David Hernandez, CFA

Director of Traditional Manager Search

This week’s chart examines the change in yield for global sovereign debt. While we have been in a low interest rate environment since 2008, over the last three years, we have seen negative yielding bonds move from 0% of the developed bond universe to 38%. A staggering number indeed, this has been the by-product of anemic global growth and aggressive monetary policies in Europe and Japan.

One of the consequences of a negative rate environment is increased demand for higher yielding assets. Through the second quarter, U.S. high yield and emerging market debt have returned 9.1% and 10.3%, respectively. In addition to attractive yields, these asset classes have benefitted from stability in commodity prices and minimal exposure to the Brexit event. Should these conditions persist going forward, expect investor preference for credit and higher yielding bonds to continue, given this historically low interest rate environment.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

12.01.2025

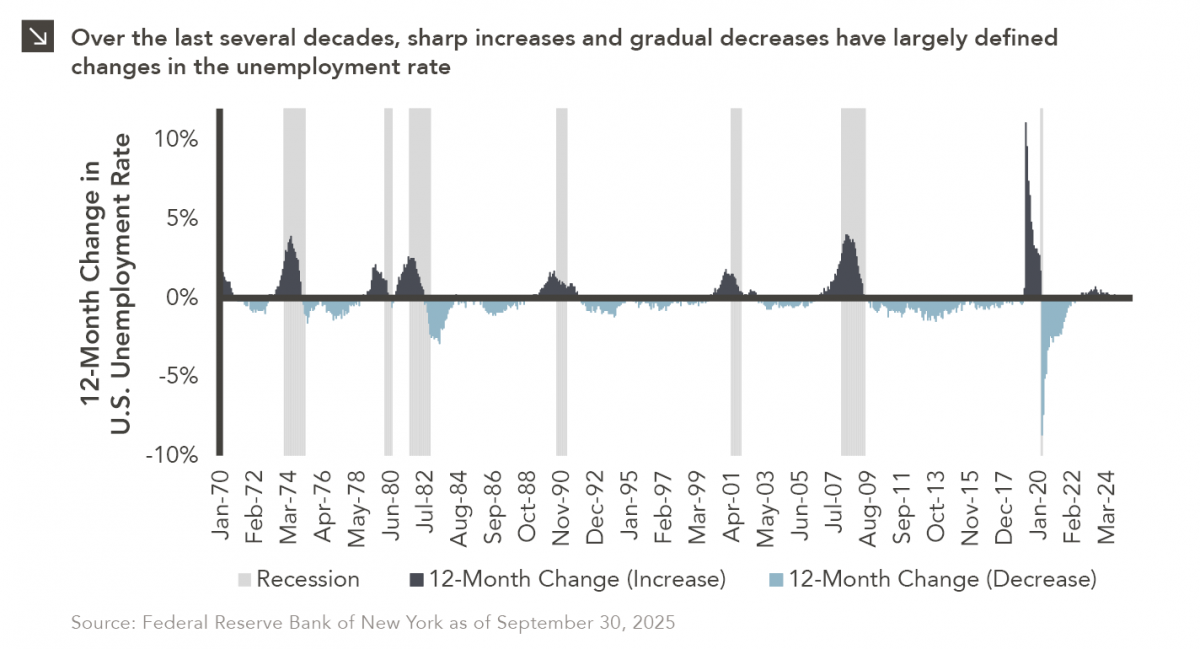

A fundamental characteristic of U.S. labor markets is the pronounced asymmetry in unemployment dynamics, as joblessness rises anywhere from three…

11.24.2025

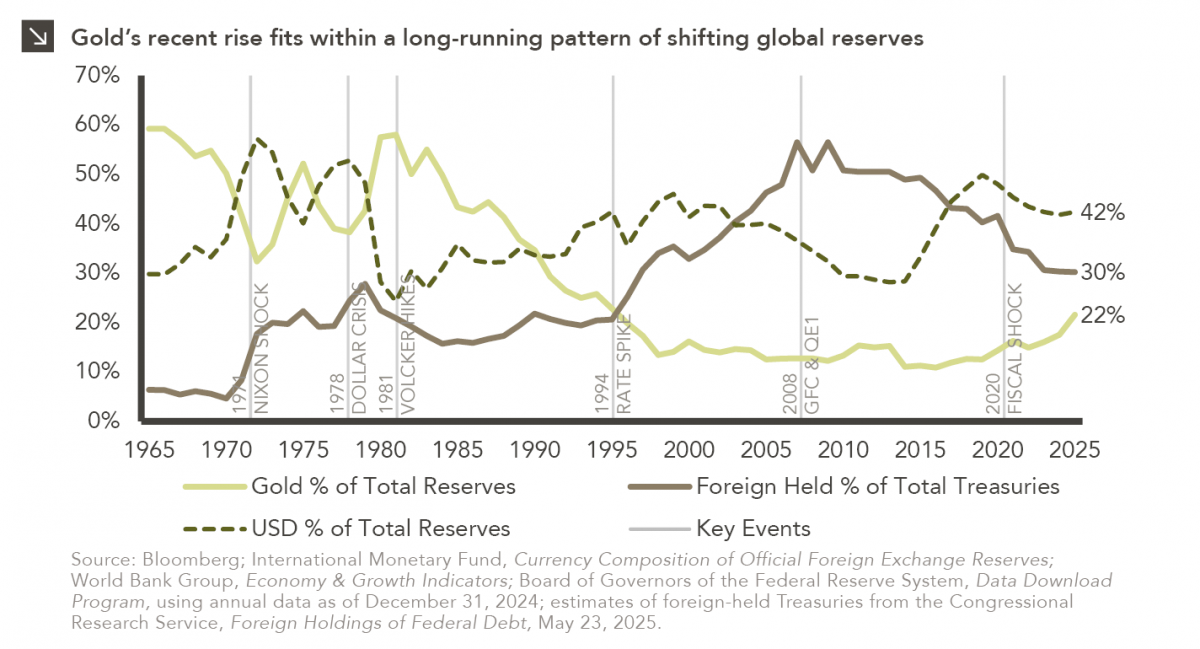

With gold now trading near $4,000 per ounce after a steady multi-year climb, investor attention has turned to the potential…

11.17.2025

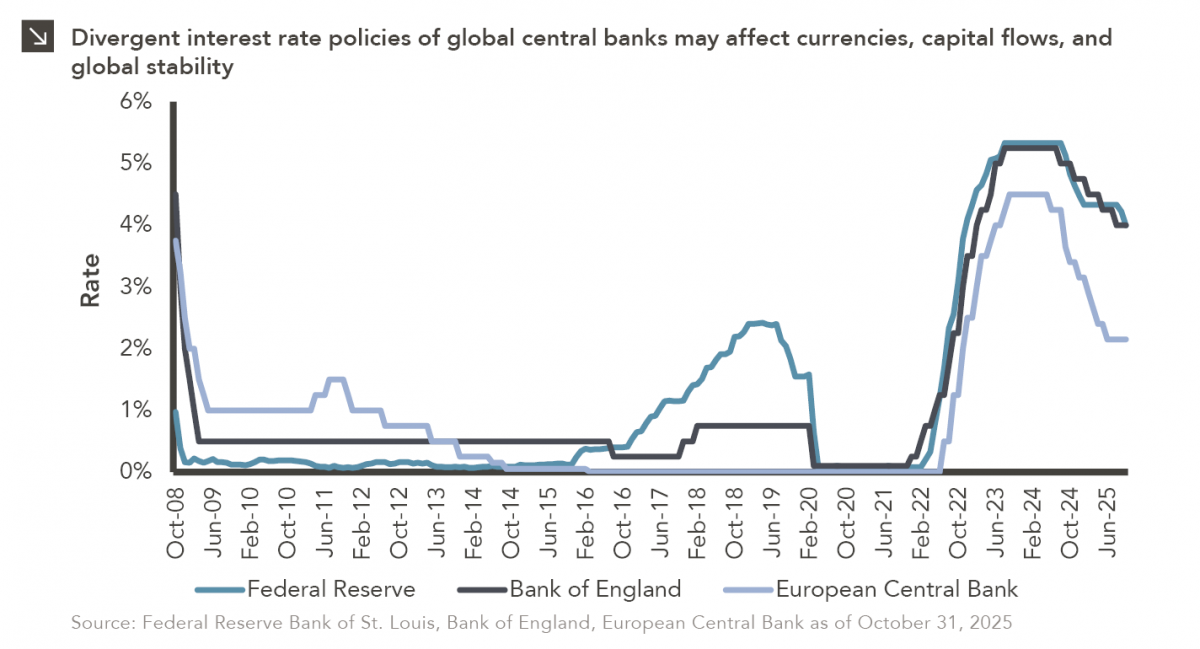

After a largely synchronized hiking cycle beginning in 2022, there has been a slight divergence in interest rate policies across…

