2020 was a year like no other and has left investors across the world wondering what the future looks like. Will vaccines prove effective in halting a pandemic that spread like wildfire across the globe? What will the impact of a new administration in Washington be on economies and markets? How much additional stimulus will be injected into the economy? And most broadly, will things ever get back to “normal”? While there are no easy answers to these questions, 2021 promises to be another volatile year, most especially until there has been sufficient roll-out and distribution of vaccines to contain the COVID-19 outbreak that continues to haunt economic growth across the globe.

Remarkably, 2020 ended up as a positive year for financial markets despite a massive sell-off in the equity and credit markets during February and March. Paradoxically, 2021 may be a less eventful year but at the same time a lower overall return environment, given that much of the optimism about economic re-openings and stimulus has already been priced into the markets. Nonetheless, there are a variety of factors worth monitoring over the next year which will directly impact market returns. Similar to past years, we offer our 2021 market preview newsletters for each of the primary asset classes we cover, with in-depth analysis of last year’s performance as well as trends, themes, opportunities, and risks to watch for in 2021.

We hope these materials can assist you and your committees as you plan for the coming year and beyond. We have also produced a 2021 Market Preview video if you would like to hear a high-level summary of the market previews. Should you have any questions about anything related to these materials, please feel free to reach out to any of us for further assistance. Here’s to a return to normalcy in 2021!

U.S. Economy: Are Better Days Ahead?

by Brandon Von Feldt, CFA, Research Analyst

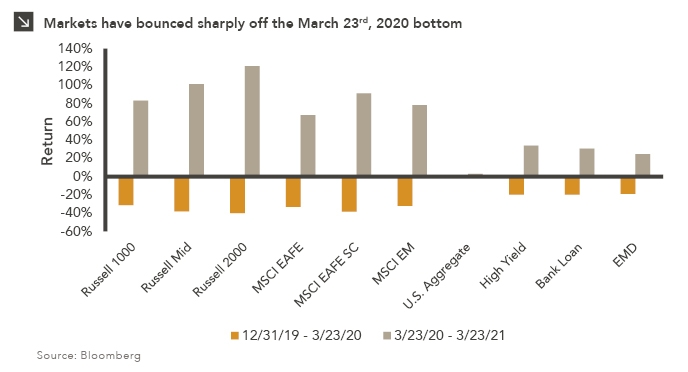

Fixed Income: Poised for Further Recovery with Undertones of Exuberance

by Ben Mohr, CFA, Director of Fixed Income

U.S. Equities: Birth of a New Market

by Samantha T. Grant, CFA, CAIA, Assistant Vice President,

Colleen Flannery, Research Analyst, U.S. Equities, and

Evan Frazier, CAIA, Research Analyst, U.S. Equities

Non-U.S. Equities: Constructive but Cautious

by David Hernandez, CFA, Senior Research Analyst, Non-U.S. Equities, and

Nicole Johnson-Barnes, CFA, Senior Research Analyst, Global Equities

Hedge Funds: Poised for Another Record Year?

by Joe McGuane, CFA, Senior Research Analyst, Alternatives

and Jessica Noviskis, CFA, Senior Research Analyst, Hedge Funds

Real Estate: Finding the New Normal

by Will DuPree, Senior Research Analyst, Real Assets

Infrastructure: An Evolving Opportunity Set, but an Essential Allocation

by Will DuPree, Senior Research Analyst, Real Assets

Private Equity: Both Quality and Growth Shine Brightly in 2020

by Derek Schmidt, CFA, CAIA, Director of Private Equity

Private Credit: Two Steps Forward, One Step Back

by Brett Graffy, CAIA, Research Analyst

Download the combined files > Traditional and Alternatives

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.