01.12.2026

I Drink Your Milkshake

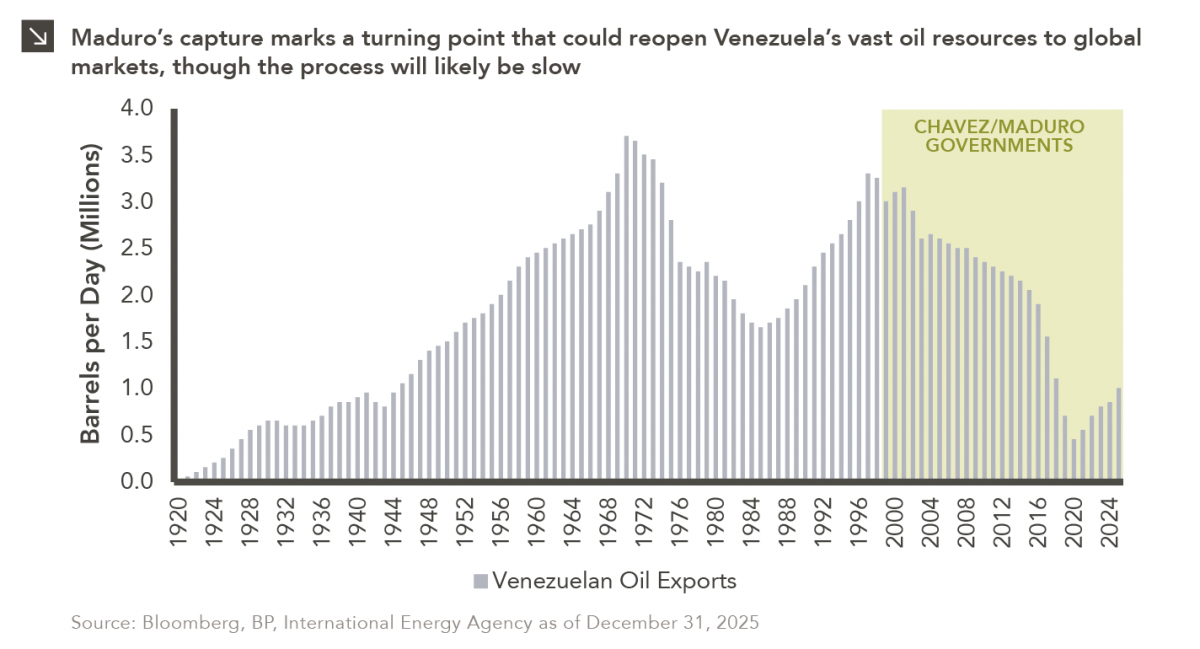

The capture of Venezuelan president Nicolás Maduro is a watershed moment for a country whose natural resource economy has been…

By now, you have all read the headlines and watched various news commentators detail the perils of the latest pneumonia outbreak, 2019 Novel Coronavirus (“nCov”), impacting China, nearby countries, and a few of their western trade partners. As of February 13th, confirmed cases in mainland China had reached over 60,000 patients, and as was broadcast on February 11th, the death total has surpassed 1,000. Even though these health figures are alarming, we have experienced similar outbreaks in the past and can take some comfort in knowing that eventual containment — and a vaccine — are in the works.

From a financial market’s standpoint, one common theme we are hearing from economists and portfolio managers is that, similar to the SARS outbreak of 2002–2003, the recent sharp, nCoV-driven market sell-off is temporary and the overall market impact will be minimal over the long-term. This chart of the week shows the short-term returns of the broader market — using the MSCI All Country World Index as the guidepost — during the SARS outbreak, as well as the current coronavirus. As shown in the chart, during the first three months of the SARS outbreak the MSCI ACWI posted a -2.9% return. However, six months after the initial SARS patient, the MSCI ACWI return was back in positive territory, up 2.8%.

While comparing SARS and nCoV makes sense from a regional and virus strain commonality, one must also consider the economic circumstances surrounding each outbreak. The supply chain connectivity between China and the broader world has advanced in leaps and bounds since 2003. The potential knock-on effects of an extended drop in Chinese factory productivity could slow, for instance, the technology supply chains for Apple, LG, Google, and more. Hence, economists are probably spot on that the market will rebound, but the details of the true impact on global growth are yet to be defined.

Print PDF > Much Ado About Corona?

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

01.12.2026

The capture of Venezuelan president Nicolás Maduro is a watershed moment for a country whose natural resource economy has been…

01.07.2026

Please join Marquette’s research team for our 2026 Market Preview Webinar analyzing 2025 across the economy and various asset classes…

01.05.2026

The development of artificial intelligence is advancing along two largely distinct paths. The first centers on generative AI powered by…

12.29.2025

While the holiday season was once marked by bustling bars, readers may notice that nightlife isn’t what it used to…

12.22.2025

Private equity is known for being an illiquid asset class, with investments typically locked up for several years and limited…

12.15.2025

While technology-oriented firms have made their presence known in equity markets for several years, these companies have made waves in…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >