U.S. equities recently experienced a sharp three-day sell-off as the market digested the potential for short-term disruptions to economic growth and company earnings due to the Coronavirus (COVID-19). With new health figures coming out daily, it is easy to become alarmed. However, as our Chart of the Week from February 13th highlighted, prior health crises have been proven to be non-events longer-term for equity markets. Similar outbreaks in the past caused short-term sell-offs in equity markets but longer-term saw positive market performance.

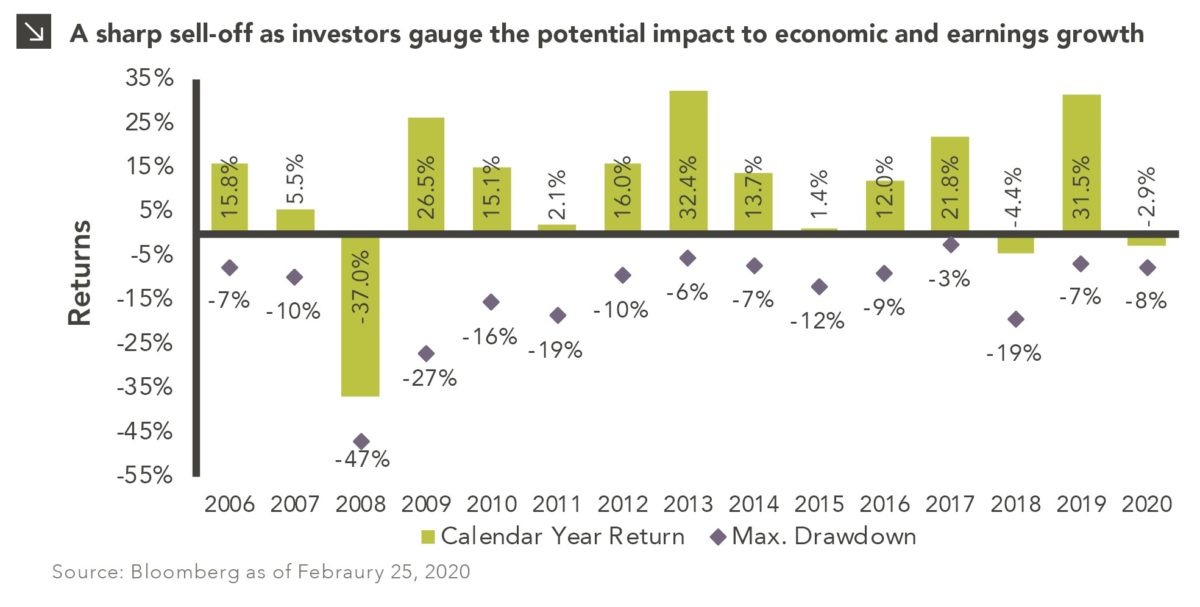

This week’s chart shows calendar year returns for the S&P 500 along with the max drawdown that occurred in each respective year. As of February 25, 2020, the S&P 500 has recorded a year-to-date drawdown of 7.6%. The current pullback is undeniably sharp in nature, but it is important to maintain perspective during turbulent times. Over the past 15 years, the average annual max drawdown was 14%. Many years experienced drawdowns near this level, yet still yielded a positive return for the year. On average, equities see a 5% pullback four times per year, a 10% pullback once per year, and a 20% correction once every five years.

While no one knows the full impact that the current outbreak will have to supply chains, trade, or travel, we recommend taking a long-term view to investing. The market had been looking past this current health crisis until the last few days, so a repricing of risk was inevitable. As this is an evolving situation, there is risk that the economic impact could increase and add further pressure to equities. However, the current pullback remains in-line with historical trends.

Print PDF > Coronavirus Roils the Equity Markets