David Hernandez, CFA

Director of Traditional Manager Search

Through the first half of the year, most U.S. and non-U.S. equity indices have produced double-digit returns. For example, the S&P 500 and MSCI ACWI ex U.S. indices are up 18.5% and 13.6%, respectively. On the surface, these large returns appear to indicate a healthy equity market. However, when we dig deeper, we find that multiple expansion — rather than fundamentals — has been the key driver of year-to-date returns. In fact, earnings revisions have been negative across the globe as analysts have downgraded their 2019 EPS estimates.

Why have equity returns been so strong during a tepid earnings environment? First, we think markets were likely oversold in 2018, leading to a bounceback this year. Second, central banks throughout the world have become more accommodative, including possible rate cuts in the U.S. and tax cuts in China. This shift in monetary policy has boosted equity investor optimism. Looking to the rest of the year, we have a cautious view on equity returns given the poor earnings momentum. Additionally, macro events like the Brexit and U.S.-China trade relations serve as potential potholes in the second half. Collectively, these risks suggest more modest equity returns in the second half of 2019.

Print PDF > What to Expect from Global Equities?

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

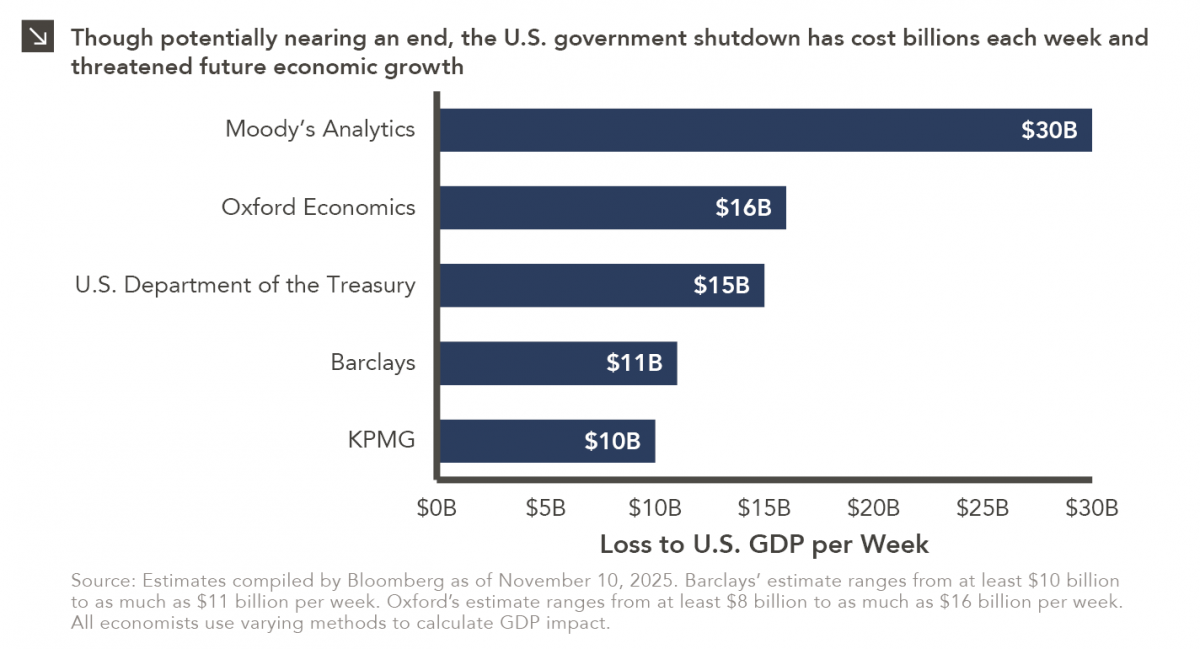

11.10.2025

Over the weekend, the Senate overcame a key procedural obstacle in its attempt to end the record-breaking government shutdown, as…

