Amy Miller

Associate Director of Private Equity

In investment management, asset allocators and their advisors frequently revisit the concept of portfolio diversification — whether by geography, market capitalization, security, or industry. While Marquette advocates for a diversified portfolio within private markets, it is important to recognize that not all diversification strategies are equally effective. Certain industry characteristics make specific sectors more attractive for private investments, particularly those that exhibit sustainable growth driven by favorable demographic or secular trends, fragmentation, capital constraints, and market inefficiencies. These features are often advantageous in private markets as they create opportunities for value enhancement and potential alpha generation.

Within the private equity asset class, five core sectors — what we refer to as the “magnificent five” — have consistently dominated merger and acquisition activity over the past six years. These sectors are healthcare, technology, industrials, business services, and financial services. According to Dealogic, over 60% of deals across 13 tracked industries have been concentrated within these five sectors, as measured by transaction count. Moreover, these industries have outperformed relative to top-quartile multiple on invested capital (MOIC). It is therefore logical that private equity managers would focus their capital in areas with higher probabilities of outsized returns, which in turn shapes the composition of investor portfolios. It is also important to note that this concentration also intensifies competition for deals within these sectors.

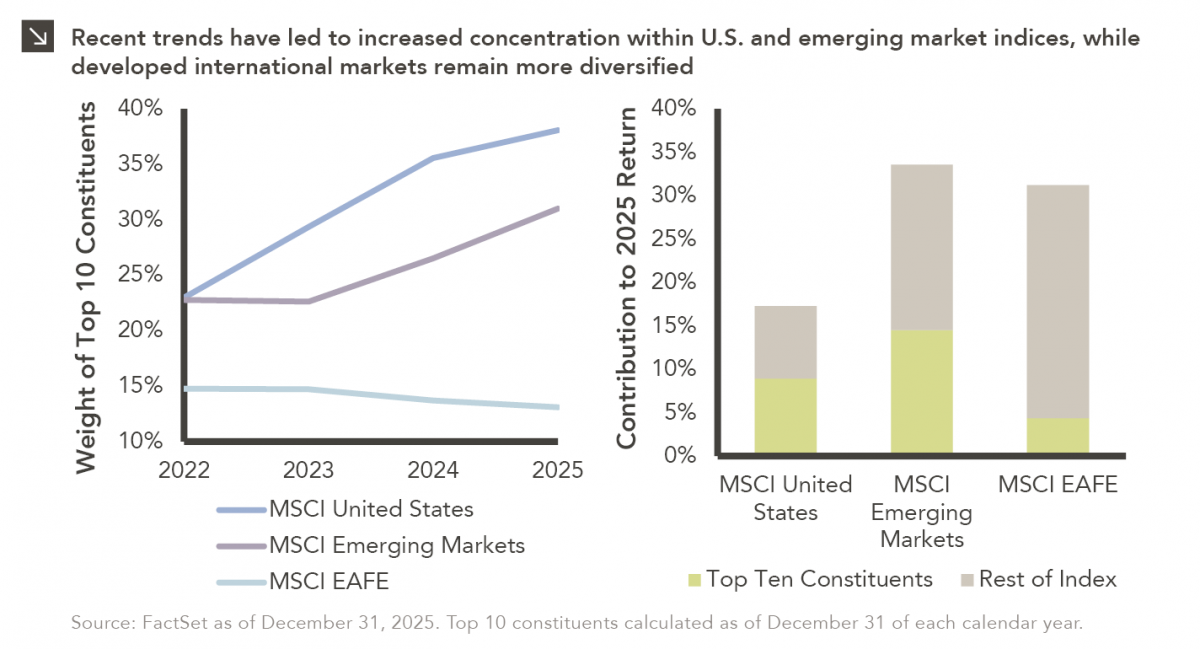

A critical point to consider is the dispersion of returns between top and bottom quartiles across industries — the wider the dispersion, the greater the risk. It is no surprise that the highest-performing industries, healthcare and technology, are often heavily represented in private equity portfolios. In this competitive and risk-laden environment, particularly within the private equity asset class, manager selection becomes increasingly crucial for investors seeking to achieve superior outcomes.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

02.02.2026

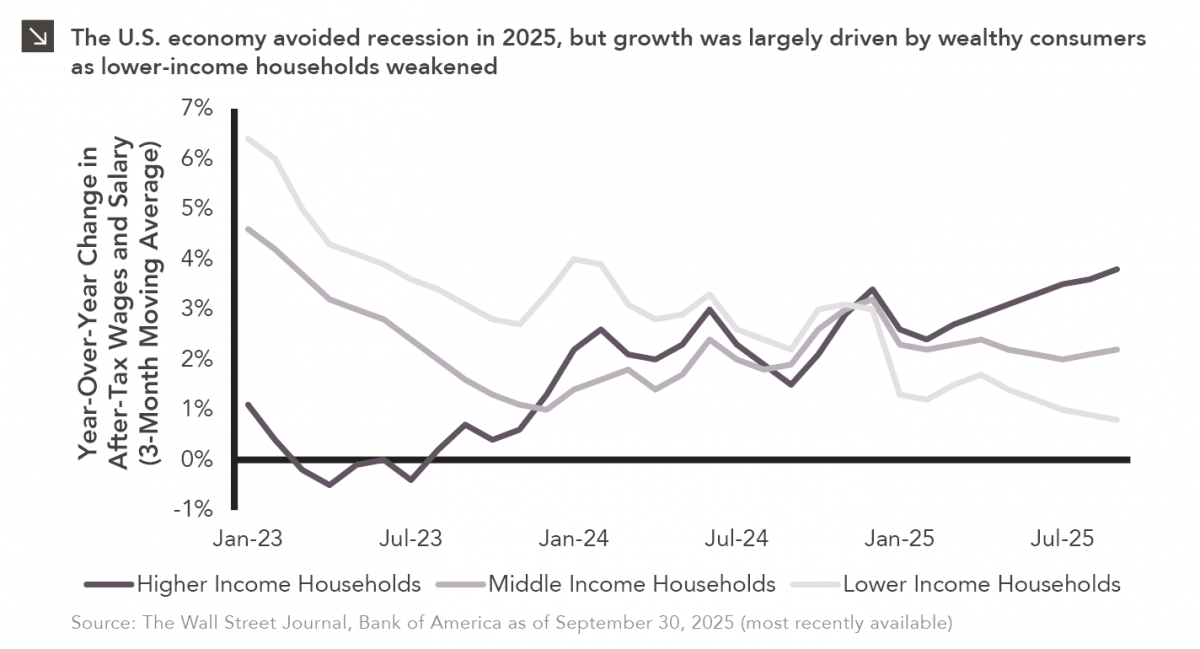

Macroeconomic forecasting is challenging in the best of times and proved downright impossible in 2025, which saw high levels of…

01.26.2026

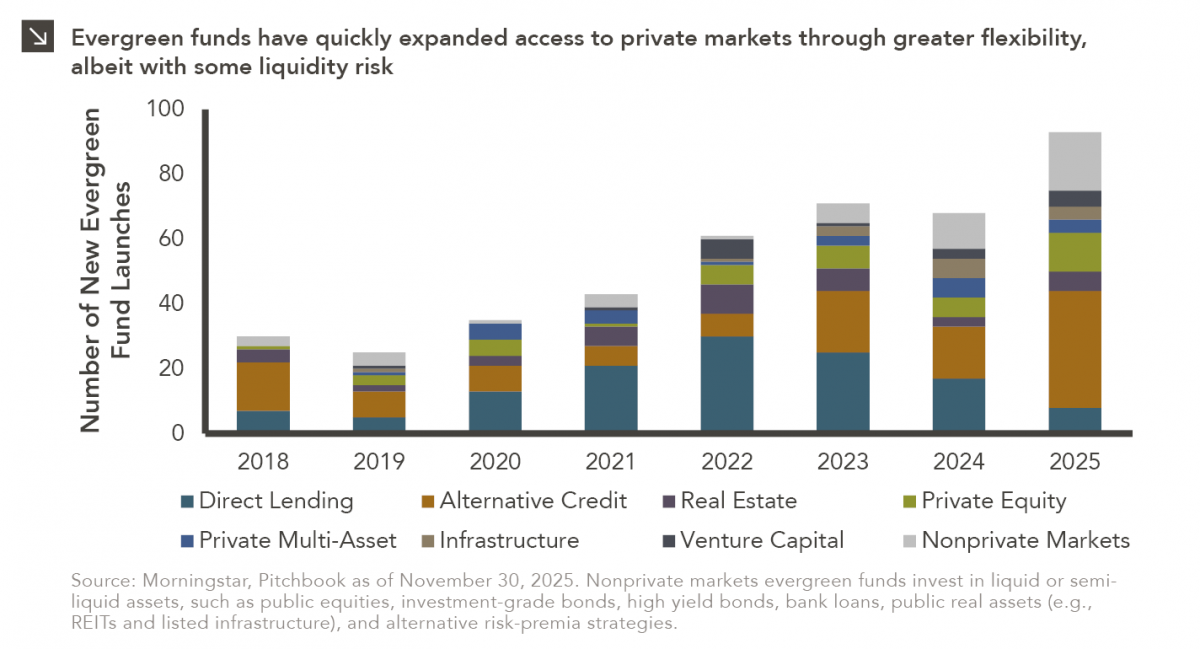

In recent years, access to traditionally illiquid private markets has expanded through the rapid growth of evergreen funds, which provide…

01.22.2026

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest…

01.20.2026

Last week, Alphabet joined NVIDIA, Microsoft and Apple as the only companies to ever reach a market capitalization of $4…

01.07.2026

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the…

01.14.2026

Contrary to widespread belief, fixed income aggregate strategies offer a continuum of active risk and return profiles. While aggregate strategies…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >