Greg Leonberger, FSA, EA, MAAA, FCA

Partner, Director of Research

Any ride on the London Tube reminds riders to mind the gap: Beware the space between train car and platform as you board and depart the train. A recent trip to London brought this phrase back to me and it seemed like a perfect description of how to look at financial markets this year, with the “gap” serving as the difference between expectations and reality, most particularly in terms of interest rate cuts.

In our market preview, we identified the Fed pivot as a primary driver of financial markets this year, most especially how expectations of cuts would line up with actual Fed policy. Going into the year, the market had priced in at least five cuts, which helped fuel a furious fourth quarter rally and investor optimism for 2024. One quarter in, however, those expectations have been turned on their head. Hotter than expected inflation and jobs reports in March have created a “higher for longer” narrative with the market expecting no more than two cuts during the second half of the year. Some economists have taken an even more bearish stance, suggesting there will not be any cuts. Overall, rates rose across the curve during the quarter as current U.S. debt levels sustained the long end of the curve while the short end was relatively unmoved.

Intuitively, many investors would expect such a big change in rate expectations to weigh heavily on markets, both equities and bonds. In that sense, equity performance was surprising during the first quarter, as the upward trend from 2023 continued. Predictably, bonds suffered as rates rose, but below investment grade sectors were profitable. To be fair, though, it should be noted that equities have endured a difficult start to this month, down 4.6% through April 22 as the higher for longer narrative has gained momentum.¹

Going forward, what should we watch for from asset classes as we venture into a market environment that looks much different than what we were expecting only three months ago?

Read > Mind the Gap

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

02.02.2026

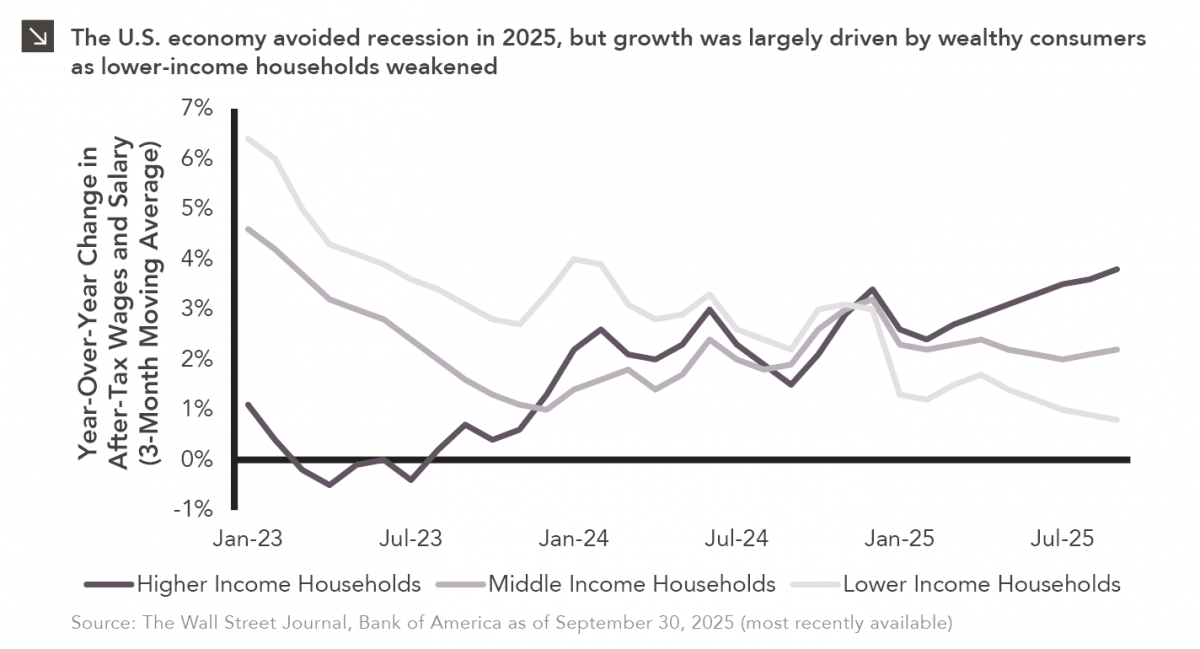

Macroeconomic forecasting is challenging in the best of times and proved downright impossible in 2025, which saw high levels of…

01.22.2026

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest…

01.07.2026

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the…

01.14.2026

Contrary to widespread belief, fixed income aggregate strategies offer a continuum of active risk and return profiles. While aggregate strategies…

01.12.2026

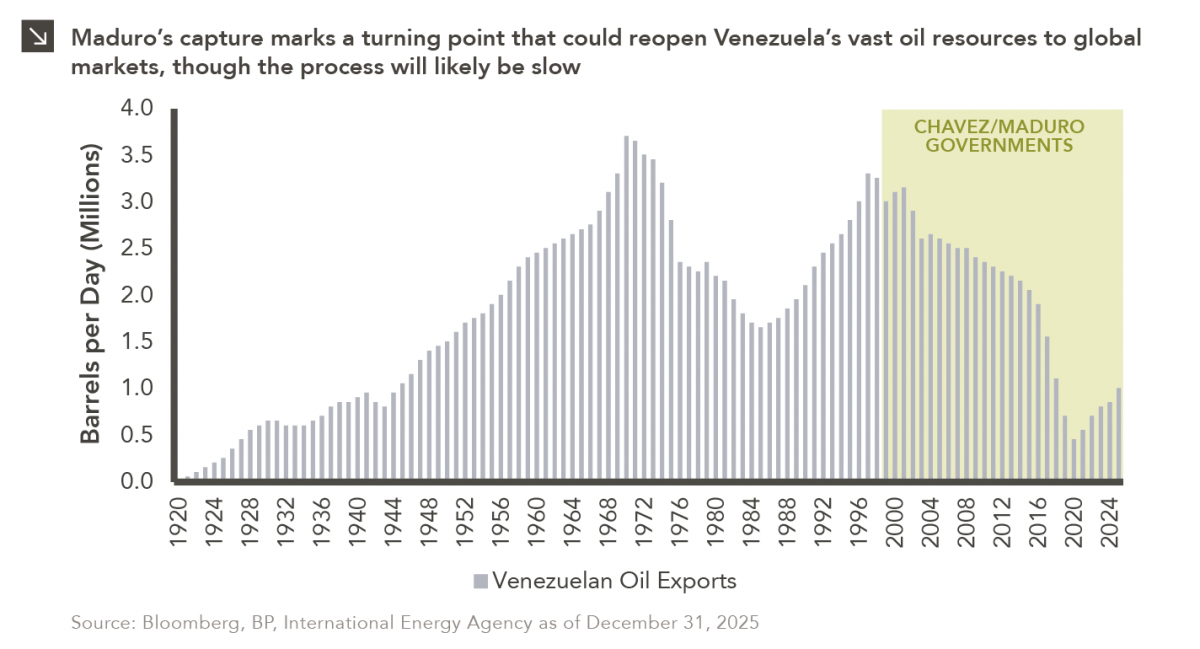

The capture of Venezuelan president Nicolás Maduro is a watershed moment for a country whose natural resource economy has been…

01.05.2026

The development of artificial intelligence is advancing along two largely distinct paths. The first centers on generative AI powered by…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >