Thomas Neuhardt

Associate Research Analyst

Get to Know Thomas

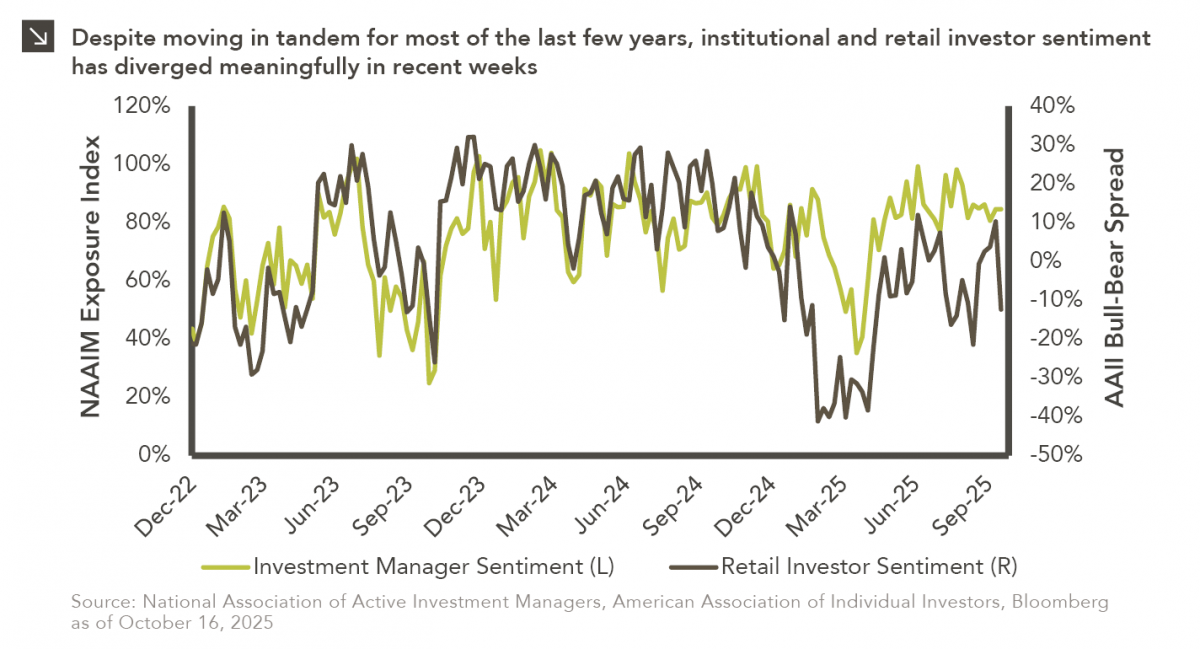

This week’s chart compares institutional and retail investor sentiment using two established indicators. Institutional sentiment is represented by the National Association of Active Investment Managers (NAAIM) Exposure Index, which measures the average U.S. equity market exposure reported by NAAIM member firms (i.e., organizations that actively manage client portfolios). Reported exposures for this index include -200% (leveraged short) to -100% (fully short), 0% (market neutral), +100% (fully invested), and +200% (leveraged long), capturing the breadth of positioning from extremely bearish to highly bullish. Retail sentiment is represented by the American Association of Individual Investors (AAII) Sentiment Survey, which reflects the bullish-minus-bearish spread regarding the six-month outlook for stocks across individual AAII members (i.e., retail investors). When analyzed together, these indicators offer perspective on how both institutional and individual investors view the near-term prospects of equity markets.

Readers will note that these two indices have moved in tandem throughout most of the last several years but have diverged significantly in recent weeks as retail investor sentiment has plunged. It is not entirely clear what’s driving this latest divergence, but several factors likely play a role. Specifically, renewed U.S.–China trade tensions, the ongoing federal government shutdown, and interest rate uncertainty have likely weighed more heavily on retail investors, who tend to be more influenced by headline noise. Institutional money managers, on the other hand, appear to be maintaining confidence in healthy corporate fundamentals and the broader economic backdrop. Regardless of its exact cause, this divergence underscores the notion that sentiment data should be viewed as context-dependent rather than as a market timing signal.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.22.2026

The usual midyear version of these letters has touched on year-to-date performance as well as the most influential macroeconomic and…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >