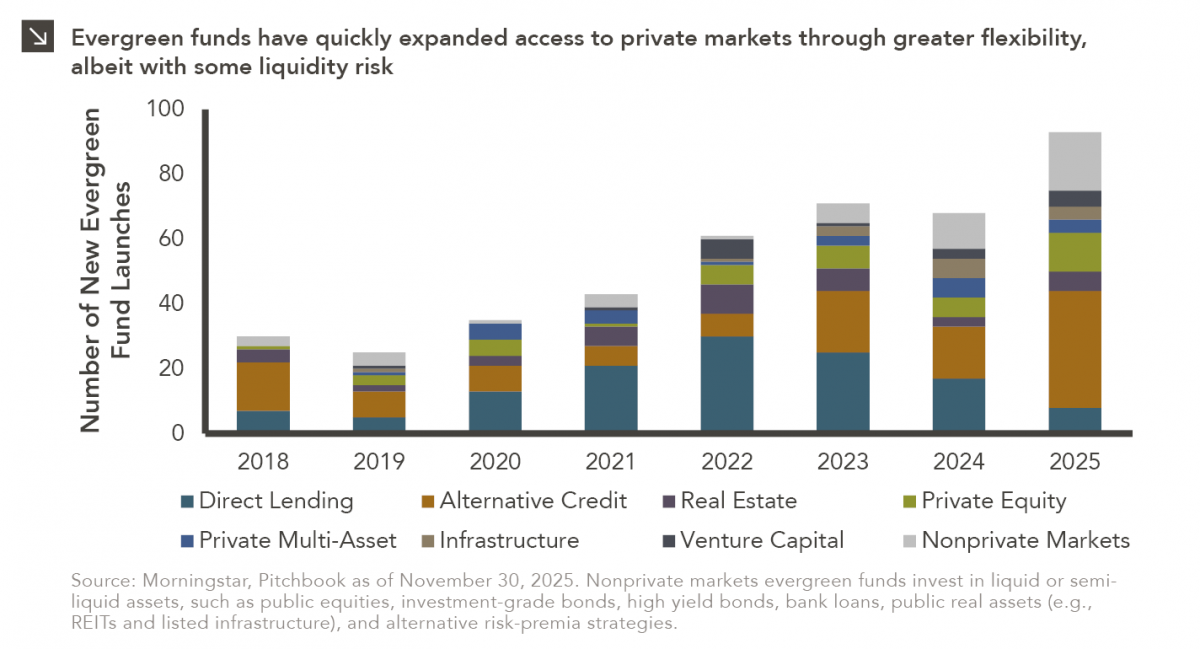

In recent years, access to traditionally illiquid private markets has expanded through the rapid growth of evergreen funds, which provide…

01.22.2026

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest…

01.20.2026

Last week, Alphabet joined NVIDIA, Microsoft and Apple as the only companies to ever reach a market capitalization of $4…

01.07.2026

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the…

01.14.2026

Contrary to widespread belief, fixed income aggregate strategies offer a continuum of active risk and return profiles. While aggregate strategies…

01.12.2026

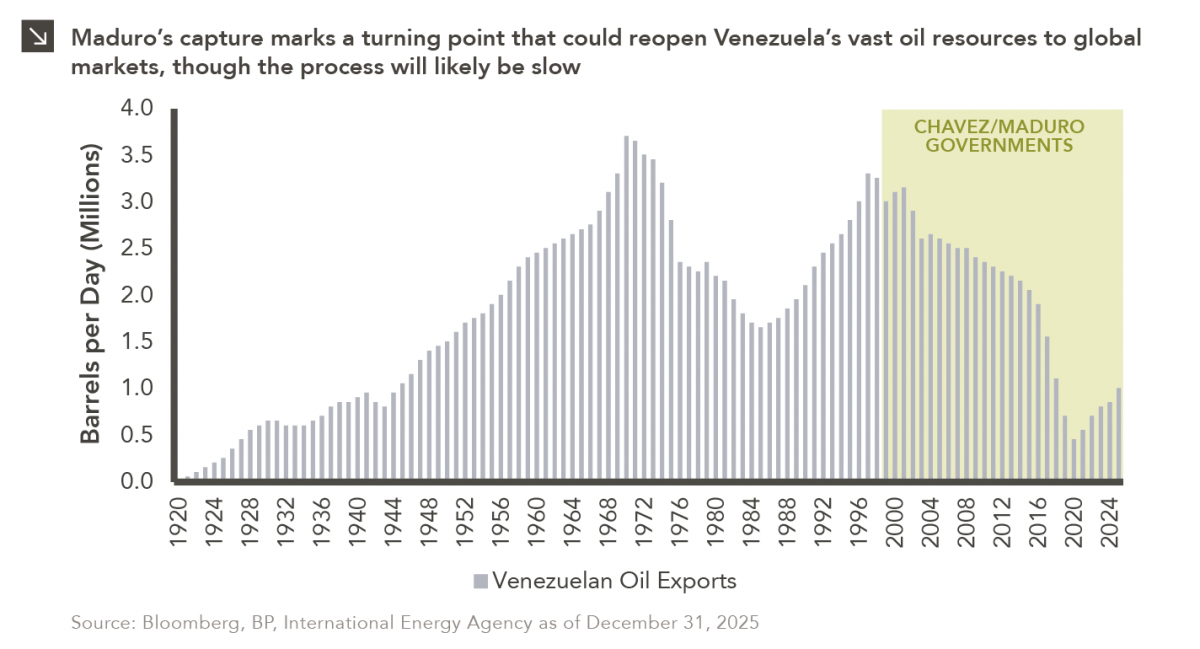

The capture of Venezuelan president Nicolás Maduro is a watershed moment for a country whose natural resource economy has been…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >