01.26.2026

Pining for Evergreens

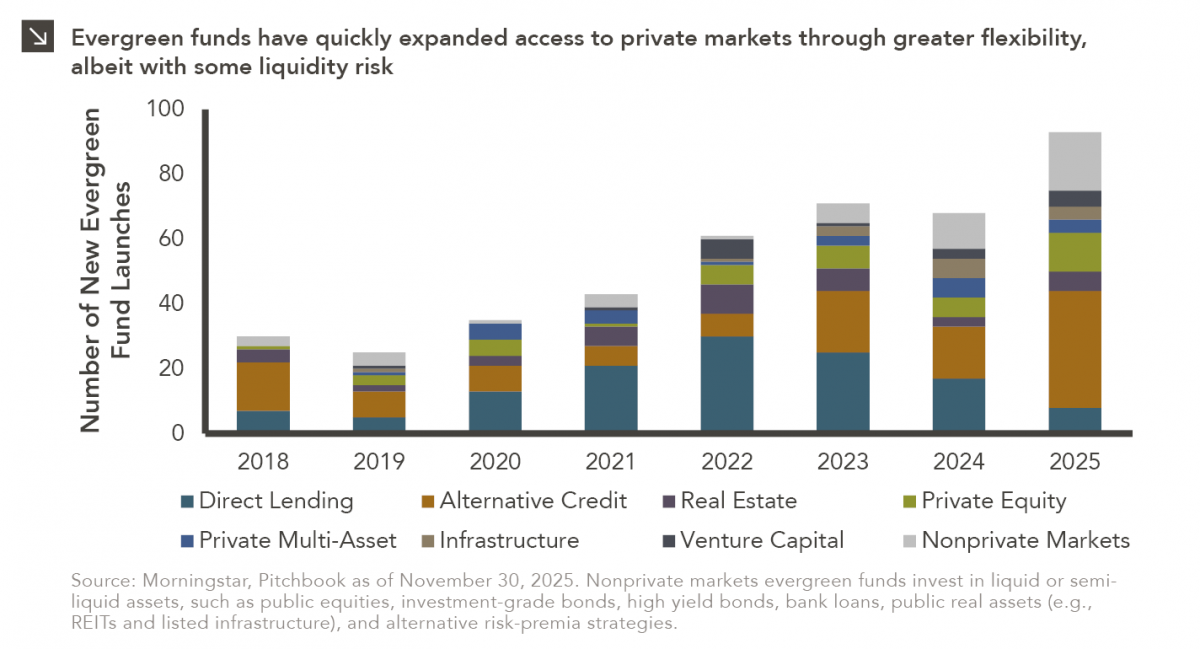

In recent years, access to traditionally illiquid private markets has expanded through the rapid growth of evergreen funds, which provide…

Real estate debt investors, relative to equity investors, are generally more insulated against downside risk with underlying properties secured as collateral. Mechanically, a debt investor is effectively lending money to a borrower who may require bridge or rescue financing to close on prospective property acquisitions or development deals. Lending to borrowers at higher interest rates allows for higher returns, as well as consistent cash yields.

Commercial mortgage-backed securities (CMBS)¹ — the public form of real estate debt — have seen market yields rise materially amid higher interest rates. Debt is en vogue again as yields are back to levels that can contribute meaningfully to portfolio returns. 2022 was a year of re-pricing due to the impact of higher interest rates. Public real estate markets quickly embedded a recession risk-premium into pricing while private market valuations trailed. If the economy enters a recession this year, debt is likely to perform relatively well based on conservative underwriting and performance that is not directly tied to a property’s net operating income growth. CMBS excess spreads have also widened out relative to corporate bonds to account for real estate-specific downside scenarios. As shown in the chart, CMBS yields are currently comparable to the yield of corporate bonds rated at least two full ratings lower. Though market risks remain, higher rates and wider spreads have created a potentially attractive relative value landscape for CMBS opportunities.

Print PDF > Debt is the New Equity

¹Commercial mortgage-backed securities (CMBS) are fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

01.26.2026

In recent years, access to traditionally illiquid private markets has expanded through the rapid growth of evergreen funds, which provide…

01.22.2026

Anyone who has gone snowmobiling knows it can be simultaneously exhilarating and terrifying. Throttling across snow and through a forest…

01.20.2026

Last week, Alphabet joined NVIDIA, Microsoft and Apple as the only companies to ever reach a market capitalization of $4…

01.07.2026

This video is a recording of a live webinar held January 15 by Marquette’s research team analyzing 2025 across the…

01.14.2026

Contrary to widespread belief, fixed income aggregate strategies offer a continuum of active risk and return profiles. While aggregate strategies…

01.12.2026

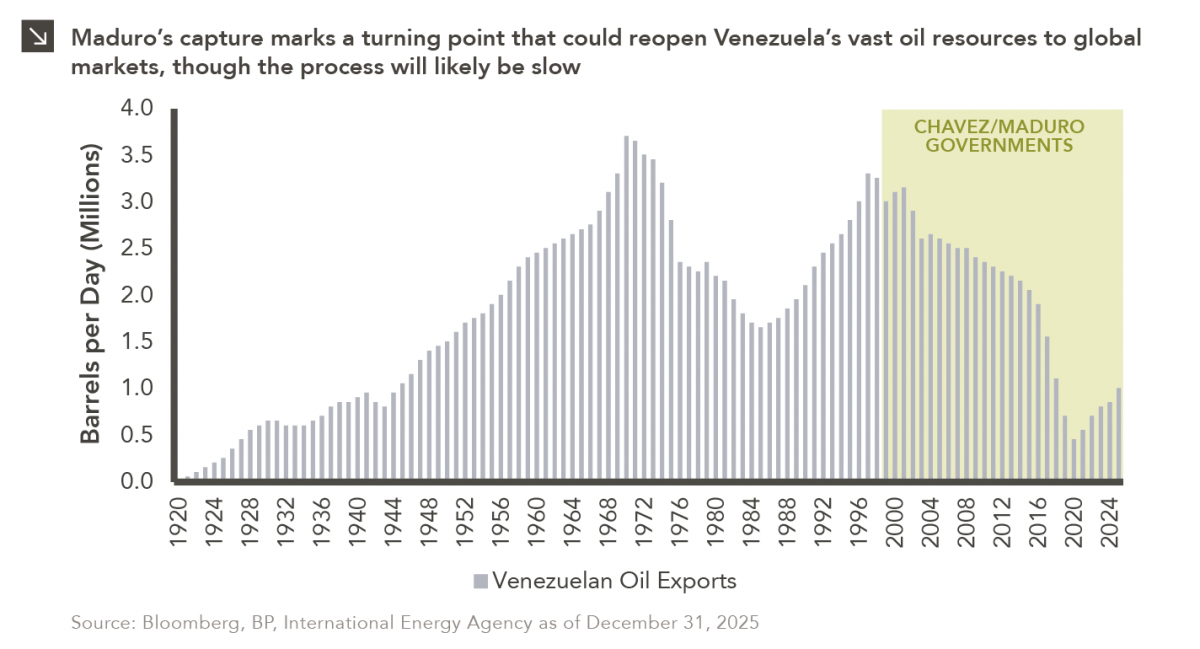

The capture of Venezuelan president Nicolás Maduro is a watershed moment for a country whose natural resource economy has been…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >