An article by Marquette investment consultant and partner Linsey Schoemehl Payne was featured in the April 2021 edition of Benefits Magazine. The article, Sustainable Investment Options in a Post-COVID-19 World, examines performance trends for ESG investments, the impact of recent DOL guidance, and steps for evaluating ESG performance.

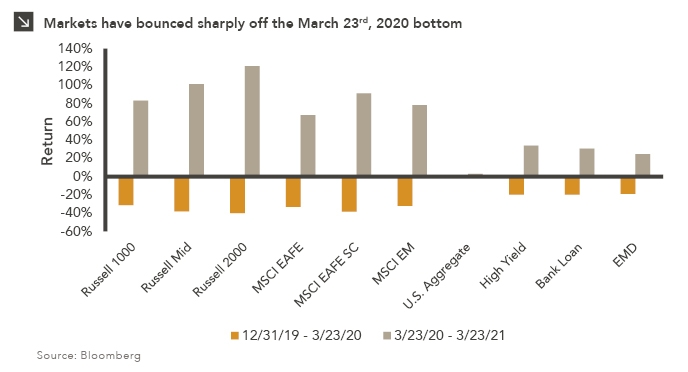

COVID-19 and the resulting economic recession have created the first sustainability crisis of the 21st century. As the virus spread across the globe in late March 2020, the global economy came to a screeching hald, and stocks experienced a record-breaking decline. While no sector was left unscathed, research showed that investment strategies that integrated environmental, social, and governance (ESG) factors into their approach provided more downside protection compared with those that did not. ESG integration is a returns-based approach, using ESG factors as an additional source of information during the investment manager’s risk analysis process. This article explores the why and how of that resilience in times of market turmoil, as well as the hurdles plan sponsors should consider when selecting investments that are considered ESG or sustainable strategies.

For more of Marquette’s sustainable investing coverage, reference our research here. Linsey previously presented our video series, Sustainable Investing, an introduction to our approach to ESG integration and considerations, and has also authored several papers on the topic. An owner of the firm, Linsey has been with the company since 2016 and has 13 years of investment experience. Linsey is the vice chair of the firm’s sustainable investing group and a member of the OCIO committee. She holds a B.A. in political science from the University of Missouri-Columbia, a J.D. from the DePaul University College of Law, and an M.B.A. with honors from the University of Chicago Booth School of Business.

Benefits Magazine, the monthly publication of the International Foundation of Employee Benefit Plans, covers benefit issues affecting multiemployer, single employer, and public employee plan representatives.

Download PDF > Sustainable Investment Options in a Post-COVID-19 World

Reproduced with permission from Benefits Magazine, Volume 58 Number 4, pages 24-31, April 2021, published by the International Foundation of Employee Benefit Plans (www.ifebp.org), Brookfield, Wisconsin. All rights reserved. Statements or opinions expressed in this article are those of the author and do not necessarily represent the views or positions of the International Foundation, its officers, directors or staff. No further transmission or electronic distribution of this material is permitted.

The opinions expressed herein are those of Marquette Associates, Inc. (“Marquette”), and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Marquette reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.