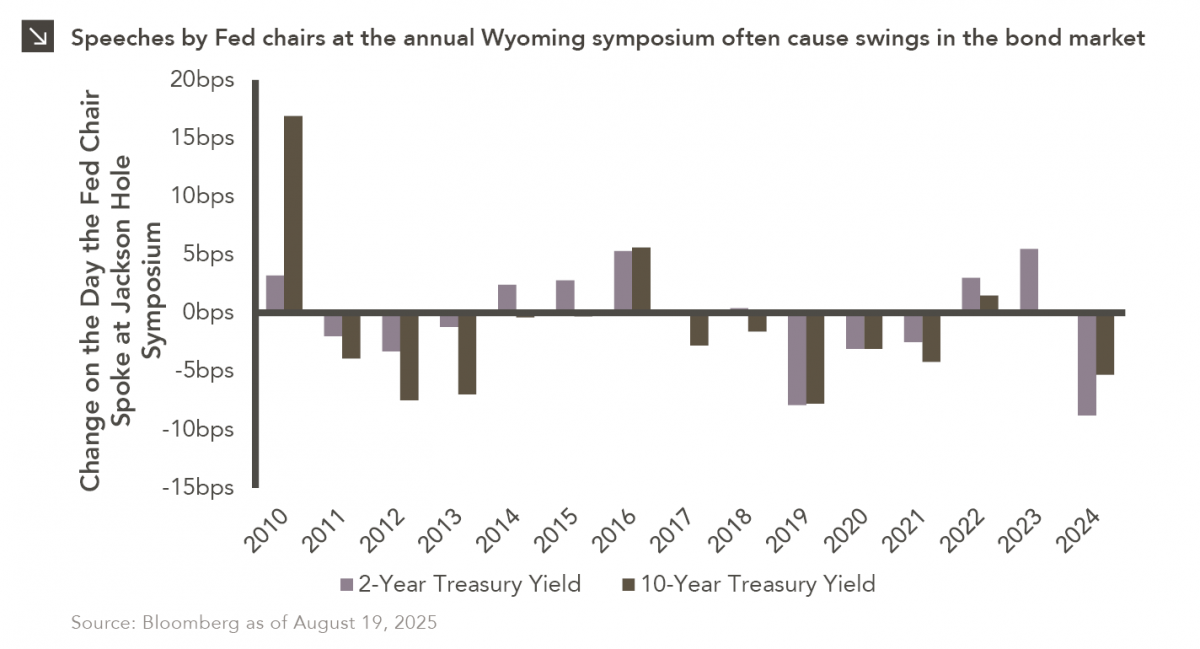

No, you are not seeing double. This very special edition of our chart of the week series comes with an added bonus chart with the goal of highlighting key dynamics within fixed income markets that have been top of mind for investors in recent weeks. Read on and enjoy two charts for the price of one!

What’s Your Haven?

Fixed income has historically provided three benefits to investors: Income, diversification, and liquidity. U.S. Treasuries are a pure form of diversification given their limited risk with the 10-year Treasury serving as a bellwether, and these securities are viewed by many as safe havens during periods of market stress. Historically, Treasuries and equities have tended to exhibit low to negative correlations. However, much like returns and volatility, correlations are time-varying. For instance, the historical relationship between stocks and bonds broke down in the aftermath of the COVID-19 crisis, when accommodative monetary policy led to higher levels of inflation and the two asset classes moved in tandem. The same pattern took hold over the last few weeks amidst tariff-induced market volatility, with correlations between stocks and Treasuries increasing and hampering traditional diversification benefits. With Treasury rates recently trading like risk assets, there are other safe haven assets to which investors have turned for insulation against volatility.

Gold is often referred to as a safe haven asset given its status as a precious metal that is viewed as a store of value and a hedge against inflation. Over the last few years, gold has offered favorable diversification relative to risk assets with inflation running hot. It also tends to do well when fears are high. To that point, with the S&P 500 Index down more than 8% on a year-to-date basis, spot gold prices have risen from $2,625/oz to $3,312/oz.¹ All of this being said, gold is not necessarily a good investment as it does not provide cash flows and its price movements are largely driven by speculation. Additionally, the correlation of gold to equities fluctuates over time from somewhat positive to somewhat negative, with material variations over longer investment horizons.

Some currencies are also viewed as safe haven assets, with the classic example being the yen given Japan’s stable political system and ample liquidity. The yen has rallied with stocks down this year, moving from ¥157.20/$ to ¥142.66/$. Diversification benefits from the yen have historically been better than those provided by gold, but they have also waned somewhat in recent years. Currencies also suffer from some of the same issues as gold, including a lack of cash flows and price speculation. As such, most currencies are generally best used as tactical hedges as opposed to long-term portfolio constituents.

Diversification is a critical component of portfolio construction and while Treasuries have historically served as safe havens during market volatility, other assets have offered more compelling diversification benefits in recent weeks. However, the viability of these assets (i.e., gold and currencies) as outright replacements for Treasuries in portfolios is questionable given the points made above.

¹ Bloomberg as of April 16, 2025

Who is the “Godfather” of the Bond Market?

Current global trade tensions beg the question: Can foreign holders of U.S. debt manipulate the Treasury market? Indeed, some have speculated that China sold Treasuries to put upward pressure on yields last week to retaliate against the U.S. for its new tariffs (i.e., causing the U.S. to borrow at higher rates). This action, however, would likely be painful for China as well. If news of significant Treasury sales by China were to circulate, yields would likely spike, and the value of its remaining holdings would fall. The U.S. also has tools to combat such a move, including quantitative easing (i.e., bond purchases) designed to return yields to normal levels. Ultimately, a retaliatory Treasury sale would be a huge risk to China, not to mention the fact that China’s holdings tend to be of a shorter nature and recent pressure has mostly been on the long end of the curve (which sold off by around 50 basis points last week). Might another country be responsible for this movement?

While some Japanese politicians have lobbied for using its country’s Treasury holdings as a tool in trade negotiations, the ruling party has repeatedly emphasized that Japan should not sell its Treasuries to rile the United States. So, while Japan has indeed been a notable seller of U.S. Treasuries in recent weeks, these sales have likely been influenced by other factors. For instance, Japanese life insurers are major holders of long-dated U.S. Treasuries, and these entities could be rotating out of Treasuries given a cautious stance on U.S. policy. Another potential reason for recent sales is Japanese pension plans rotating into European bonds.

In summary, technical signals from non-U.S. investors can certainly influence the Treasury market, but it is unlikely that these players could engage in outright market manipulation. At the end of the day, the Federal Reserve can pull strings to combat Treasury-related turmoil and remains the godfather of the bond market.