06.15.2026

Centers of Attention

The rapid buildout of artificial intelligence infrastructure is reshaping the U.S. investment landscape. According to recent Census Bureau data, spending…

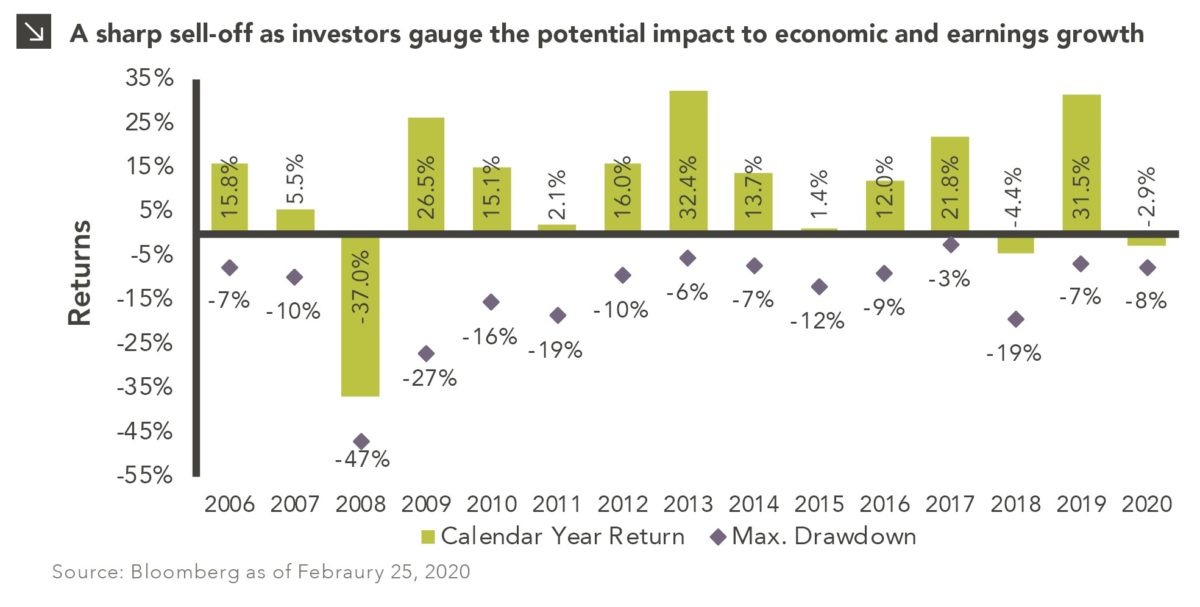

U.S. equities recently experienced a sharp three-day sell-off as the market digested the potential for short-term disruptions to economic growth and company earnings due to the Coronavirus (COVID-19). With new health figures coming out daily, it is easy to become alarmed. However, as our Chart of the Week from February 13th highlighted, prior health crises have been proven to be non-events longer-term for equity markets. Similar outbreaks in the past caused short-term sell-offs in equity markets but longer-term saw positive market performance.

This week’s chart shows calendar year returns for the S&P 500 along with the max drawdown that occurred in each respective year. As of February 25, 2020, the S&P 500 has recorded a year-to-date drawdown of 7.6%. The current pullback is undeniably sharp in nature, but it is important to maintain perspective during turbulent times. Over the past 15 years, the average annual max drawdown was 14%. Many years experienced drawdowns near this level, yet still yielded a positive return for the year. On average, equities see a 5% pullback four times per year, a 10% pullback once per year, and a 20% correction once every five years.

While no one knows the full impact that the current outbreak will have to supply chains, trade, or travel, we recommend taking a long-term view to investing. The market had been looking past this current health crisis until the last few days, so a repricing of risk was inevitable. As this is an evolving situation, there is risk that the economic impact could increase and add further pressure to equities. However, the current pullback remains in-line with historical trends.

Print PDF > Coronavirus Roils the Equity Markets

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

06.15.2026

The rapid buildout of artificial intelligence infrastructure is reshaping the U.S. investment landscape. According to recent Census Bureau data, spending…

06.08.2026

Hi, James Torgerson here! Volatility can be an unsightly blemish on portfolios and lead to inferior risk-adjusted returns. Private credit…

06.01.2026

The MSCI Emerging Markets Index has undergone a significant structural transformation in recent years. For much of the past decade,…

05.26.2026

The classic novel A Tale of Two Cities by Charles Dickens begins with the line “It was the best of…

05.18.2026

Over the last few years, equity markets have been defined by a group of stocks often referred to as the…

05.11.2026

In addition to the humanitarian toll of the conflict in Iran, the world is currently confronting the impact that trade…

Research alerts keep you updated on our latest research publications. Simply enter your contact information, choose the research alerts you would like to receive and click Subscribe. Alerts will be sent as research is published.

We respect your privacy. We will never share or sell your information.

If you have questions or need further information, please contact us directly and we will respond to your inquiry within 24 hours.

Contact Us >