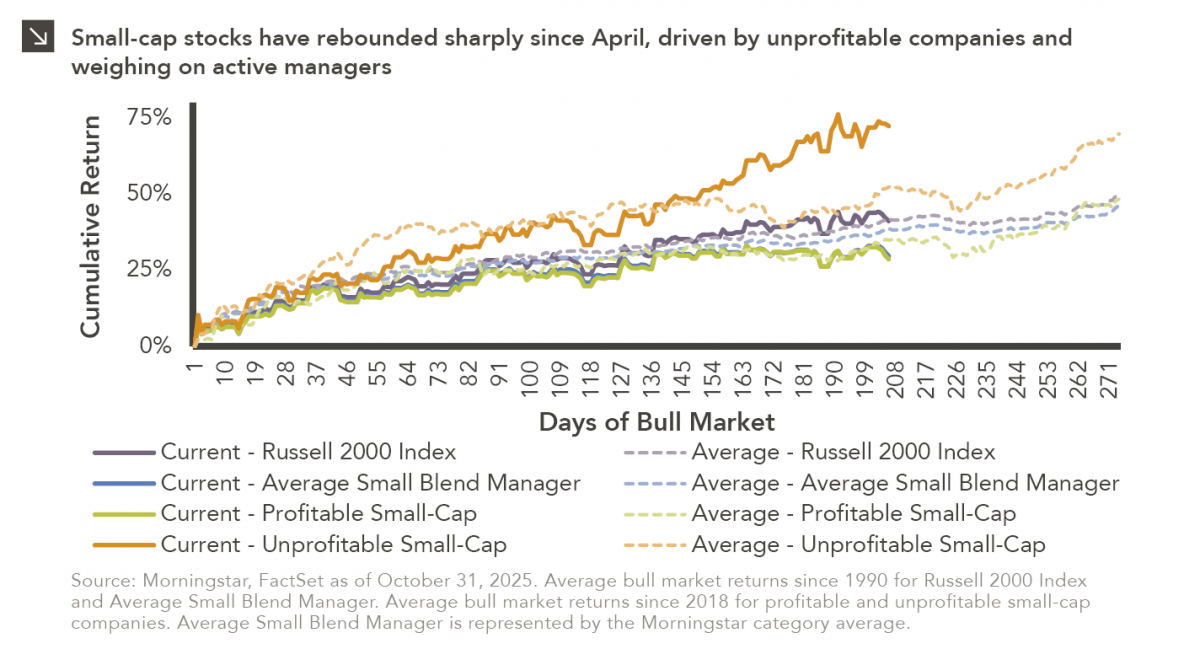

11.03.2025

Small-cap equities are in a prolonged period of underperformance relative to large-cap stocks, but this trend has shown early signs…