11.10.2025

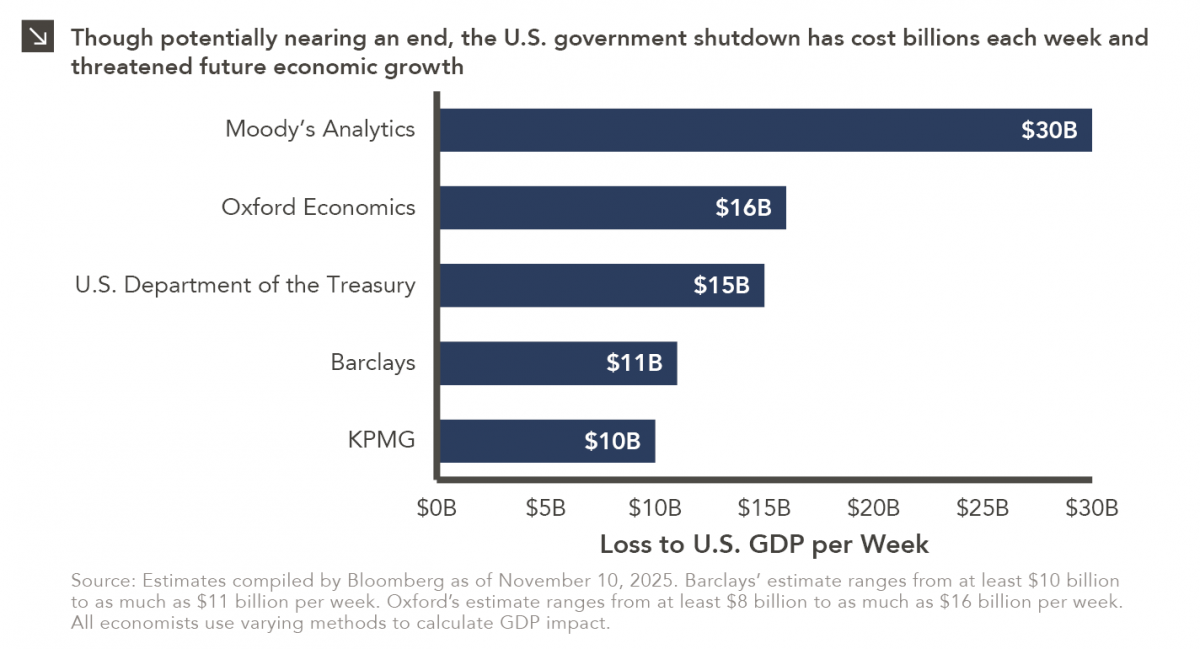

Over the weekend, the Senate overcame a key procedural obstacle in its attempt to end the record-breaking government shutdown, as…

11.03.2025

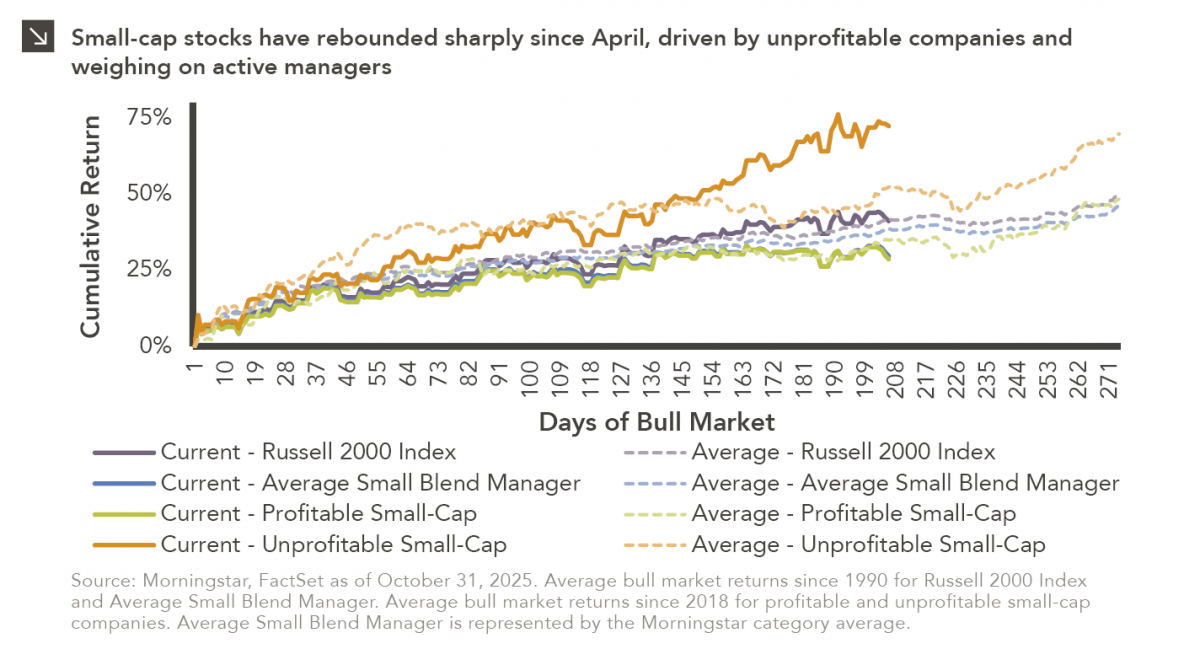

Small-cap equities are in a prolonged period of underperformance relative to large-cap stocks, but this trend has shown early signs…

10.27.2025

To paraphrase a quote from former President George W. Bush: “Fool me once, shame on… shame on you. Fool me…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >