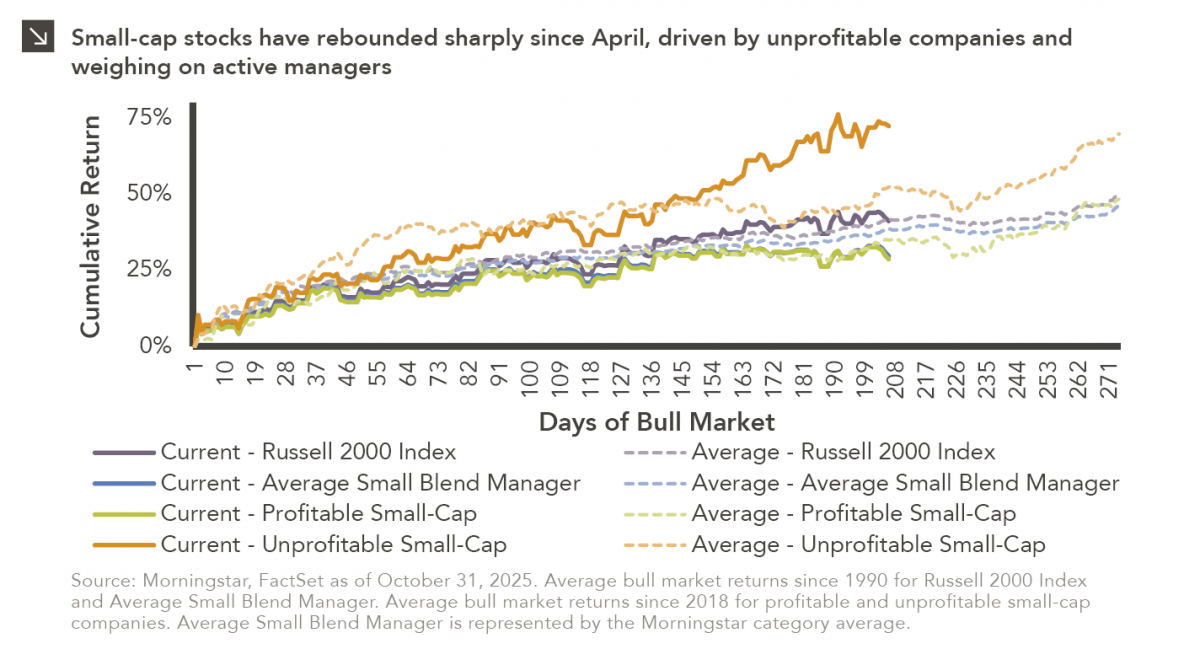

Small-cap equities are in a prolonged period of underperformance relative to large-cap stocks, but this trend has shown early signs of reversing in the aftermath of intra-year market lows on April 8, with the Russell 2000 Index up roughly 41% since that time. Interestingly, unprofitable companies within the benchmark have led the way, gaining more than 72% compared to a relatively meager 29% for profitable constituents of the Russell 2000 Index. Although the overall small-cap equity market is currently in line with its average bull market return amid this run, recent performance of unprofitables far exceeds historical norms. This dynamic can be observed in the chart above.

One of the major consequences of this trend is significant underperformance of actively managed small-cap strategies, which typically eschew companies with poor fundamentals. Specifically, the average active small-cap blend manager (as represented by the Morningstar category average) has underperformed the Russell 2000 Index by more than 10 percentage points since April 8, an extreme not seen in roughly 25 years. On the positive side, active small-cap strategies have slightly outperformed profitable small-cap companies, which are more likely to be included in these types of funds. Should this persist, it may be a tailwind for active managers, as profitable companies may have additional upside from here based on trends observed in prior bull markets. That said, more accommodative monetary policy and fiscal support may lead to additional strength from unprofitables and, as a result, further underperformance of active managers.