Julia Sheehan

Research Analyst

The first 100 days of a presidential administration are typically scrutinized closely as the public develops a sense of the new government’s agenda and top priorities. The second Trump administration is certainly no exception, and the recent flurry of executive orders and tariff proposals has caused significant uncertainty for policymakers and financial markets alike. Trump’s handling of the Russia-Ukraine War has had an especially notable impact. In March, the Trump administration suspended aid to Ukraine after a tense meeting with Ukrainian President Volodymyr Zelenskyy. That decision elicited a strong response from European leaders, who now have a newfound sense of urgency when it comes to rebuilding the continent’s defense capabilities. In recent weeks, the European Commission, the executive branch of the European Union, announced its “ReArm Europe Plan,” complete with a white paper entitled “European Defense Readiness 2030.” These documents emphasize the need for Europe to bolster defense spending and outline an investment plan to do so.

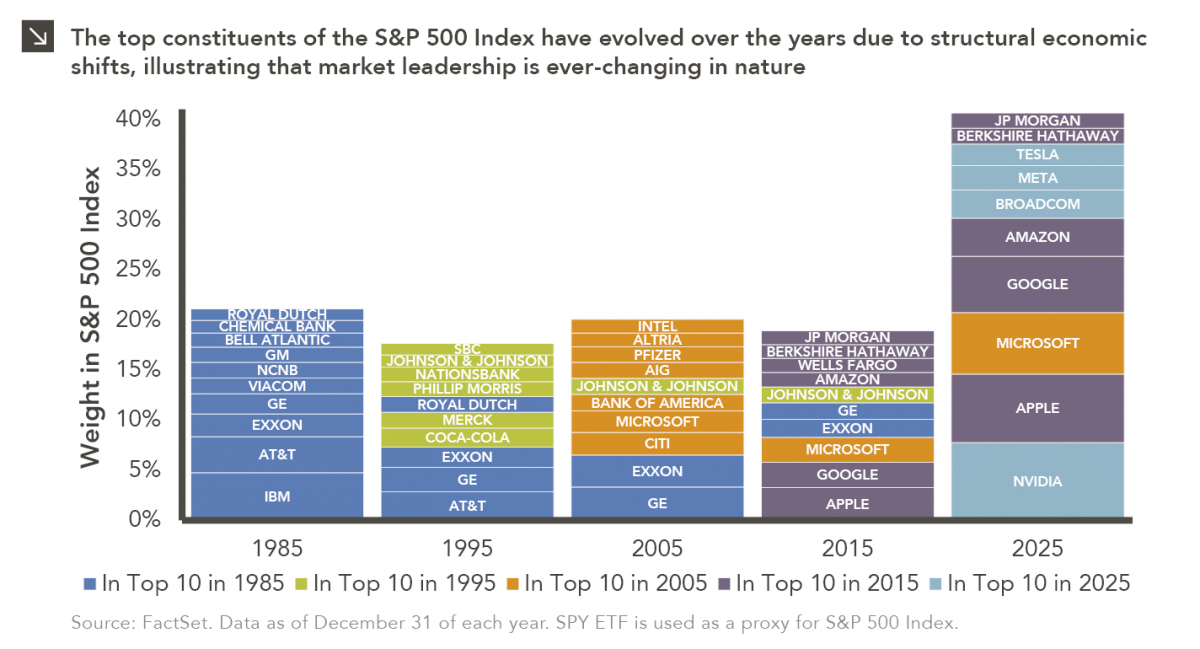

Global markets took note of this dynamic well before the unveiling of the ReArm Europe Plan, with European defense stocks surging as the continent’s relationship with the Trump administration has deteriorated. To that point, the STOXX Europe Total Market Aerospace & Defense index returned roughly 28.9% in the first quarter, with noteworthy contributors including Rheinmetall, a German arms manufacturer, the French military aircraft manufacturer Dassault Aviation, and Leonardo DRS, an Italian aerospace and defense specialist. This is in striking contrast to the market leaders of 2024, including U.S.-based tech giants such as NVIDIA and Microsoft. The Magnificent Seven basket of stocks have returned roughly -16.0% so far in 2025.

While investors are understandably enthusiastic about the prospects of defense spending jumpstarting the European economy, making these defense goals a reality will not be an easy task, especially for European countries such as France that are heavily indebted with a highly taxed citizenry. One thing is for certain: The market’s response to recent defense initiatives in Europe illustrates the importance of maintaining a diversified investment portfolio, as it is difficult to predict the catalysts that will drive performance reversals like the one detailed above.

Print PDF

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

06.01.2026

The MSCI Emerging Markets Index has undergone a significant structural transformation in recent years. For much of the past decade,…

05.26.2026

The classic novel A Tale of Two Cities by Charles Dickens begins with the line “It was the best of…

05.18.2026

Over the last few years, equity markets have been defined by a group of stocks often referred to as the…

05.11.2026

In addition to the humanitarian toll of the conflict in Iran, the world is currently confronting the impact that trade…

05.07.2026

The leadership structure of the Federal Reserve is intentionally designed to promote continuity, independence, and institutional stability across political cycles….

05.04.2026

Rooted in medieval Persian Sufi thought, the adage “this too shall pass” speaks to the fleeting and impermanent nature of…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >