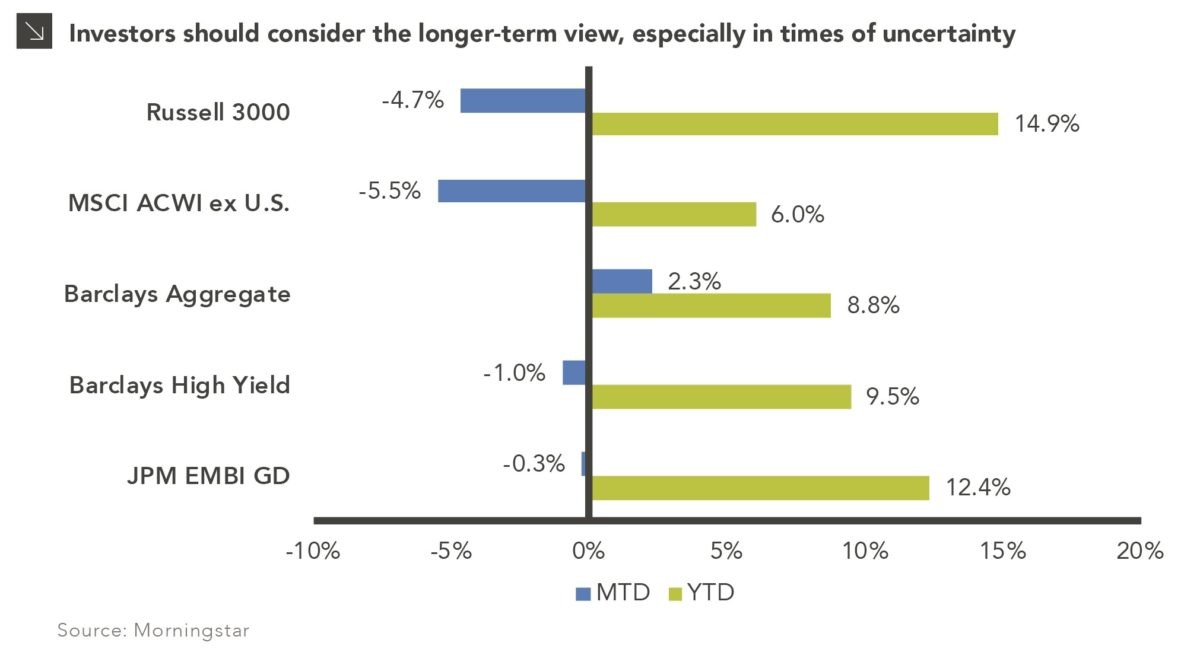

Given this week’s volatility driven by (brief) yield curve inversion, the ongoing U.S.-China trade dispute, disappointing economic data from Germany, and overall growing pessimism about future growth, investors’ growing concerns about portfolio returns are entirely justified. However, despite this week’s volatility and mostly negative news, almost all asset classes have delivered positive returns for the year, with the great majority of U.S. equity strategies up double digits. Furthermore, most fixed income strategies have profited from falling interest rates, as shown by positive returns from investment grade as well as below investment grade sectors. And for all the negative news out of the Eurozone and China, international equities — as represented by the ACWI ex-US index — are still up more than 6% through August 15th. While the rest of the year is likely to feature elevated volatility and lower returns, barring a major market correction most portfolios should remain in positive territory, despite what has transpired the first half of August. If nothing else, we encourage investors to take a long-term view of the markets and not overreact in times of market stress, as stepping back and taking a longer-term view of the markets indicates that 2019 has been a profitable year to date.

Print PDF > All is Not Lost for 2019

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.