Pooja Vyas

Research Analyst

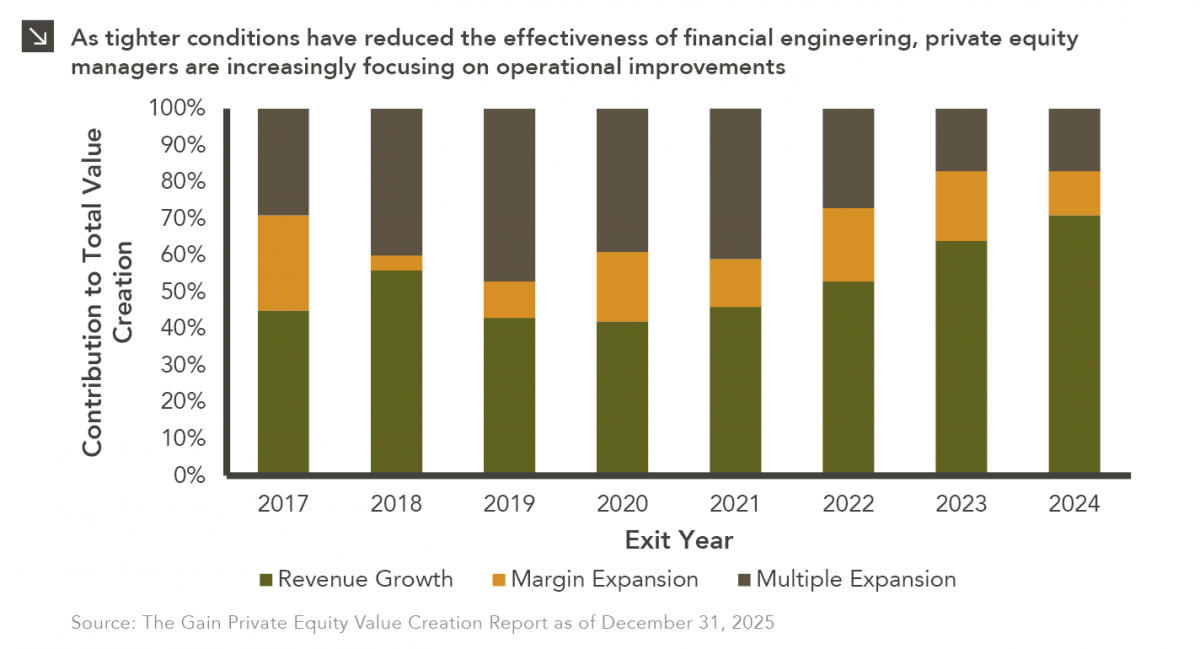

In the period between 2009 and 2022, private equity managers thrived amid an environment of low interest rates and rising asset prices, which led to financial engineering serving as a primary driver of portfolio value. In recent years, however, higher interest rates, elevated valuations, and tighter exit conditions have reduced the effectiveness of this value creation method. As a result, financial engineering has shifted from a core value driver to a supporting tool, prompting firms to increasingly focus on operational improvements within portfolio companies. Indeed, top-line growth and margin expansion are the key areas of value creation today, with revenue growth accounting for roughly 54% of value creation for deals that saw exits between 2017 and 2024. This dynamic can be attributed to the role of revenue growth as a sustainable and longer-term source of value creation, as it supports revenue base expansion, enables EBITDA growth, and facilitates more favorable valuation outcomes.

To drive both growth and profitability, private equity firms deploy a range of operational initiatives, including cost transformation, pricing optimization, technology integration, and supply chain improvements. While studies show that operations and pricing are the most effective levers in value creation playbooks, it is important to remember that execution is just as important as planning. To that point, a recent study found that more than half of executives cited poor implementation as a primary and controllable cause of underperformance of their businesses. Ultimately, as operational improvements become more crucial to value creation, private equity firms that can execute with discipline, particularly across revenue growth and margin expansion, will differentiate themselves when it comes to delivering returns and building more resilient and scalable businesses.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

07.24.2026

This video is a recording of a live webinar held July 23 by Marquette’s research team analyzing the first half…

07.20.2026

Our most recent Chart of the Week publication discussed how the AI investment opportunity has expanded beyond…

07.13.2026

One of the enduring lessons of the California Gold Rush is that the greatest fortunes were often made not by…

07.06.2026

Since traditional exit routes have remained constrained in recent years due to higher interest rates, valuation gaps, and a subdued…

06.29.2026

This week’s chart highlights the varying return profiles across key infrastructure sectors by illustrating the split between income and capital…

06.22.2026

When Benchmark, one of Silicon Valley’s most renowned early-stage venture capital firms, closed $2 billion across two new funds this…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >