This morning, the Federal Reserve cut short term interest rates by 50bp to defend against the global economic effects of the coronavirus outbreak. The previous three cuts occurred throughout 2019 as a result of combatting the global slowdown due to the U.S.-China tariff negotiations. This latest cut was a surprise for the markets as going into the day Fed Funds futures showed a strong probability of one rate cut in each of the Fed’s March, June, and September Federal Open Market Committee meetings this year.

This week’s chart shows that the rate cut brings the Fed Funds target range upper limit now to 1.25% (not shown is the lower limit now at 1.00%), juxtaposed against the VIX, which is a measure of the S&P 500’s expected volatility that spiked over the last few days.

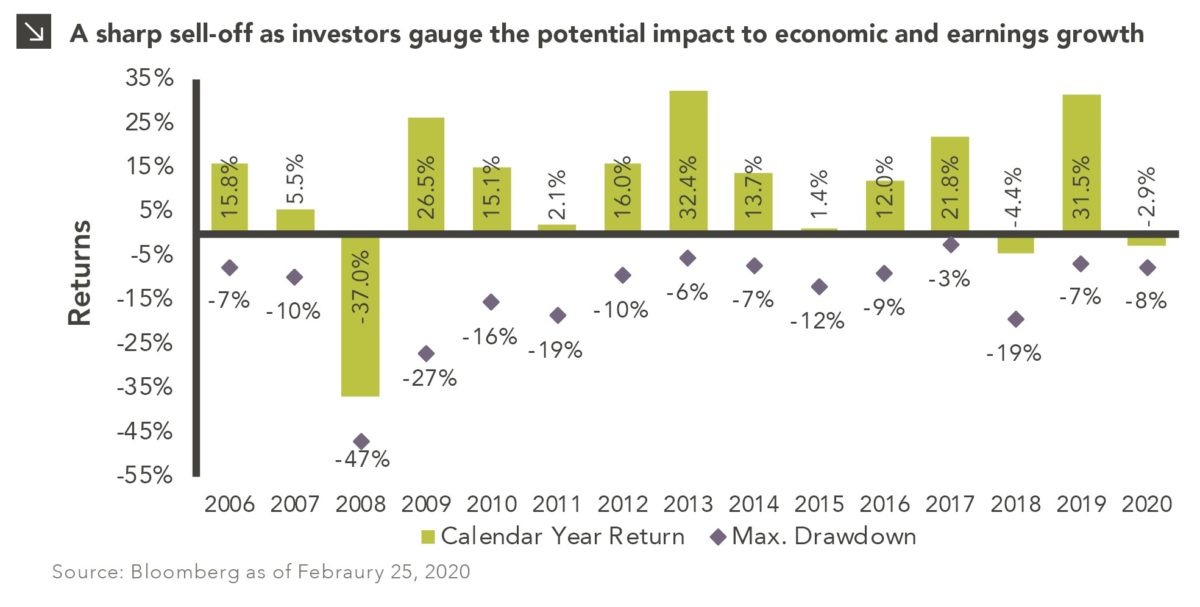

It is unclear what the ramifications of this central bank action might be on the markets in the short-term, as the Fed’s signal of apparent concern may cause a fear-induced sell-off in the markets. This is what we are seeing so far, as the S&P 500 is off 2.8% for the day while the 10-year U.S. Treasury fell from yesterday’s close of 1.10% to 1.02% at today’s close. However, the longer-term effects should be stimulative as lower rates will make it easier for businesses and consumers to borrow and refinance their debts as well as ease their interest expense burdens.

The hope is that this cut will reduce short-term economic headwinds to the global economy and combat the onset of a recession. While it is impossible to predict when the outbreak will be contained, the number of new cases in source country China is declining and the coronavirus fatality rate remains low at 3%.

The global fatality rate is especially low for individuals not of elderly age. The latest data provided by global insurer Natixis and the Chinese Center for Disease Control & Prevention show that the fatality rate for individuals under 60 years of age is less than 1.3%, with those under age 50 seeing a fatality rate less than 0.4%.

As such, the U.S. Treasury yield curve is still upward sloping in both the 2-year vs. the 10-year and the 2-year vs. the 30-year, showing no signal of an impending recession. In contrast, both these measures were downward sloping going into the tech crisis in 2000 and housing crisis in 2008.

However, we may expect persistent short-term volatility as China recently released its Purchasing Managers’ Index (PMI). A PMI below 50 signals a contraction, and China’s latest PMI is at 30, the lowest it has ever been. To preemptively combat this potential economic slowdown, the Fed’s 50bp rate cut should provide a boost to the U.S. and global economy and we would expect central banks around the world to likely follow suit.

Print PDF > Fed Cuts Rates 50bp to Fight Coronavirus Effects

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.