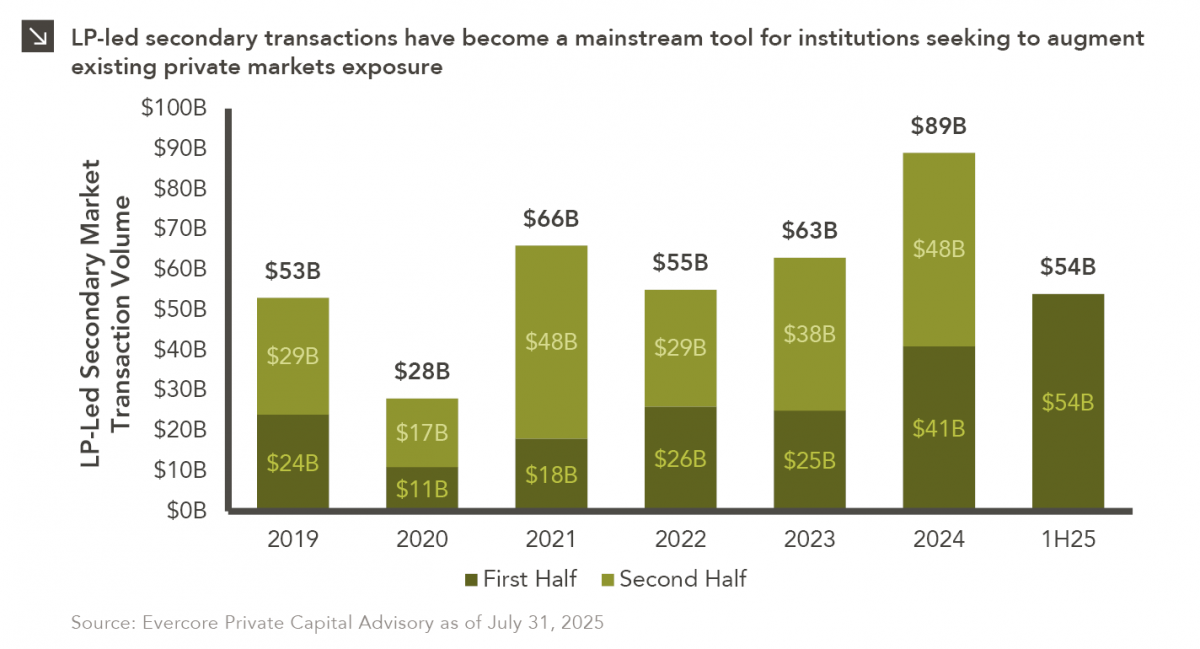

Private equity is known for being an illiquid asset class, with investments typically locked up for several years and limited options to access cash before a fund winds down. Investors have largely accepted these restrictions in exchange for the potential of higher returns, but this lack of liquidity has become a challenge more recently. For instance, DPI (distributions to paid-in capital) as a percentage of net asset value for 2024 was 12%, significantly lower than the 25-year average of 21%. As a result of these dynamics, there has been rapid growth in the private equity secondary market, which allows investors to sell their existing stakes in ongoing private equity funds. Indeed, what was once a niche option for distressed sellers is now a mainstream tool for managing portfolios, with global secondary market transactions on pace to exceed $200 billion in 2025. This figure would constitute a record high. Interestingly, more than 50% of secondary transactions in the first half of this year came in the form of Limited Partner (“LP”)-led secondaries, which occur when existing LPs sell fund interests to other investors.

The rise of LP-led secondaries is about more than investors simply “cashing out.” Specifically, LPs may tap the secondary market to rebalance portfolios when private equity exposure becomes too high, move away from underperforming funds, or free up capital to invest in new opportunities. Institutions of all types are embracing this strategy. For instance, the University of Illinois Foundation recently announced the sale of roughly $245 million of net asset value of private market assets, aiming to reduce exposure to high-risk, illiquid positions and reposition its endowment for greater long-term stability. Additionally, CalPERS announced a potential $3 billion secondary transaction earlier this year, and Yale University is currently in talks for its first-ever secondaries sale to convert older private equity holdings into liquid assets for reinvestment. These developments reflect a broader trend among institutional investors seeking flexibility and liquidity amid a challenging private equity environment. Indeed, as private equity funds continue to hold assets for longer and exit activity remains slow, the secondary market may become a standard part of portfolio management for both large institutions and smaller investors in the years ahead.