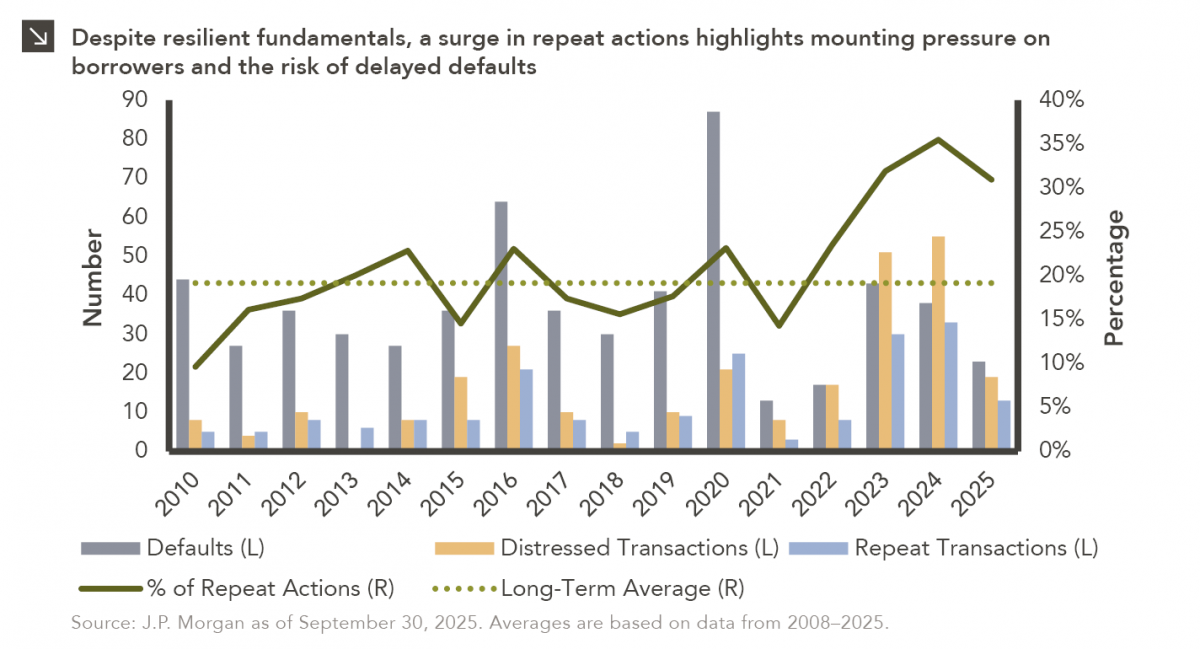

10.27.2025

To paraphrase a quote from former President George W. Bush: “Fool me once, shame on… shame on you. Fool me…

10.22.2025

This video is a recording of a live webinar held October 22 by Marquette’s research team analyzing the third quarter…

10.22.2025

I spent the past weekend at my alma mater to watch them play their biggest rival. Football weekends there are…

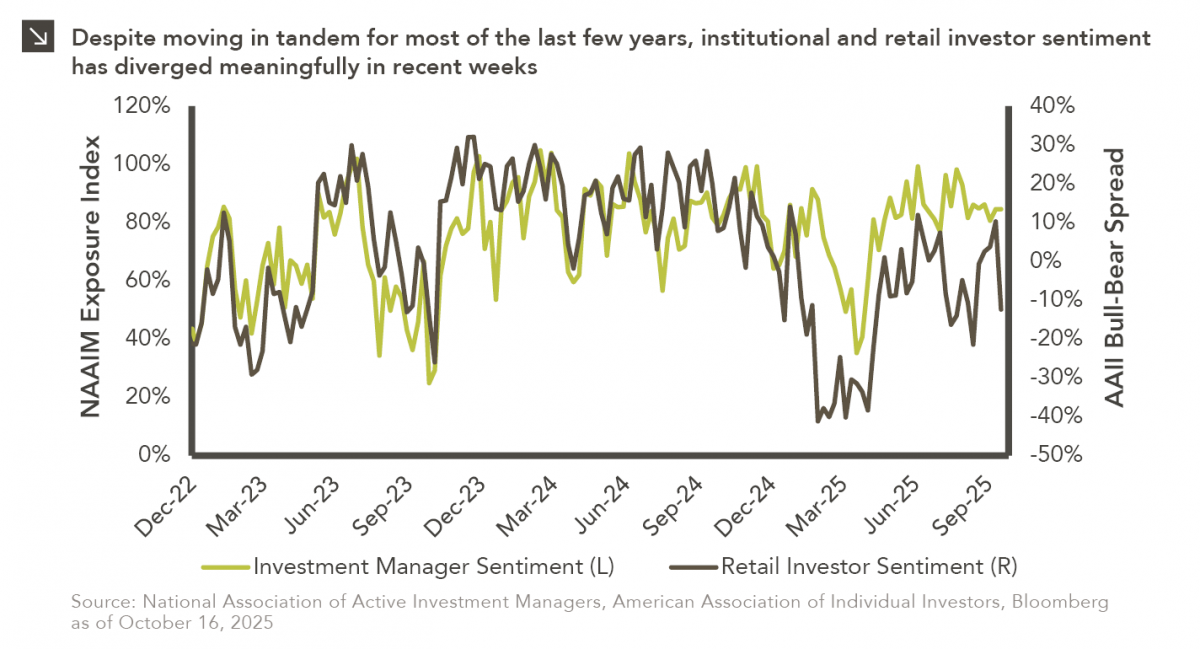

10.20.2025

This week’s chart compares institutional and retail investor sentiment using two established indicators. Institutional sentiment is represented by the National…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >