06.08.2026

How to Launder Your Volatility

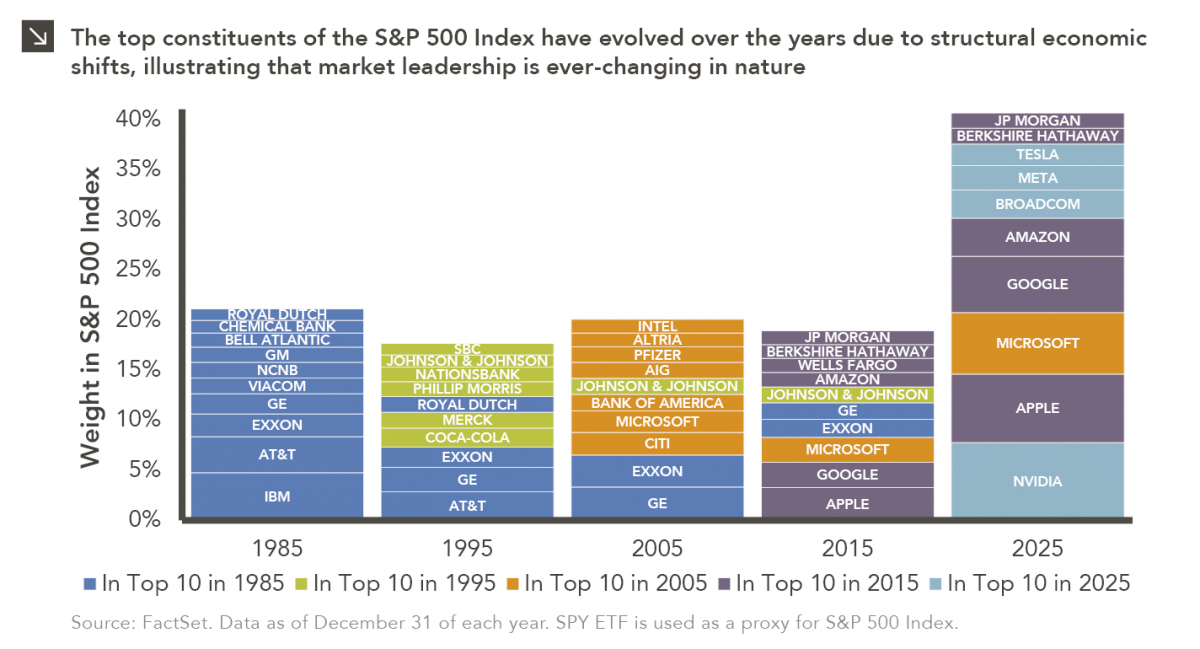

Hi, James Torgerson here! Volatility can be an unsightly blemish on portfolios and lead to inferior risk-adjusted returns. Private credit…

Uncertainty lingers in the office sector against a backdrop of extended office closures across the U.S. Average occupancy rates have dropped over the past year and net absorption further declined in the first quarter of 2021. The national average vacancy rate for the office sector rose to 16% in Q1 2021, up 100 basis points quarter-over-quarter and 370 basis points year-over-year.¹ The ongoing rate of deterioration in office fundamentals has been somewhat surprising given the rebound in the labor market as the economy has reopened. Although office rents have been sticky so far, questions remain about the longer-term demand for office space, with some property owners offering leasing concessions in primary markets hit hardest by vacancies.

The second half of the year should provide some clarity with the COVID-19 vaccine rollout in full swing and more and more employees expected to return to work. The long-term extent of remote working on office demand is the biggest outstanding question. Average days in the office has fallen from 4.6 days a week to 3.6 days a week.² Employers are re-evaluating office space needs, looking to balance a flexible work environment with the benefits of workplace collaboration and productivity. Rising new supply combined with more than a year of minimal leasing activity will also continue to put downward pressure on office rents and occupancies in the near term. From here, we may see office demand stabilize, setting the stage for an uptick in leasing activity, or we may realize we are facing a new normal. We will continue to look for and recommend to our clients real estate managers that we believe are best positioned to navigate this evolving dynamic.

Print PDF > Welcome Back…to the Grind

¹ Cushman & Wakefield, KPMG, The 2021 KPMG CEO Outlook Pulse Survey, Clarion Partners Investment Research, June 2021.

² TA Realty, Defining Themes of 2021

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

06.08.2026

Hi, James Torgerson here! Volatility can be an unsightly blemish on portfolios and lead to inferior risk-adjusted returns. Private credit…

06.01.2026

The MSCI Emerging Markets Index has undergone a significant structural transformation in recent years. For much of the past decade,…

05.26.2026

The classic novel A Tale of Two Cities by Charles Dickens begins with the line “It was the best of…

05.18.2026

Over the last few years, equity markets have been defined by a group of stocks often referred to as the…

05.11.2026

In addition to the humanitarian toll of the conflict in Iran, the world is currently confronting the impact that trade…

05.04.2026

Rooted in medieval Persian Sufi thought, the adage “this too shall pass” speaks to the fleeting and impermanent nature of…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >