01.26.2026

Pining for Evergreens

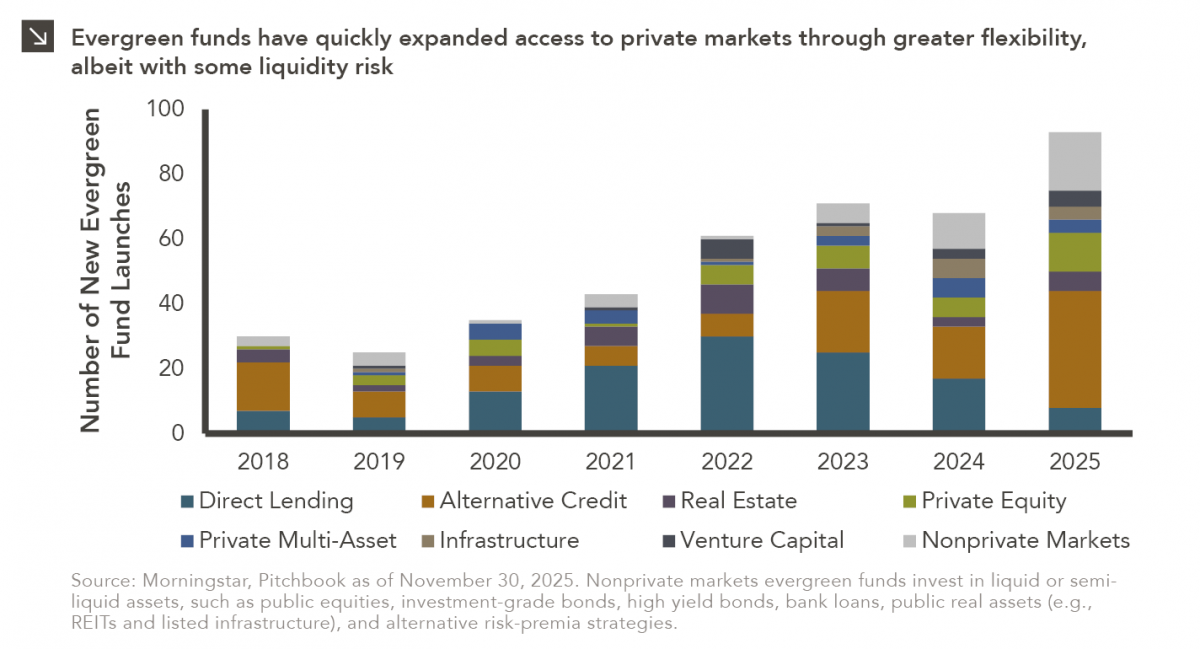

In recent years, access to traditionally illiquid private markets has expanded through the rapid growth of evergreen funds, which provide…

Our chart this week examines the historical1 total returns of the NCREIF Property Index (“NPI”) during times of rising interest rates. As illustrated in the chart, real estate has historically showed little correlation with interest rates indicating changes in interest rates do not immediately translate to asset prices. In fact, the average annual total return during periods of rising rates is 12.3%; typically rising rates are accompanied by stronger economic growth and/or inflation, both which inevitably draw investors to real assets. It is important to keep in mind, however, that private real estate is valued less frequently than its publicly traded (daily valued) counterparts. This is important because changes in private real estate prices will typically lag changes in interest rates as a result of less frequent valuations.

With interest rates expected to rise further, the spread between the 10-Year Treasury and real estate cap rates will continue to shrink, but strong fundamentals – such as rent growth and economic growth – are much more important than movements in the 10-year Treasury. There is no magic number for the 10-year that would trigger a re-pricing of real estate, but some property types are more susceptible to higher rates such as those with longer-term bond-like leases. Going forward, we believe that a mix of strong fundamentals mixed with stable rising rates will translate into moderate, income-driven returns to core real estate in the mid to high single-digit range.

1Since inception

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

01.26.2026

In recent years, access to traditionally illiquid private markets has expanded through the rapid growth of evergreen funds, which provide…

01.22.2026

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest…

01.20.2026

Last week, Alphabet joined NVIDIA, Microsoft and Apple as the only companies to ever reach a market capitalization of $4…

01.07.2026

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the…

01.12.2026

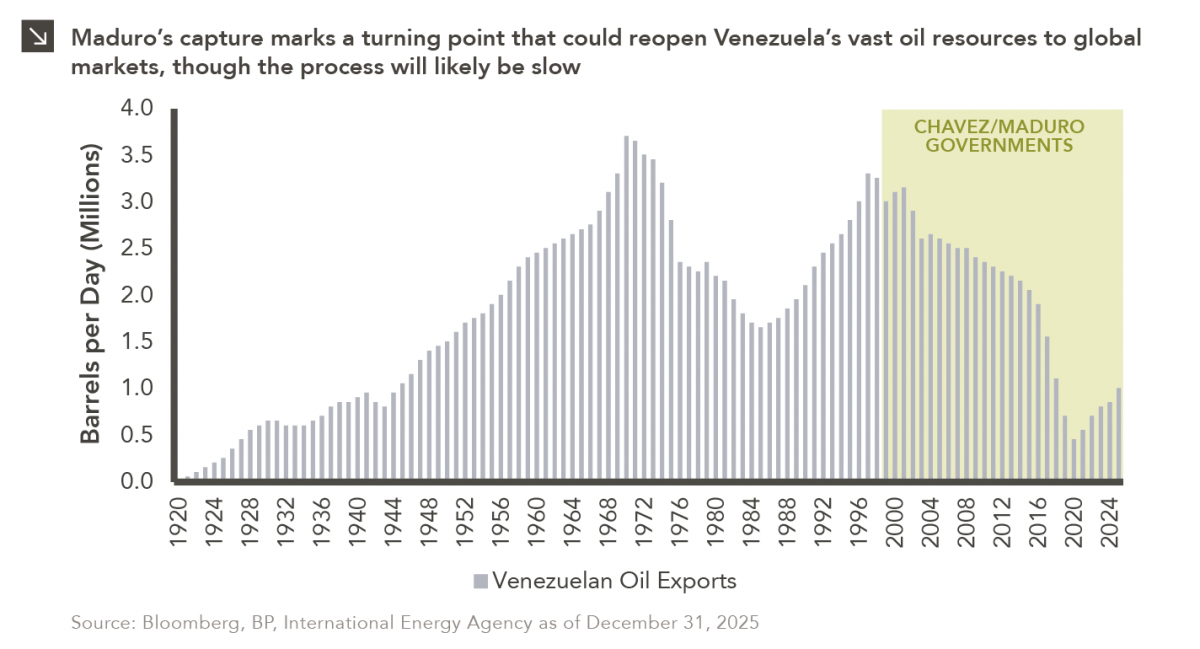

The capture of Venezuelan president Nicolás Maduro is a watershed moment for a country whose natural resource economy has been…

01.05.2026

The development of artificial intelligence is advancing along two largely distinct paths. The first centers on generative AI powered by…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >