Jesus Jimenez

Principal

This week’s chart of the week examines the difference in private non-financial sector debt levels as a percentage of GDP for the United States and China. Private non-financial sector includes non-financial corporations (both private-owned and public-owned), households, and non-profit institutions serving households. Rising debt levels are a concern to any economy, as higher debt as a percentage of GDP is a potential drag on growth.

In the chart above, the most striking development is that China’s debt (as a percentage of GDP) is now higher than the U.S. There are a variety of reasons for this, including deleveraging in the U.S. in the wake of the Great Recession, as well as easy credit coupled with massive infrastructure spending in China. Collectively, these trends have driven the relative debt in China higher than the U.S., which is especially worrisome for future growth prospects in China, and by extension, investments in the country. It is not surprising that investor sentiment has cooled regarding China as of late, and investors will closely watch the growing debt level in the coming years.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

11.03.2025

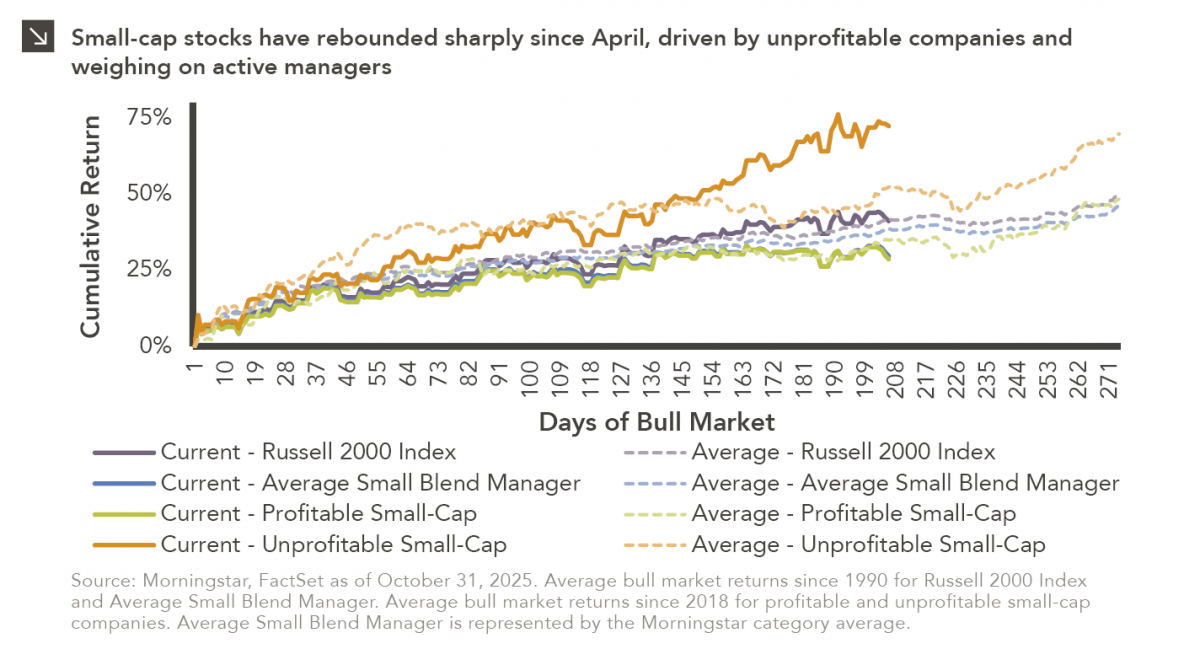

Small-cap equities are in a prolonged period of underperformance relative to large-cap stocks, but this trend has shown early signs…

10.27.2025

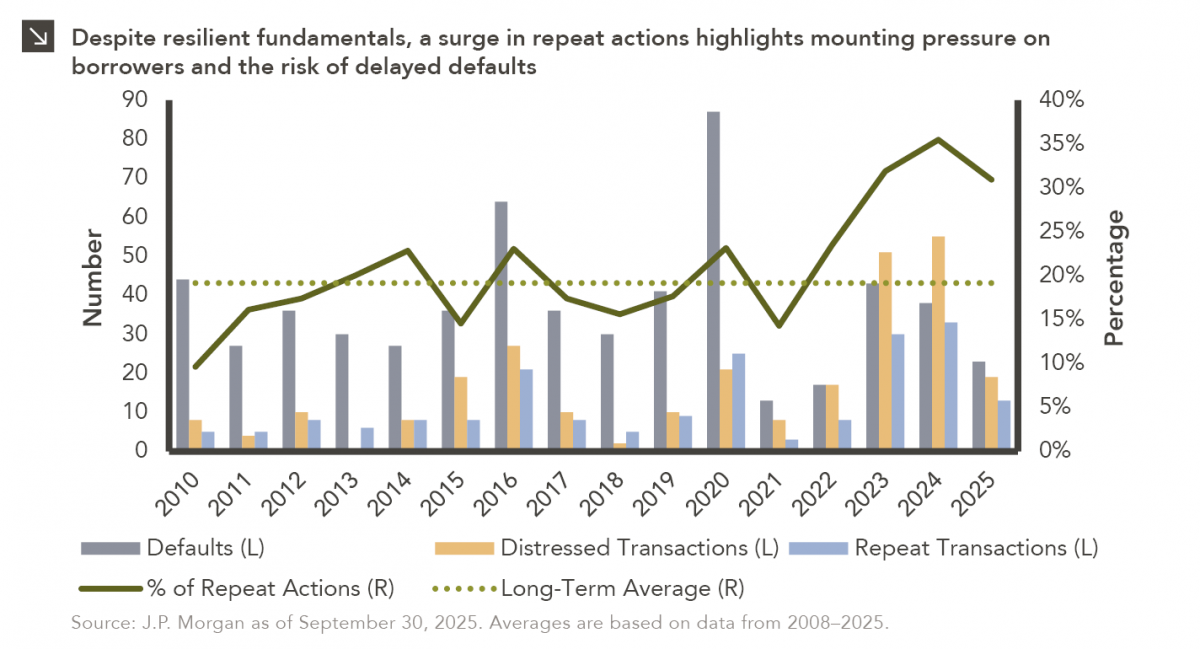

To paraphrase a quote from former President George W. Bush: “Fool me once, shame on… shame on you. Fool me…

10.22.2025

This video is a recording of a live webinar held October 22 by Marquette’s research team analyzing the third quarter…

10.22.2025

I spent the past weekend at my alma mater to watch them play their biggest rival. Football weekends there are…

10.20.2025

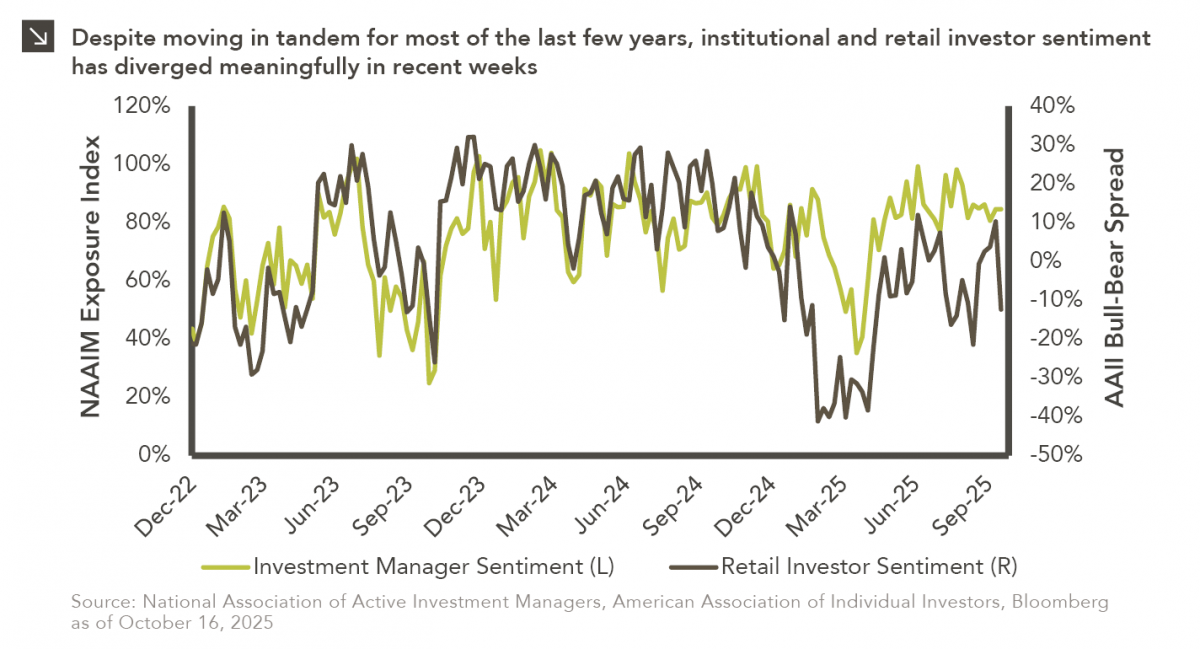

This week’s chart compares institutional and retail investor sentiment using two established indicators. Institutional sentiment is represented by the National…

10.13.2025

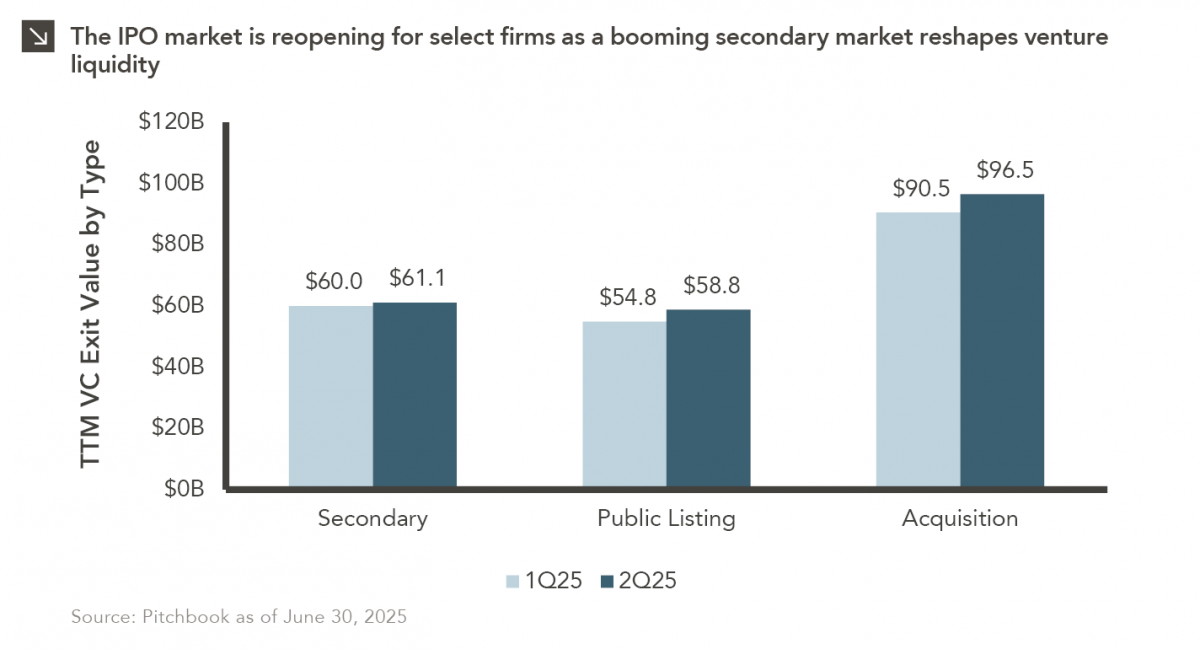

After a three-year drought, the IPO market is stirring again… but only for a select few. Just 18 companies have…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >