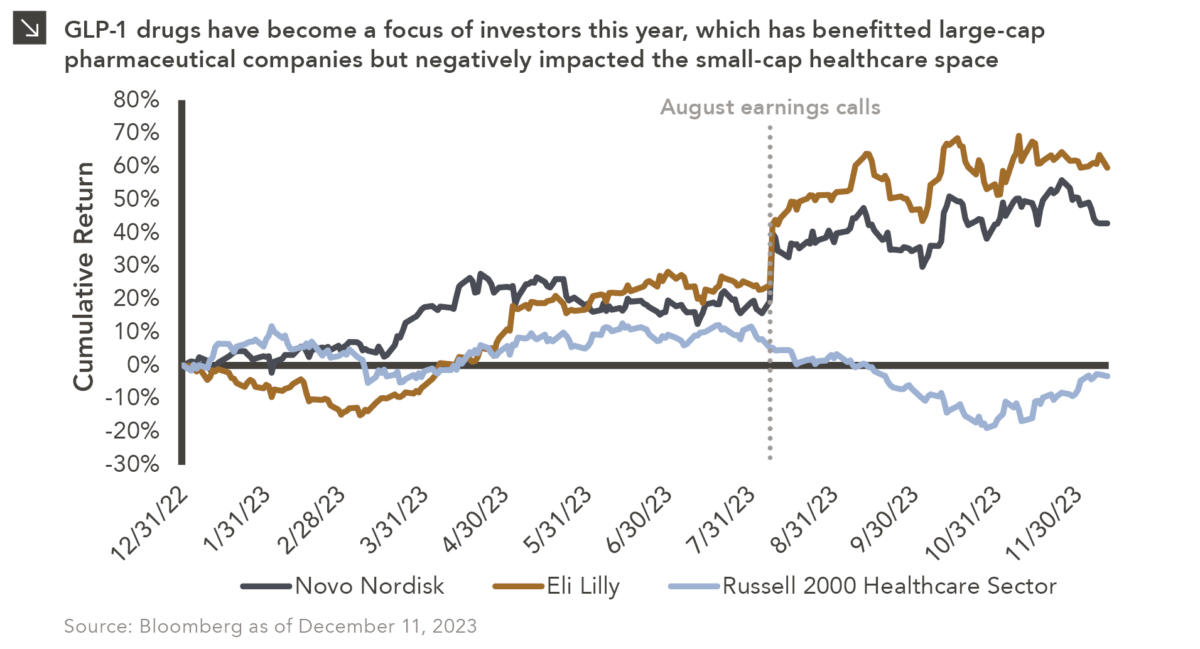

After a challenging 2022, during which significant drawdowns were exhibited by equity and fixed income indices alike, last year saw resurgent performance from most areas of the public market landscape. U.S. stocks were higher in 2023, with the S&P 500 and Russell 2000 indices posting returns of 26.3% and 16.9%, respectively, during the year. Key themes within domestic equity markets in 2023 included increased investor interest in GLP-1 obesity drugs, which led to strong performance from large-cap healthcare companies like Eli Lilly, as well as advances within the field of artificial intelligence. These advances resulted in narrow market leadership for much of 2023 and helped fuel a strong 42.7% calendar year return for the Russell 1000 Growth Index, which is home to each of the “Magnificent Seven” companies (Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia, and Tesla) that were ultimately some of the largest beneficiaries of AI-related fervor. Some may have expressed skepticism that U.S. equity markets would exhibit such robust calendar year returns in March of 2023, which saw a banking crisis that led to the shuttering of Silicon Valley Bank, Signature Bank, and First Republic Bank amid an aggressive monetary tightening campaign by the Federal Reserve and widespread runs on deposits. Fortunately, concerns about broader contagion were allayed when the Fed announced plans to protect uninsured deposits at the affected institutions, though performance of mid- and small-cap indices did suffer due to these events.

Non-U.S. equities posted gains in 2023 as well, with the MSCI EAFE and EAFE Small-Cap indices, which track developed market stocks, returning 18.2% and 13.2%, respectively. UK stocks, while still positive for the year, lagged the broad market due to economic stagnation and higher borrowing costs. Japanese equities, on the other hand, served as a bright spot within the developed market space given recent shareholder-friendly corporate governance reforms and monetary policy that continues to be accommodative. The MSCI Emerging Markets Index was positive for the year as well, notching a return of 9.8%. Companies domiciled in Latin American countries like Brazil and Mexico were some of the largest gainers within non-U.S. markets during the year, as many have benefited from a reconfiguration of global supply chains and favorable population demographics. Additionally, the Taiwanese company TSMC, which is the largest constituent of the MSCI EM Index, exhibited strong performance in 2023 thanks to the enthusiasm surrounding AI advances detailed above. Despite these positive outcomes, the 2023 return of the EM benchmark was hampered due to continued challenges faced by China, which was among the worst performing countries during the period. Indeed, a slump in its property sector, ongoing geopolitical issues, a weak job market, and widespread debt stress in the corporate space have spelled trouble for China’s economy in recent time, however, many believe the nation’s slowdown has bottomed.

Fixed income indices were also positive in 2023 after a dismal 2022, with falling inflation, a resilient economy, and expectations of interest rate cuts on the horizon leading to a bond market rally to end the year. To that point, the yield on the 10-year Treasury, which sat above 5.0% less than three months ago, has now dropped to below 3.9%. Thanks in part to these dynamics, the Bloomberg Aggregate Index notched a return of 5.5% in 2023, while high yield bonds (+13.4%) and bank loans (+13.0%) posted their best calendar year performance figures since 2019 and 2009, respectively.

It is important to note that private markets asset classes, including private equity and real estate, report performance on a lagged basis, meaning full calendar year returns for these spaces will not be available for some time. In the coming weeks, Marquette will be providing more detailed analysis related to both public and private market performance in 2023, as well as what investors might reasonably expect in the new year. We encourage clients, in tandem with their consultants, to review these analyses, as well as existing investment exposures and policy targets, to ensure the appropriate positioning of portfolios in 2024 and beyond. Finally, as it relates to the new year, we wish all readers many happy returns!