Julia Sheehan

Research Analyst

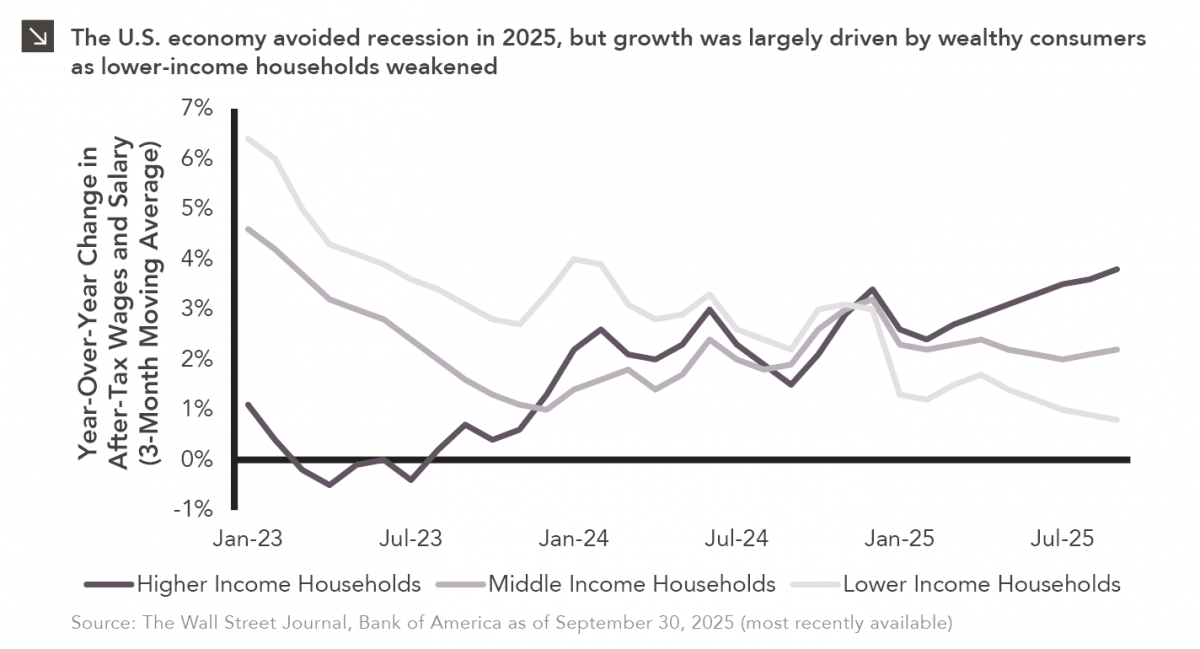

Macroeconomic forecasting is challenging in the best of times and proved downright impossible in 2025, which saw high levels of geopolitical instability and policy uncertainty. Many economists were cautiously optimistic about the state of the global economy at the start of last year, only to revise growth forecasts sharply downward after President Trump’s tariff announcements in April. By summer, markets and economists alike were still largely convinced that a recession was imminent, but this anticipated downturn did not materialize. On the contrary, high-level GDP and consumer spending data for 2025 suggest stable (albeit slowing) economic growth. Despite steady headline figures, however, concerns remain surrounding potential softening of the domestic labor market and slowing real-wage growth. As illustrated by the chart above, these effects are distributed unevenly across income brackets, with wages rising by 3.8% for the highest-earning households over the last year, compared to only 0.8% for lower-earning households. Consumption for lower-income households has also declined in recent time, with a Moody’s survey estimating that the top 10% wealthiest U.S. households now account for roughly half of all consumer spending. Equity market performance has exacerbated this inequality, as wealthier individuals tend to have a larger percentage of their net worth invested in financial assets.

Economic bifurcation, often referred to as a “K-shaped economy,” explains why strong GDP growth can occur in tandem with deteriorating consumer confidence. This dynamic has also challenged policymakers, as institutions like the Federal Reserve have been tasked in recent years with both cooling inflation and preventing further labor market deterioration. Moreover, as lower-income households struggle to finance essential purchases, it is possible that future GDP growth will be contingent on wealthier households spending at current or higher rates. It follows that an event that leads to a pullback in spending (e.g., an equity market downturn) could be detrimental to overall growth. While predicting the trajectory of the economy is certainly a challenge, understanding these dynamics offers some insight into the indicators to monitor in 2026.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

03.30.2026

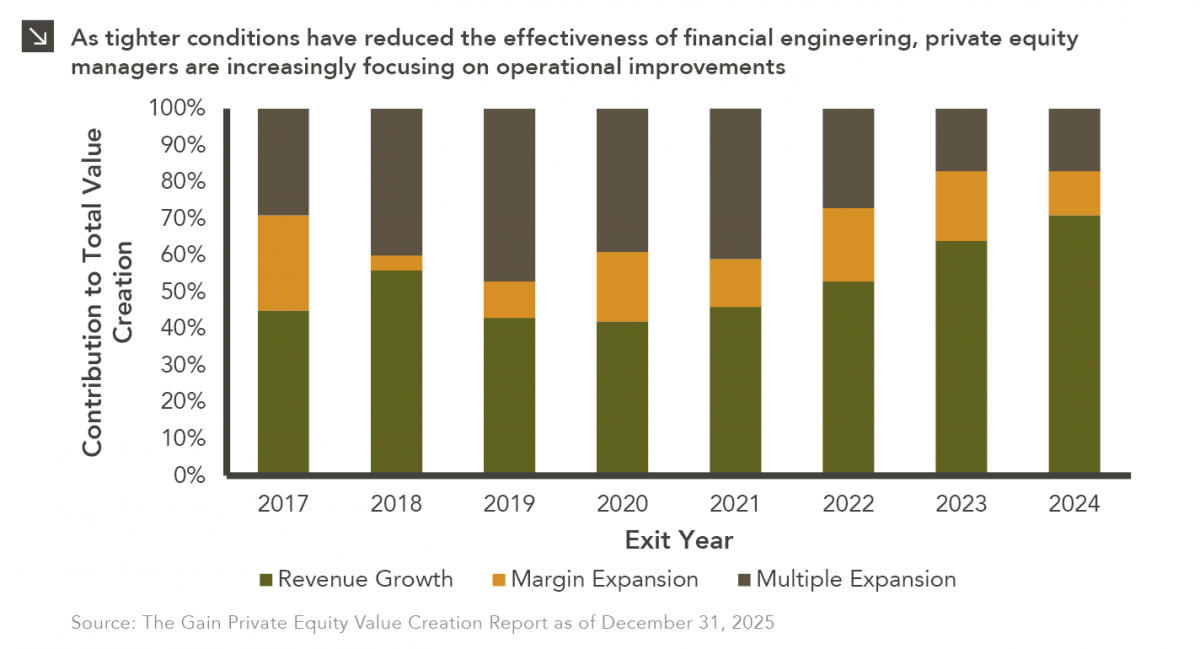

In the period between 2009 and 2022, private equity managers thrived amid an environment of low interest rates and rising…

03.23.2026

Global energy costs have risen sharply this month due to a convergence of geopolitical shocks, as critical infrastructure and transport…

03.16.2026

This week’s chart illustrates a clear structural shift in the fundraising dynamics of North American closed-end real estate funds over…

03.09.2026

Warren Buffett once implored investors to “be greedy when others are fearful,” and this sage advice is certainly applicable to…

03.02.2026

Recent market dynamics in the software sector reflect a sharp shift in investor sentiment driven primarily by concerns that advances…

02.23.2026

Most have traditionally viewed a successful exit for a venture-backed start-up as either an IPO or an acquisition by a…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >